What Is the Weighted Average Cost of Capital (WACC)?

The weighted average cost of capital (WACC) is the blended rate a company pays to finance its operations across all sources of capital, equity, debt, and preferred stock. It represents the minimum return a company must earn on its existing assets to satisfy its investors and creditors.

WACC is calculated using this formula:

WACC = (E/V x Re) + (D/V x Rd x (1 – T))

Where E is equity value, D is debt value, V is total capital (E + D), Re is the cost of equity, Rd is the cost of debt, and T is the corporate tax rate.

In company valuation, WACC serves as the discount rate in a discounted cash flow (DCF) analysis, one of the most widely used methods for estimating a company’s intrinsic value. A lower WACC increases the present value of future cash flows, resulting in a higher valuation. A higher WACC does the opposite.

This article explains each WACC component, walks through a full calculation with real numbers, and covers the most common mistakes analysts make when estimating WACC.

Starting your finance career?

Our Starter Program gives you the foundational skills to land your first analyst role, including DCF valuation, financial modeling, and interview preparation.

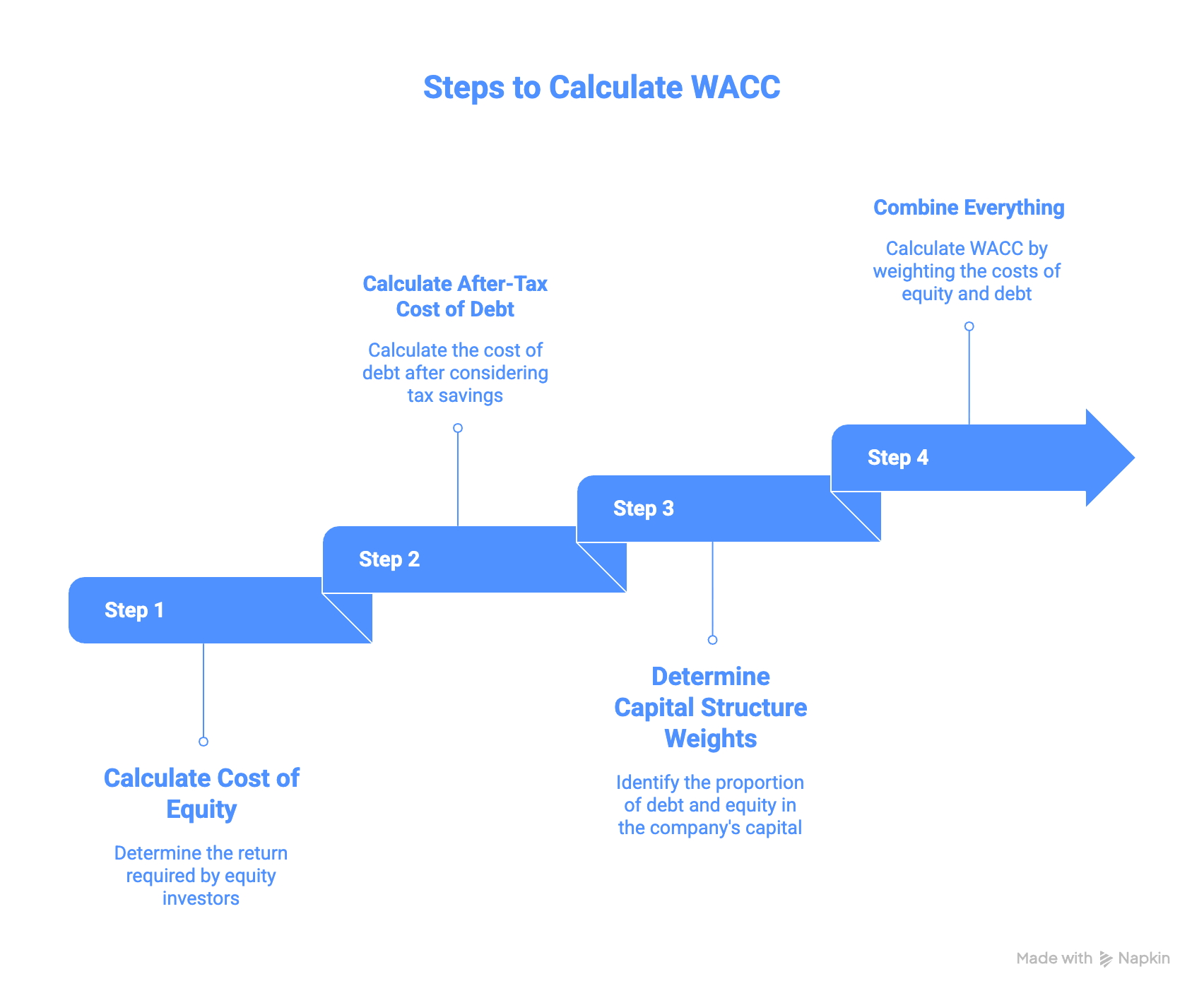

How Do You Calculate WACC?

Calculating WACC requires three inputs: the cost of equity, the after-tax cost of debt, and the capital structure weights. Each component is weighted by its proportion of total financing, then summed to produce the blended rate.

The WACC Formula:

WACC = (E/V x Re) + (D/V x Rd x (1 – T))

| Variable | Meaning | How to Find It |

|---|---|---|

| E | Market value of equity | Share price × shares outstanding (market capitalization) |

| D | Market value of debt | Face value of outstanding bonds and loans (or use book value as a proxy) |

| V | Total capital value | E + D |

| E/V | Equity weight | Market cap / Total capital |

| D/V | Debt weight | Debt / Total capital |

| Re | Cost of equity | Calculated via CAPM (see below) |

| Rd | Cost of debt | Interest expense / Total debt, or yield on traded bonds |

| T | Corporate tax rate | Effective tax rate from financial statements |

Important: Use market values, not book values, for equity and debt weights. Book value of equity often differs dramatically from market value; using it is one of the most common WACC errors.

Step 1: Calculate the Cost of Equity (Re)

The cost of equity is the return shareholders require for investing in the company. The standard method is the Capital Asset Pricing Model (CAPM):

Re = Rf + B x (Rm – Rf)

| Variable | Meaning | Typical Source |

|---|---|---|

| Rf | Risk-free rate | 10-year government bond yield (FRED for US rates) |

| B (Beta) | Stock’s sensitivity to market movements | Industry-average unlevered beta from Damodaran’s data |

| Rm – Rf | Equity risk premium | Historical or implied premium (Damodaran’s country risk premiums) |

Example: If the risk-free rate is 4.2%, beta is 1.1, and the equity risk premium is 5.5%:

Re = 4.2% + 1.1 x 5.5% = 4.2% + 6.05% = 10.25%

Step 2: Calculate the After-Tax Cost of Debt (Rd x (1 – T))

The cost of debt is the effective interest rate a company pays on its borrowings. Because interest payments are tax-deductible, you use the after-tax cost:

After-tax Rd = Rd x (1 – T)

To find Rd:

- For public companies: Use the yield to maturity on outstanding bonds

- If no traded bonds: Divide total interest expense by total debt from the financial statements (available on SEC EDGAR for US companies)

- For credit-rated companies: Use the credit spread over the risk-free rate

Example: If the cost of debt is 5.0% and the tax rate is 25%:

After-tax Rd = 5.0% x (1 – 0.25) = 5.0% x 0.75 = 3.75%

The tax shield on debt is the reason WACC often decreases as a company adds moderate levels of debt; the government effectively subsidizes the cost of borrowing through the interest tax deduction.

Step 3: Determine the Capital Structure Weights

Use the market value of equity and debt to determine each source’s weight:

- Equity weight (E/V): Market capitalization / (Market cap + Market value of debt)

- Debt weight (D/V): Market value of debt / (Market cap + Market value of debt)

The weights should reflect the company’s optimal capital structure, the mix of debt and equity that minimizes WACC. If the current structure is temporarily distorted (e.g., recent large debt issuance), many analysts use target weights instead.

Step 4: Combine Everything

Multiply each cost by its weight and sum the results.

Full Worked Example:

Suppose you are valuing a manufacturing company with the following data:

| Input | Value |

|---|---|

| Market cap (E) | $800 million |

| Market value of debt (D) | $200 million |

| Total capital (V) | $1,000 million |

| Cost of equity (Re) | 10.25% |

| Cost of debt (Rd) | 5.0% |

| Tax rate (T) | 25% |

Calculation:

- Equity weight: E/V = $800M / $1,000M = 0.80 (80%)

- Debt weight: D/V = $200M / $1,000M = 0.20 (20%)

- After-tax cost of debt: 5.0% x (1 – 0.25) = 3.75%

WACC = (0.80 x 10.25%) + (0.20 x 3.75%) WACC = 8.20% + 0.75% WACC = 8.95%

This means the company must earn at least 8.95% on its investments to satisfy both equity and debt investors. In a DCF model, you would discount future free cash flows at 8.95% to determine the company’s enterprise value.

Sanity check: Compare your result against Damodaran’s WACC by industry data. If your calculated WACC is dramatically different from the industry average, revisit your inputs.

Why Does WACC Matter in Valuation?

WACC is not just a textbook formula; it is one of the most consequential numbers in corporate finance. Small changes in WACC produce large changes in valuation, especially for companies with long-duration cash flows.

WACC as a DCF Discount Rate

In a discounted cash flow analysis, WACC serves as the rate at which future free cash flows to the firm (FCFF) are discounted to present value. The relationship is direct:

- Lower WACC = Higher present value = Higher valuation

- Higher WACC = Lower present value = Lower valuation

A 1-percentage-point change in WACC can shift an enterprise value by 10-20%, depending on the company’s growth profile and terminal value assumptions. This is why WACC estimation deserves careful analysis, not a quick back-of-the-envelope calculation.

WACC as a Hurdle Rate

Companies also use WACC as a hurdle rate for capital budgeting decisions. A project should only be accepted if its expected return exceeds WACC; the company is destroying value by investing in projects that earn less than what investors require.

WACC and Value Creation

The difference between a company’s return on invested capital (ROIC) and its WACC determines whether the company is creating or destroying value:

| Scenario | Meaning |

|---|---|

| ROIC > WACC | The company creates value; every dollar invested earns more than it costs |

| ROIC = WACC | The company earns exactly its cost of capital; no value created or destroyed |

| ROIC < WACC | The company destroys value; investments earn less than the investor’s required return |

This relationship is fundamental to understanding why some companies trade at premiums (consistently high ROIC relative to WACC) and others trade at discounts.

Ready to advance?

The Advancer Program helps mid-career professionals sharpen their valuation and equity research skills and stand out for promotions or lateral moves into investment roles.

What Is a Good WACC?

There is no universal “good” WACC because it varies by industry, geography, company size, and market conditions. However, benchmarks help you evaluate whether your estimate is reasonable.

WACC Ranges by Industry

| Industry | Typical WACC Range | Why |

|---|---|---|

| Utilities | 4-6% | Stable cash flows, high debt capacity, regulated returns |

| Consumer Staples | 6-8% | Predictable demand, moderate leverage |

| Industrials / Manufacturing | 8-10% | Cyclical exposure, moderate risk |

| Technology | 9-12% | High growth uncertainty, mostly equity-financed |

| Biotech / Early-stage | 12-18% | Extreme uncertainty, no debt capacity |

These ranges shift with macroeconomic conditions. When interest rates rise, both the risk-free rate and cost of debt increase, pushing WACC higher across all industries.

How Capital Structure Affects WACC

Because debt is cheaper than equity (due to the tax shield and lower risk to lenders), adding debt generally lowers WACC up to a point. Beyond that point, financial distress risk increases, credit spreads widen, and equity holders demand higher returns to compensate for leverage risk.

This tradeoff defines the optimal capital structure, the debt-to-equity ratio that minimizes WACC and maximizes firm value. The concept comes from the Modigliani-Miller theorem, which, in its modified form, shows that tax benefits of debt lower WACC until distress costs offset the advantage.

WACC vs. Cost of Equity: What Is the Difference?

These two concepts are frequently confused, but they serve different purposes in valuation.

| Feature | WACC | Cost of Equity |

|---|---|---|

| Definition | Blended cost of all capital (debt + equity) | Return required by equity investors only |

| Formula | (E/V × Re) + (D/V × Rd × (1 − T)) | Re = Rf + B × (Rm − Rf) via CAPM |

| Used to discount | Free cash flow to the firm (FCFF) | Free cash flow to equity (FCFE) or dividends |

| Result | Enterprise value | Equity value directly |

| Always lower than the cost of equity? | Yes (because debt is cheaper after tax) | Higher because equity bears more risk |

| Affected by leverage? | Yes, more debt can lower or raise WACC | Yes, more debt increases equity risk and Re |

When to use each:

- Use WACC when discounting FCFF in a DCF model to find enterprise value. This is the most common approach in investment banking and equity research

- Use the cost of equity when discounting FCFE or dividends (e.g., the Gordon Growth Model) to find equity value directly

- Use the cost of equity for financial institutions (banks, insurers) where separating operating and financing decisions is impractical

For a deeper explanation of the cost of equity component and its calculation methods, see our guide on the cost of equity.

Common Mistakes When Calculating WACC

Even experienced analysts make errors with WACC. Here are the most frequent mistakes and how to avoid them:

| Mistake | Why It Is Wrong | How to Fix It |

|---|---|---|

| Using book value weights | Book equity can differ from market cap by 2–10×, distorting the capital structure | Always use the market value of equity; approximate market value of debt if needed |

| Using the raw calculated beta | Beta varies dramatically with time period, frequency, and index chosen | Use industry-average unlevered betas from Damodaran, then re-leverage for the company’s target capital structure |

| Ignoring the tax shield | Omitting (1 − T) overstates the cost of debt, inflating WACC | Always use after-tax cost of debt: Rd × (1 − T) |

| Wrong risk-free rate | Using a short-term rate (3-month T-bill) for a long-term valuation | Match the risk-free rate to the duration of the cash flows, typically the 10-year government bond |

| Mixing currencies | Using a USD risk-free rate but cash flows in EUR | Ensure the risk-free rate, equity risk premium, and cash flow currency all match |

| Assuming WACC is constant over time | Capital structure and risk profiles change as companies grow or delever | Reassess WACC periodically; consider using a changing discount rate for early-stage companies |

| Not sanity-checking the result | An unreasonable WACC produces an unreasonable valuation | Compare against industry averages from Damodaran’s WACC data |

For a broader discussion of how WACC theory differs from real-world application, see WACC: Theory Versus Reality.

Switching into finance from another field?

Our Switcher Program is designed for career changers who need to build credibility fast — no finance background required.

Frequently Asked Questions

What does WACC stand for?

WACC stands for weighted average cost of capital. It is the average rate a company pays to finance its operations, weighted by the proportion of each capital source (equity and debt) in the company’s total capital structure. WACC reflects the minimum return the company must earn on its assets to satisfy all investors.

Why is WACC used as a discount rate in DCF?

WACC represents the opportunity cost of the capital invested in a company. In a DCF model, free cash flows to the firm belong to all capital providers, both equity and debt holders. WACC is the appropriate discount rate because it blends the required returns of both groups, weighted by their share of total financing.

How does debt affect WACC?

Adding debt typically lowers WACC because interest payments are tax-deductible, making debt cheaper than equity on an after-tax basis. However, excessive debt increases financial distress risk, causing both lenders and equity holders to demand higher returns. The debt level that minimizes WACC defines the optimal capital structure.

What is the difference between WACC and IRR?

WACC is the cost of capital, the minimum return investors require. IRR (internal rate of return) is the expected return on a specific project or investment. A project creates value when its IRR exceeds WACC and destroys value when IRR falls below WACC. Companies use WACC as the hurdle rate to evaluate whether individual investments are worthwhile.

Can WACC be negative?

In theory, WACC cannot be negative because both the cost of equity and the cost of debt are positive numbers. The cost of equity reflects a positive risk premium above the risk-free rate, and the cost of debt reflects a positive interest rate. Even with the tax shield on debt, the after-tax cost of debt remains positive as long as interest rates are above zero.

What is a typical WACC for US companies?

WACC varies widely by industry and market conditions. As of recent data, the median WACC for US companies falls between 7% and 10%. Utilities and consumer staples tend to have lower WACCs (4-7%) due to stable cash flows and high debt capacity. Technology and biotech companies tend to have higher WACCs (10-15%) due to greater uncertainty and equity-heavy financing.

Where can I learn DCF valuation online?

The Valuation Master Class Boot Camp teaches DCF valuation with hands-on practice on real companies. Over 12 weeks, you build professional equity research reports with expert feedback from Dr. Andrew Stotz, a former #1-ranked equity analyst. The program covers WACC calculation, free cash flow projection, terminal value estimation, and the complete DCF framework used by investment banks and equity research firms.

Ready to Take the Next Step?

Join 5,000+ finance professionals who’ve leveled up with Valuation Master Class.