What Is Stock Valuation?

Stock valuation is the process of determining the intrinsic (or fair) value of a company’s stock using financial analysis. By estimating what a stock is truly worth, investors can decide whether it is overvalued, undervalued, or fairly priced in the market. This is one of the most fundamental skills in company valuation methods and investment analysis.

There are two primary approaches to stock valuation:

-

Absolute valuation, which estimates intrinsic value using the company’s own financial data (e.g., DCF and DDM models)

-

Relative valuation, which compares a company to peers using valuation multiples like P/E or EV/EBITDA

Stock valuation is a foundational skill in investment analysis, equity research, and corporate finance. This guide explains the core methods, formulas, practical applications, and common mistakes to avoid.

Starting your finance career?

Our Starter Program gives you the foundational skills to land your first analyst role — DCF valuation, financial modeling, and interview prep included.

What Does Stock Valuation Mean?

Stock valuation refers to the analytical process of estimating a company’s theoretical value based on its:

-

Earnings

-

Cash flows

-

Growth expectations

-

Risk profile

-

Cost of capital

The key concept behind valuation is intrinsic value, the present value of future economic benefits the company is expected to generate.

If intrinsic value exceeds the current market price, the stock may be undervalued. If it is lower than the market price, the stock may be overvalued.

Professional analysts use valuation not only for buy/sell decisions, but also for:

-

Mergers and acquisitions

-

IPO pricing

-

Portfolio allocation

| Term | Meaning |

|---|---|

| Intrinsic value | The estimated “true” worth of a stock based on fundamentals |

| Market price | The current trading price is determined by supply and demand |

| Undervalued | Intrinsic value > market price — potential buy signal |

| Overvalued | Intrinsic value < market price — potential sell signal |

| Fairly valued | Intrinsic value ≈ market price |

How Do You Value a Stock?

There are 2 main ways to value stocks: absolute and relative valuation.

| Feature | Absolute Valuation | Relative Valuation |

|---|---|---|

| Approach | Calculates intrinsic value from the company’s own financials | Compares the company to similar firms in the same industry |

| Key methods | DCF, DDM (Gordon Growth Model) | P/E ratio, EV/EBITDA, P/B ratio, P/S ratio |

| Data required | Cash flows, dividends, growth rates, discount rate | Stock prices and financial metrics of peer companies |

| Best for | Companies with predictable cash flows or dividends | Quick comparisons within an industry or sector |

| Limitation | Highly sensitive to assumptions (growth rate, discount rate) | Assumes the peer group is fairly valued |

Absolute Valuation

- Absolute valuation is calculated through the discounted dividend model (DDM) method and the discounted cash flow (DCF) method, where you only focus on the stock and look at its dividends, cash flow, and growth.

Dividend Discount Model (DDM)

- The DDM method allows you to value a company by looking at the sum of all the future dividend payments that have been discounted back to the net present value.

- The most common form of the DDM is the Gordon Growth Model (GGM), which assumes dividends grow at a constant rate indefinitely.

The GGM formula is: P = D1 / (r – g)

Where:

- P = intrinsic value of the stock (current fair price)

- D1 = expected dividend per share next year

- r = required rate of return (cost of equity)

- g = constant dividend growth rate

The GGM works best for mature, stable companies that pay regular dividends, such as utilities, consumer staples, and large-cap blue chips. It is less appropriate for high-growth companies that reinvest earnings instead of paying dividends.

For example, if a company lists its stock price at $50, has a required rate of return at 15% (r), pays a dividend of $1 per share you own, and has a constant growth rate of 6%, then how would you calculate the stock value?”

“$1 / (0.15 – 0.06) = $11.11”

“Therefore, you would say that the stock price is overvalued, as the GGM says that the stock price should only be $11.11.

Discounted Cash Flow (DCF)

- Another method to use is the discounted cash flow (DCF). Often, companies don’t pay dividends every quarter or every year, hence making their payouts irregular.

- The DCF is the perfect method to use when in a situation like this. The DCF method asks you to discount all the future cash flows of the company to the present value.

The basic DCF formula for a single period is: PV = CF / (1 + r)^n

Where:

- PV = present value

- CF = expected future cash flow

- r = discount rate (often the weighted average cost of capital, or WACC)

- n = number of periods into the future

For a multi-year DCF, you sum the present value of each year’s projected cash flow, plus a terminal value representing the company’s value beyond the forecast period. Learning to build a DCF model from scratch is one of the most valuable skills in finance.

Say a company currently has a cash flow of $10,000 and has a growth rate of 3% for one year. How do you calculate this?

[10,000 / (1 + 0.05)^1] = $9,070.29

Hence, the current value of the cash flow is $9,070.29.

Relative Valuation

- Relative valuation compares a stock’s value to its competitors and peers within the same industry.

- The main relative valuation ratios include price to free cash flow, enterprise value (EV), operating margin, price to sales, and price to earnings.

- The most popular ratio is the price-to-earnings ratio. The price-to-earnings (P/E) ratio is calculated by dividing the stock price by its earnings per share (EPS) and is expressed as a multiple.

- A company with a stock of a higher P/E ratio than its peers is considered overvalued, while a company with a relatively low P/E ratio in comparison to its peers is considered undervalued.

Beyond the P/E ratio, analysts commonly use these relative valuation multiples:

| Multiple | Formula | Best Used For |

|---|---|---|

| P/E (Price-to-Earnings) | Stock Price / EPS | Most companies with positive earnings |

| EV/EBITDA | Enterprise Value / EBITDA | Comparing companies with different capital structures |

| P/B (Price-to-Book) | Stock Price / Book Value per Share | Asset-heavy industries (banks, real estate) |

| P/S (Price-to-Sales) | Stock Price / Revenue per Share | High-growth or pre-profit companies |

| PEG Ratio | P/E Ratio / Earnings Growth Rate | Growth companies adjust P/E for expected growth |

Choosing the right multiple depends on the industry, company stage, and available data. For a deeper analysis of which valuation method is the most suitable for different types of companies, consider the company’s maturity, profitability, and sector characteristics.

Why Is Stock Valuation Important?

Stock valuation is important because it can be used to identify whether a stock is overvalued, undervalued, or at the market price. Investing in a company that is overvalued provides a huge downside risk. Whereas investing in an undervalued company can significantly reduce the risk. Therefore, stock valuation enables you to understand your risk.

Stock valuation is important for several key reasons:

- Investment decision-making: Valuation tells you whether a stock’s price reflects its fundamentals or is driven by speculation. This is the basis of value investing, famously practiced by Warren Buffett and Benjamin Graham.

- Risk management: By understanding what a stock is worth, you can set rational price targets, manage position sizes, and avoid overpaying during market euphoria.

- Career readiness: Equity research analysts, investment bankers, and portfolio managers perform stock valuations daily. Mastering this skill is essential for landing and succeeding in finance career roles.

- Corporate transactions: Companies use stock valuation for mergers, acquisitions, IPOs, and private placements. Accurate valuation prevents value destruction in deals.

- Performance benchmarking: Metrics like return on invested capital (ROIC) help investors assess whether management is creating or destroying shareholder value.

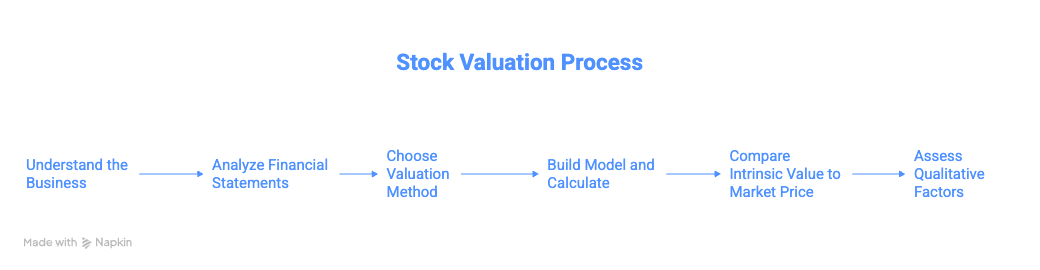

How to Value a Stock: A Step-by-Step Process

Valuing a stock involves a systematic process. Here is a practical framework that analysts follow:

Step 1: Understand the business

Before running any numbers, research the company’s products, revenue model, competitive position, and industry dynamics (Porter’s Five Forces). You cannot value what you do not understand.

Step 2: Analyze the financial statements

Review the income statement, balance sheet, and cash flow statement. Look at revenue growth, profit margins, debt levels, and free cash flow trends over the past 3-5 years.

Step 3: Choose a valuation method

Select absolute valuation (DCF or DDM) if you want to estimate intrinsic value from fundamentals, or relative valuation (P/E, EV/EBITDA) if you want to compare the stock to its peers. Most analysts use both approaches as a cross-check.

Step 4: Build your model and calculate

For a DCF, project future cash flows, determine the appropriate discount rate (WACC), and calculate present value. For relative valuation, gather peer multiples and apply them to the company’s metrics.

Step 5: Compare intrinsic value to market price

If your calculated value is significantly above the current stock price, the stock may be undervalued. If it is below, the stock may be overvalued. Factor in a margin of safety to account for estimation uncertainty.

Step 6: Assess qualitative factors

Consider management quality, competitive moats, regulatory risks, and macroeconomic conditions. Numbers alone do not capture the full picture. Aswath Damodaran’s approach to equity valuation demonstrates how narrative and numbers work together. For a real-world example of this process in action, see this Coca-Cola valuation case study.

Ready to advance?

The Advancer Program helps mid-career professionals sharpen their valuation and equity research skills and stand out for promotions or lateral moves into investment roles.

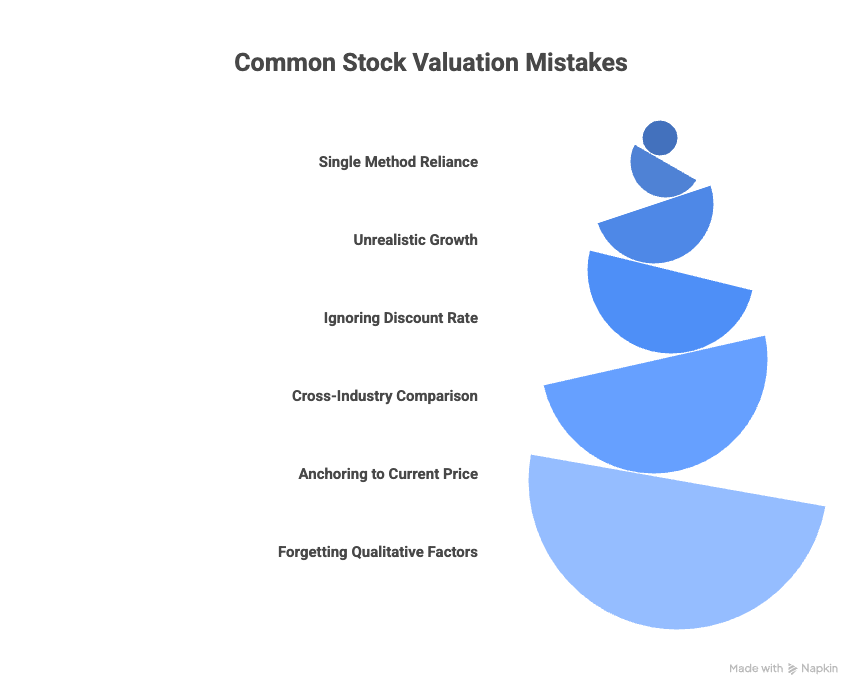

Common Stock Valuation Mistakes to Avoid

Even experienced analysts make valuation errors. Here are the most common mistakes and how to avoid them:

1. Relying on a single valuation method

No single method captures everything. A DCF might produce a compelling intrinsic value, but if every comparable company trades at half that multiple, something is wrong with your assumptions. Always cross-check absolute and relative valuations.

2. Using unrealistic growth assumptions

Projecting 20% annual growth for a decade is tempting but rarely realistic. High growth rates inevitably slow as companies mature. Use conservative, defensible assumptions and test your model with different scenarios.

3. Ignoring the discount rate

Small changes in the discount rate can dramatically change your valuation. Understand how WACC is calculated and why it matters. An incorrect discount rate will invalidate even the best cash flow projections.

4. Comparing across industries

A P/E ratio of 30 might be cheap for a high-growth technology company but expensive for a slow-growth utility. Always compare multiples within the same industry and account for differences in growth, risk, and capital intensity.

5. Anchoring to the current stock price

Effective valuation starts with fundamentals, not with the current price. If you begin by assuming the stock is worth roughly what it trades for, you introduce confirmation bias into every assumption.

6. Forgetting qualitative factors

Spreadsheets cannot capture management integrity, brand strength, regulatory risk, or industry disruption. The best analysts blend quantitative models with qualitative judgment.

Switching into finance from another field?

Our Switcher Program is designed for career changers who need to build credibility fast — no finance background required.

Stock Valuation FAQ

What is stock valuation in simple terms?

Stock valuation is the process of figuring out what a company’s stock is actually worth based on its financial performance and future potential. Analysts use methods like discounted cash flow (DCF) analysis and price-to-earnings (P/E) ratios to estimate a fair price. If the calculated value is higher than the market price, the stock may be a good buy. If it is lower, the stock could be overpriced.

What is the difference between absolute and relative valuation?

Absolute valuation estimates a stock’s intrinsic worth using the company’s own financial data, primarily cash flows, dividends, and growth rates. Relative valuation, by contrast, compares a stock to similar companies using ratios like P/E, EV/EBITDA, or price-to-book. Absolute methods tell you what a stock should be worth in isolation; relative methods tell you how it is priced compared to peers in the same industry.

What is the most common stock valuation method?

The price-to-earnings (P/E) ratio is the most widely used stock valuation method because it is simple to calculate and easy to understand. For deeper analysis, the discounted cash flow (DCF) method is considered the most theoretically sound because it values a company based on its projected future cash flows discounted to present value, rather than relying on what the market is currently willing to pay.

How do you know if a stock is overvalued or undervalued?

Compare the stock’s intrinsic value (calculated through DCF, DDM, or another absolute method) to its current market price. If intrinsic value exceeds the market price, the stock is undervalued. If the market price exceeds intrinsic value, it is overvalued. For relative valuation, compare the stock’s P/E, P/B, or EV/EBITDA multiples to industry averages. Significant deviations in either direction signal potential mispricing.

What is the stock valuation formula?

There is no single “stock valuation formula”; the formula depends on the method. The Gordon Growth Model (DDM) uses P = D1 / (r – g) where D1 is the expected dividend, r is the required return, and g is the growth rate. The DCF formula sums the present values of future cash flows: PV = CF / (1 + r)^n. Relative valuation uses ratios like P/E = Stock Price / Earnings Per Share. Each formula serves a different purpose.

Why is stock valuation important for career starters?

Stock valuation is a core skill tested in finance interviews and used daily by equity research analysts, investment bankers, and portfolio managers. Understanding how to value a stock demonstrates analytical ability and financial literacy, two qualities every hiring manager looks for. Building valuation models with real company data, as taught in the Valuation Master Class Starter Program, prepares candidates to perform from day one.

What is the best business valuation course?

The best business valuation course combines theory with hands-on practice using real company data. Valuation Master Class is designed by Dr. Andrew Stotz, a former #1-ranked equity analyst, and teaches DCF modeling, financial statement analysis, and equity research methods used by professional analysts. It offers programs for starters, career switchers, and experienced professionals looking to advance, making it one of the most comprehensive valuation courses online.

Ready to Take the Next Step?

Join 5,000+ finance professionals who’ve leveled up with Valuation Master Class.