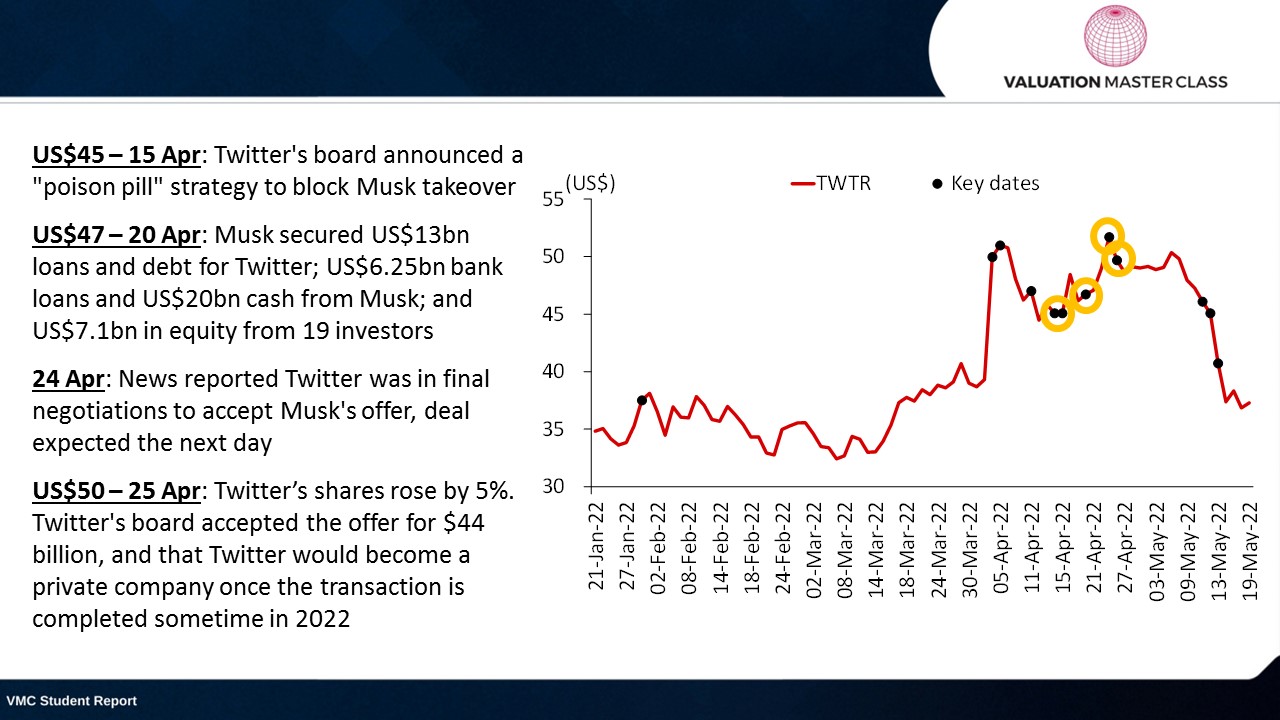

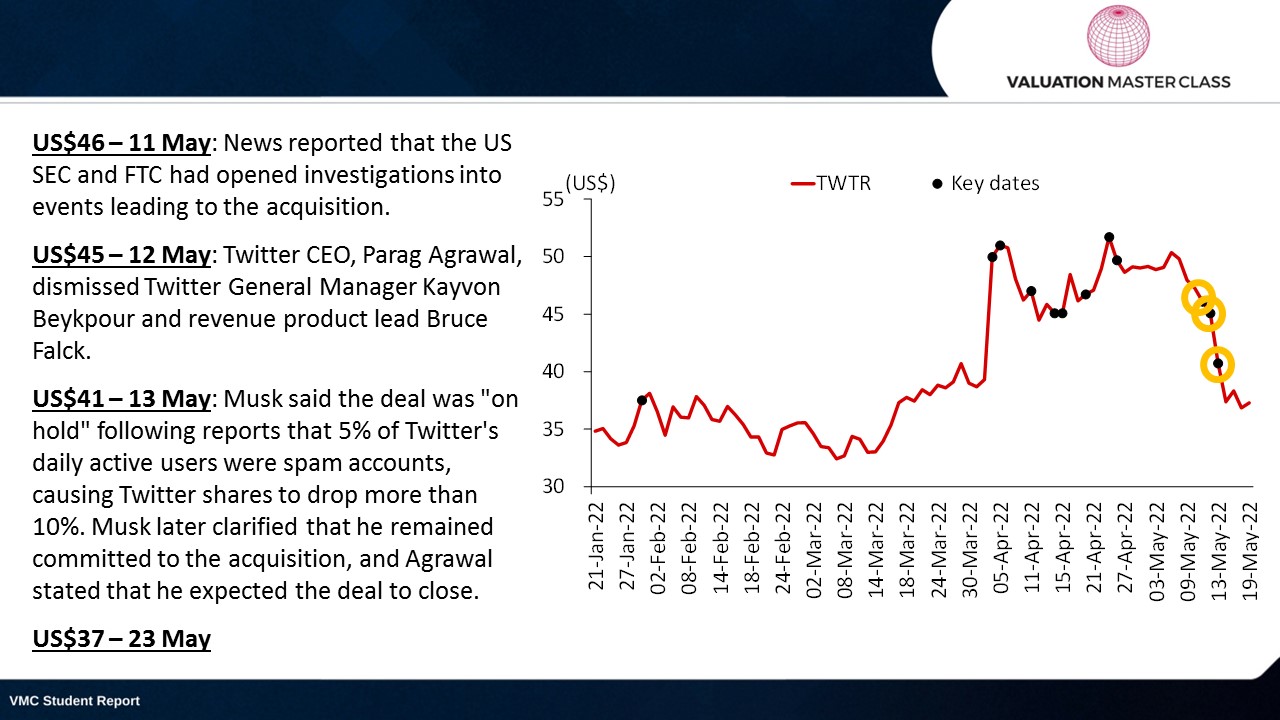

How J.P. Morgan Valued Twitter for the $44 Billion Musk Acquisition

How Do Investment Banks Value a Company for Acquisition?

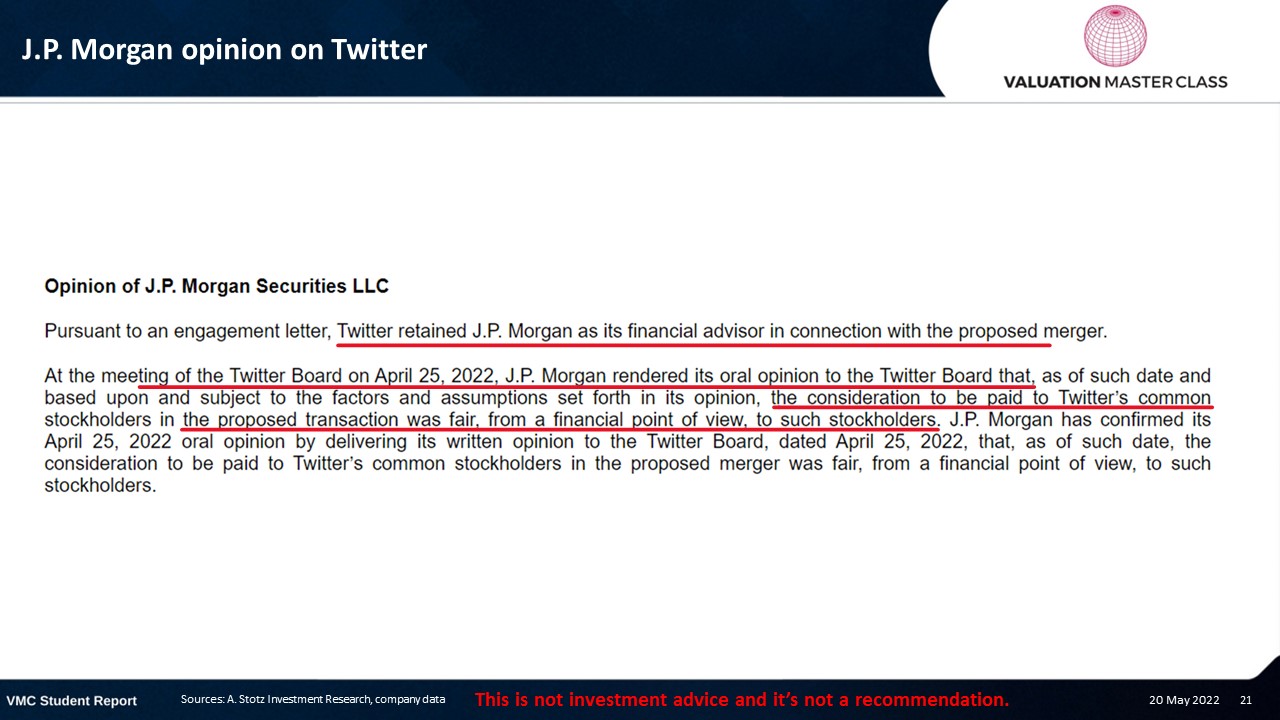

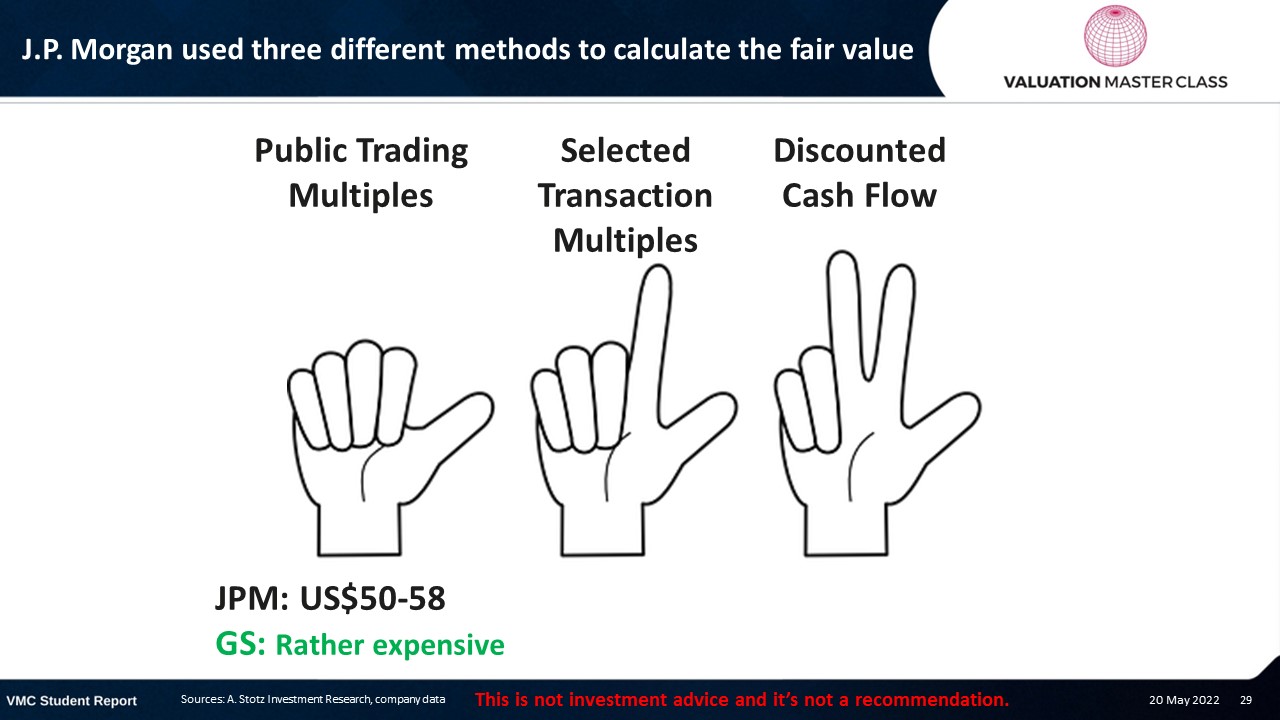

When Elon Musk offered to buy Twitter for $44 billion in 2022, Twitter’s board turned to J.P. Morgan and other advisors to determine whether the price was fair. Their analysis used three standard valuation methods that every finance professional should understand: public trading multiples, selected transaction multiples, and discounted cash flow (DCF) analysis.

This case study walks through each method using the actual data from Twitter’s Schedule 14A proxy statement, showing you how professionals apply these techniques to real companies. Whether you’re preparing for an analyst role, studying for the CFA exam, or evaluating your own investment ideas, the framework here applies to any acquisition scenario.

The three methods J.P. Morgan used:

- Public Trading Multiples: Comparing Twitter’s EV/EBITDA to peers like Meta, Alphabet, Snap, and Pinterest

- Selected Transaction Multiples: Analyzing precedent M&A deals in digital media

- Discounted Cash Flow (DCF): Projecting Twitter’s future free cash flows and discounting them to present value

Each method produced a different valuation range, and the final fairness opinion weighed all three. Here’s how they did it, and what you can learn from the process.

Starting your finance career?

If you are building your foundation in valuation and financial modeling, our Starter Program gives you the skills to land your first analyst role, including valuation, financial modeling, and interview preparation.

What’s Interesting About Twitter Is That it Makes a Better Toy for Elon Than an Investment?

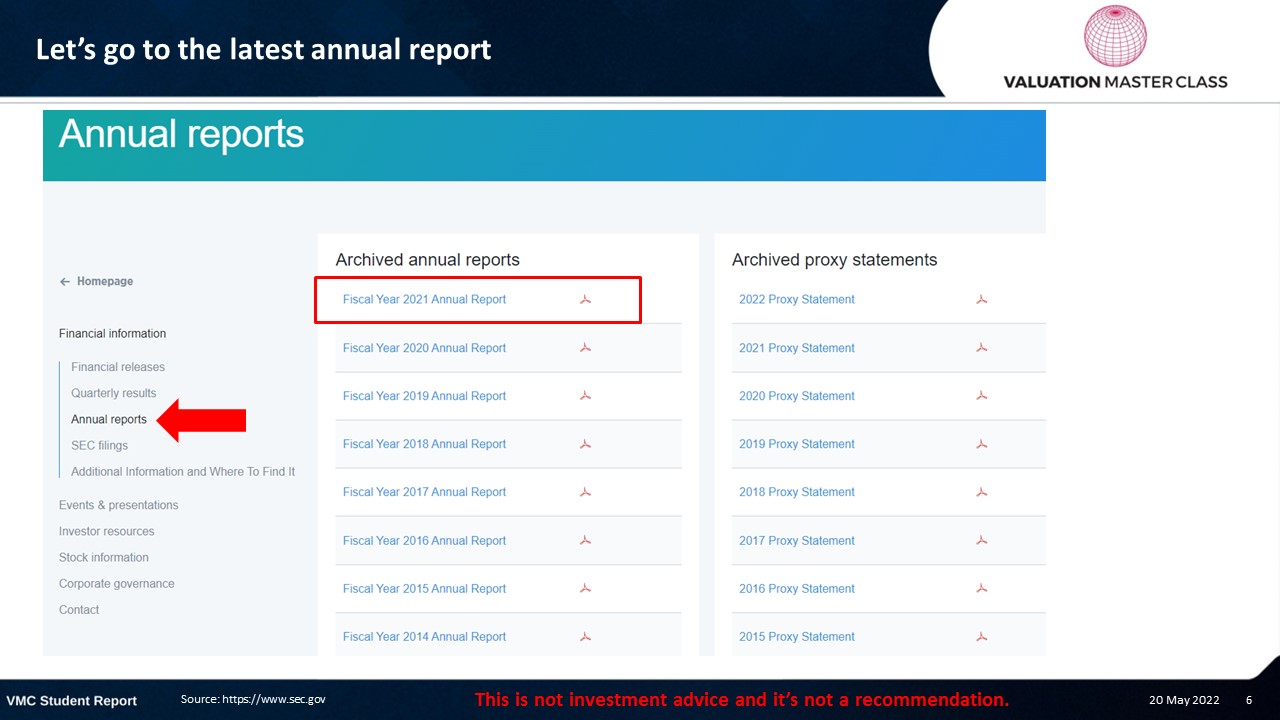

Let’s Go to the Latest Annual Report

Inside the Annual Report

- The Management’s Discussion and Analysis (MD&A) is a valuable section to get a brief overview of what the company is doing

- It also mentions the most recent developments in the company and industry

- Hence, it’s a great starting point to read

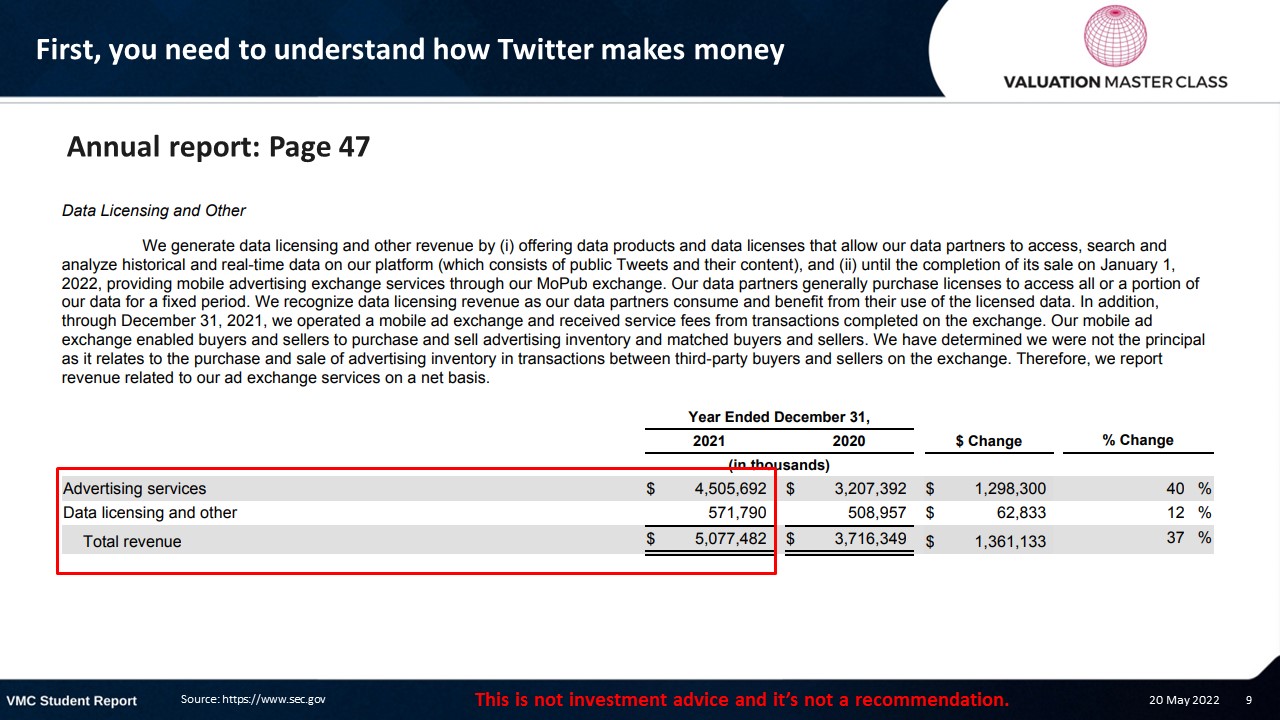

How Did Twitter Make Money? Understanding Its Revenue Model

Let’s Do a Revenue Breakdown of Twitter Together

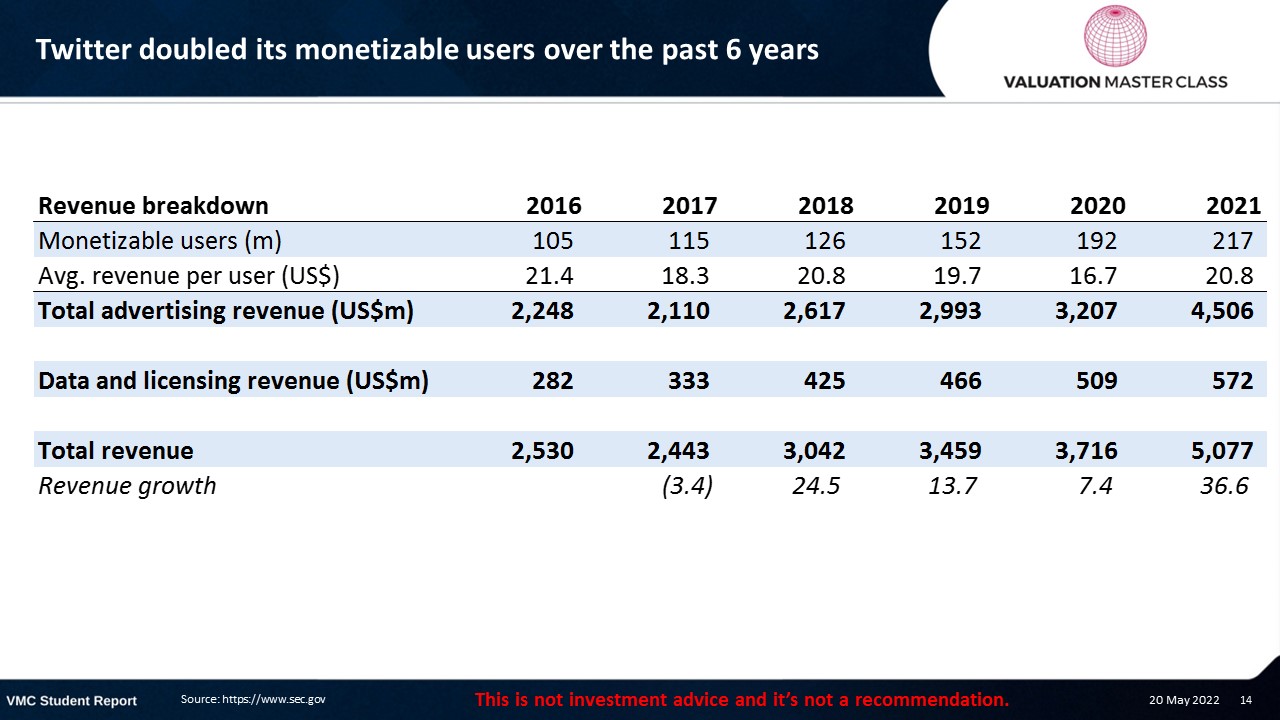

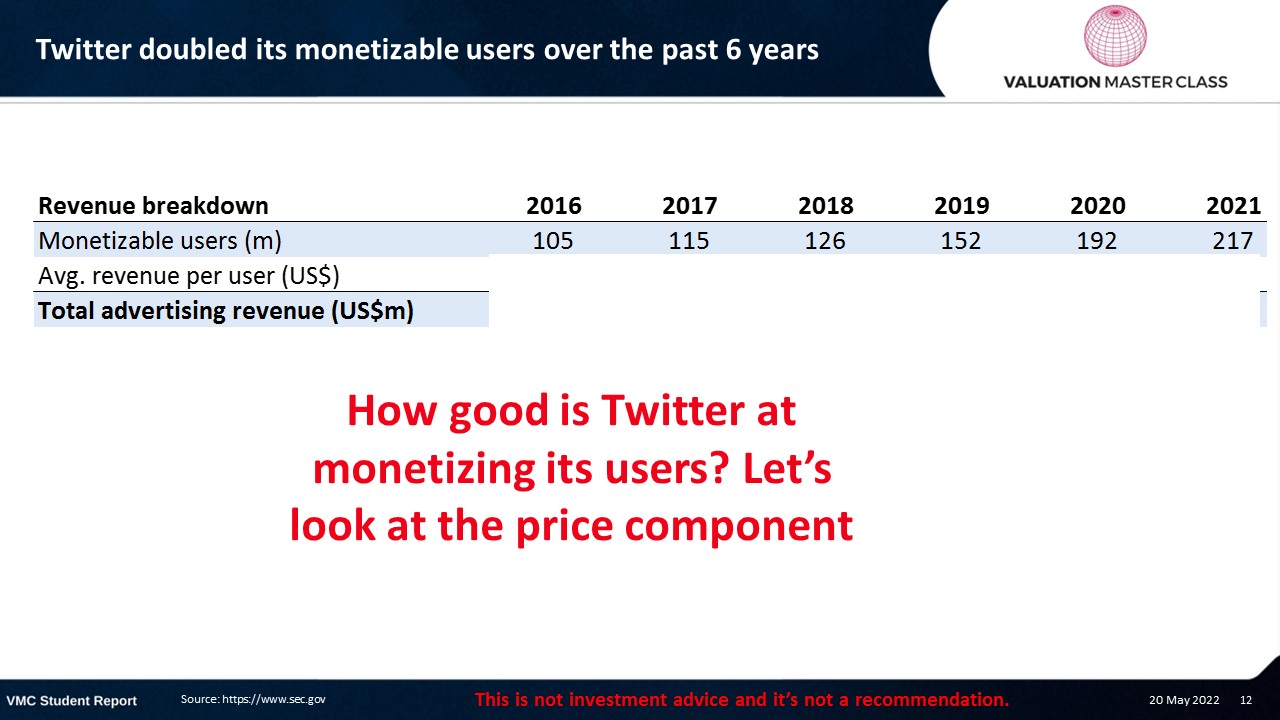

Main Driver of Twitter’s Revenue Is Quantity

Twitter Doubled Its Monetizable Users Over the Past 6 Years

Twitter Had Difficulties Getting More Money Out of Its Users

Start at the Company’s Website

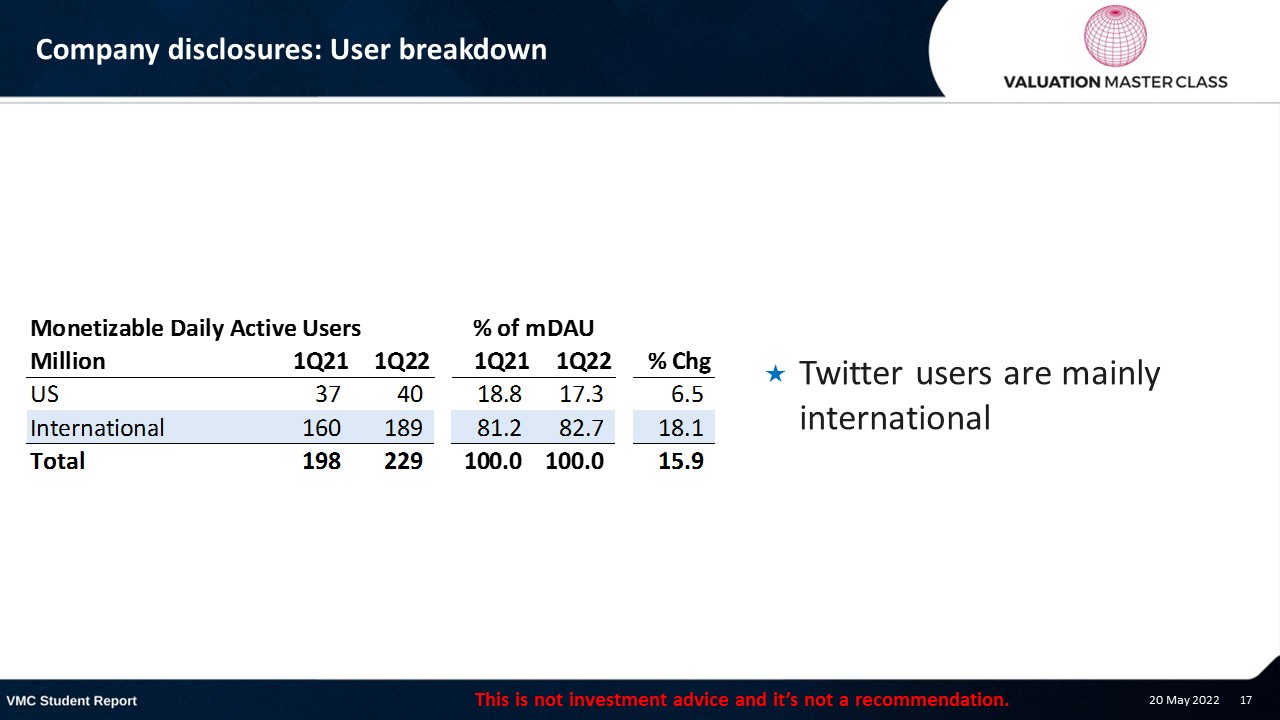

Company Disclosures: User Breakdown

- Twitter users are mainly international

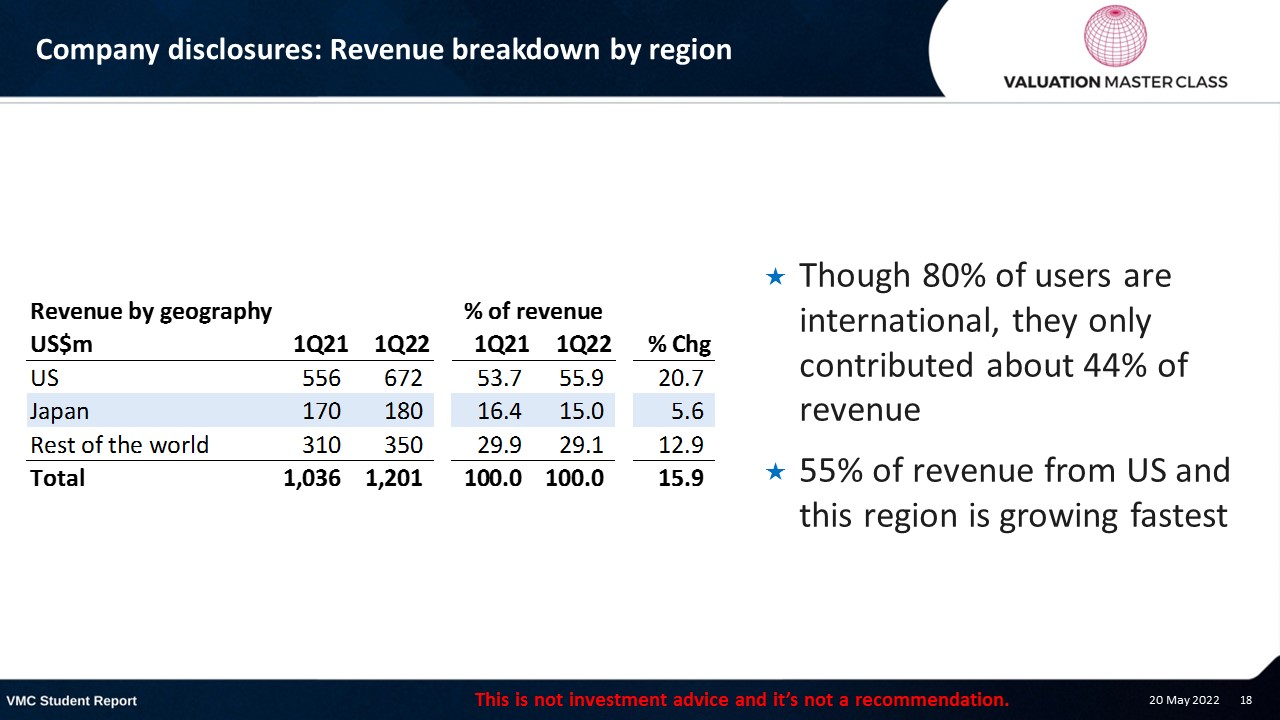

Company Disclosures: Revenue Breakdown by Region

- Though 80% of users are international, they only contributed about 44% of revenue

- 55% of revenue from the US, and this region is growing fastest

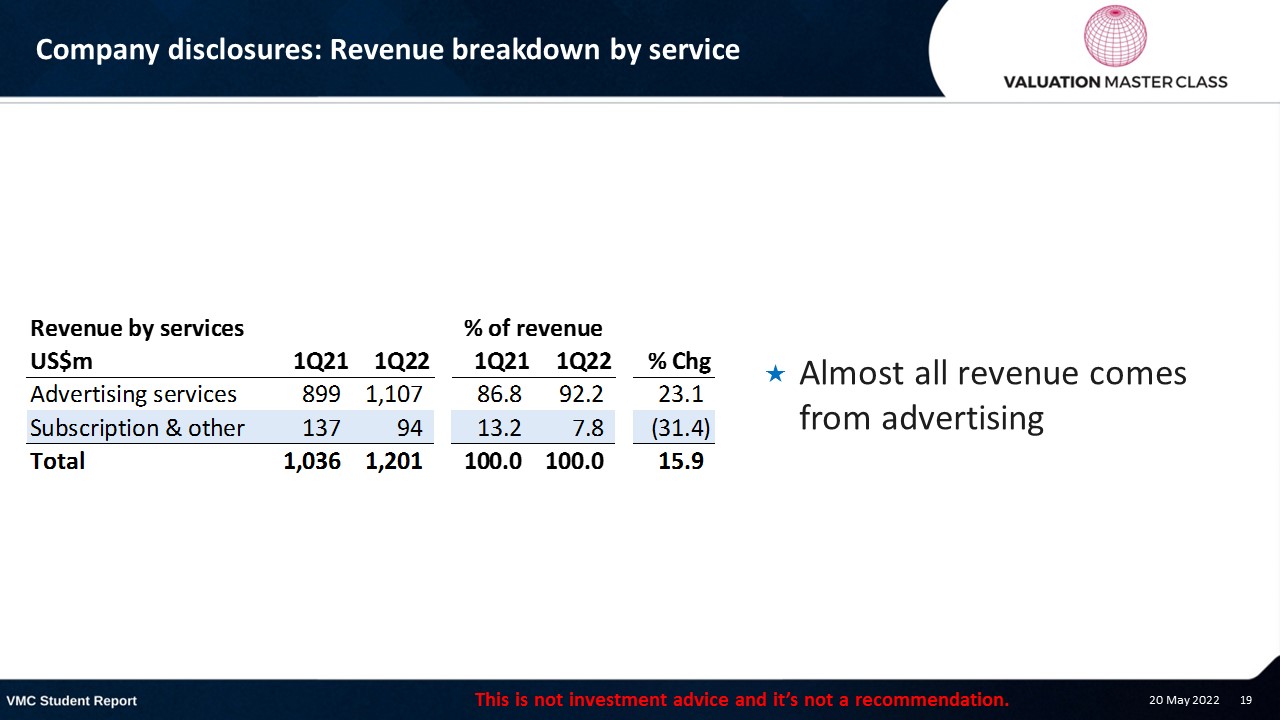

Company Disclosures: Revenue Breakdown by Service

- Almost all revenue comes from advertising

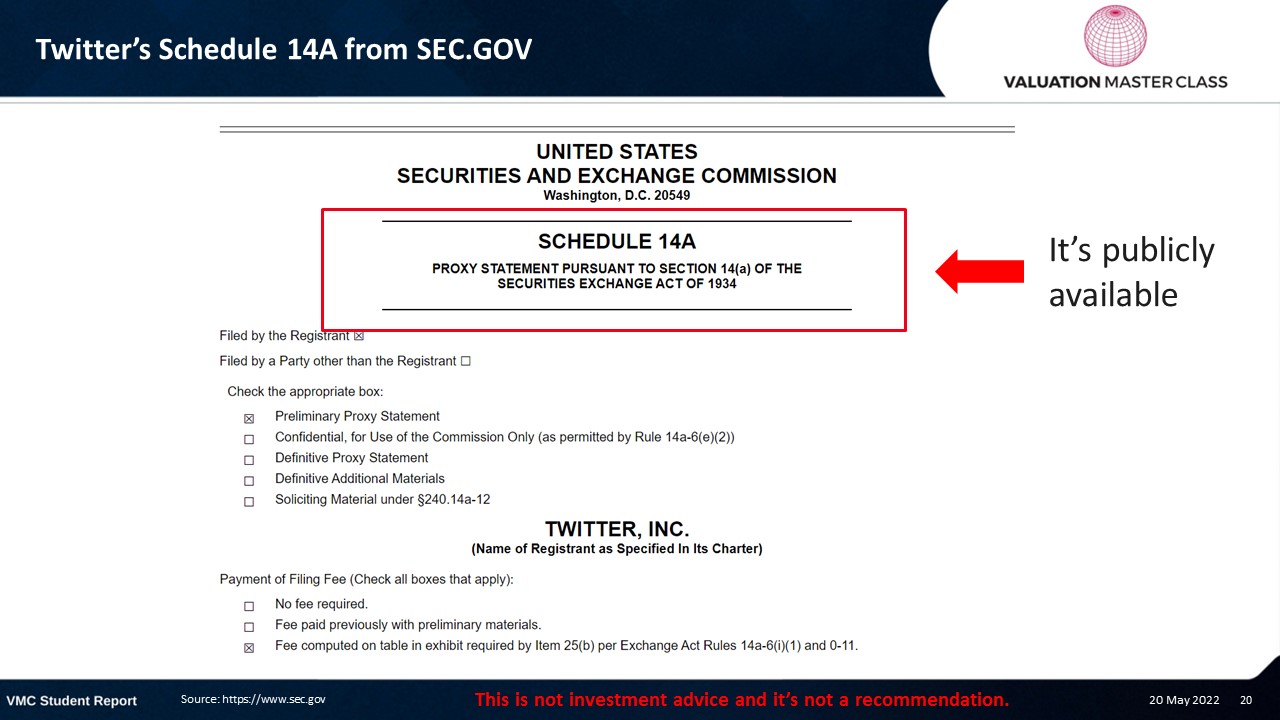

Twitter’s Schedule 14A from SEC.GOV

J.P. Morgan’s Opinion on Twitter

What Are the 3 Methods J.P. Morgan Used to Value Twitter?

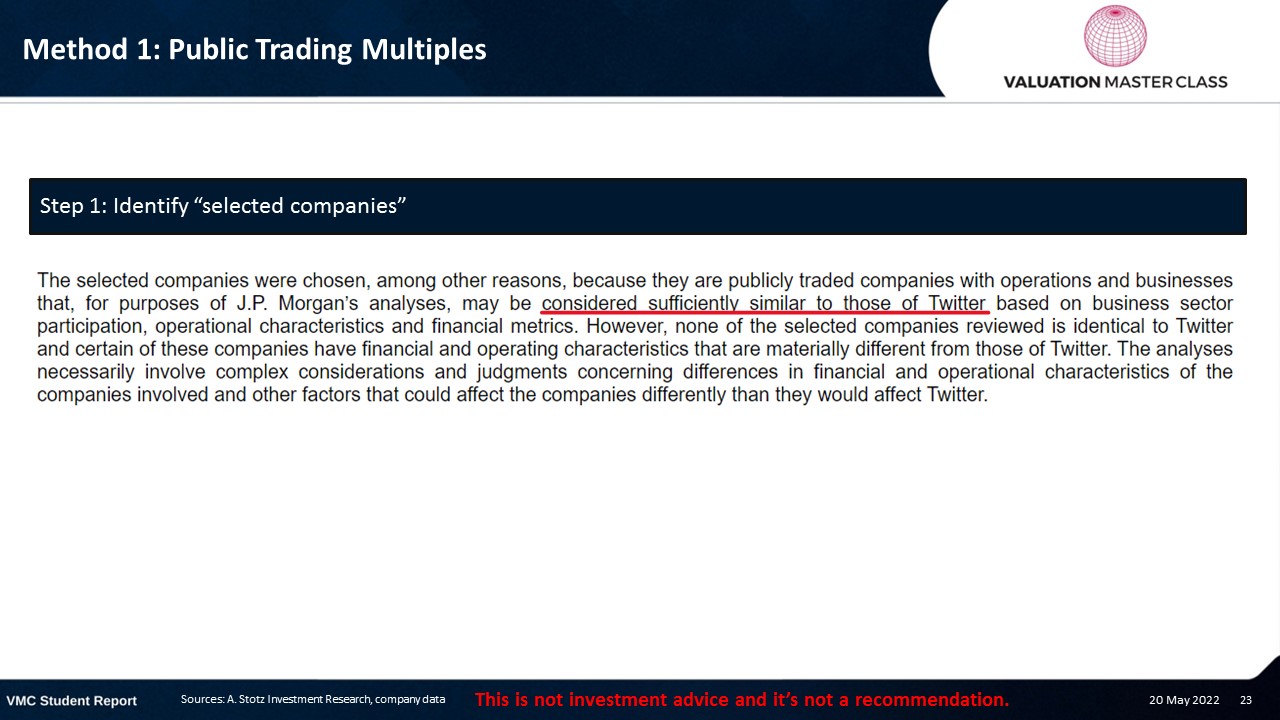

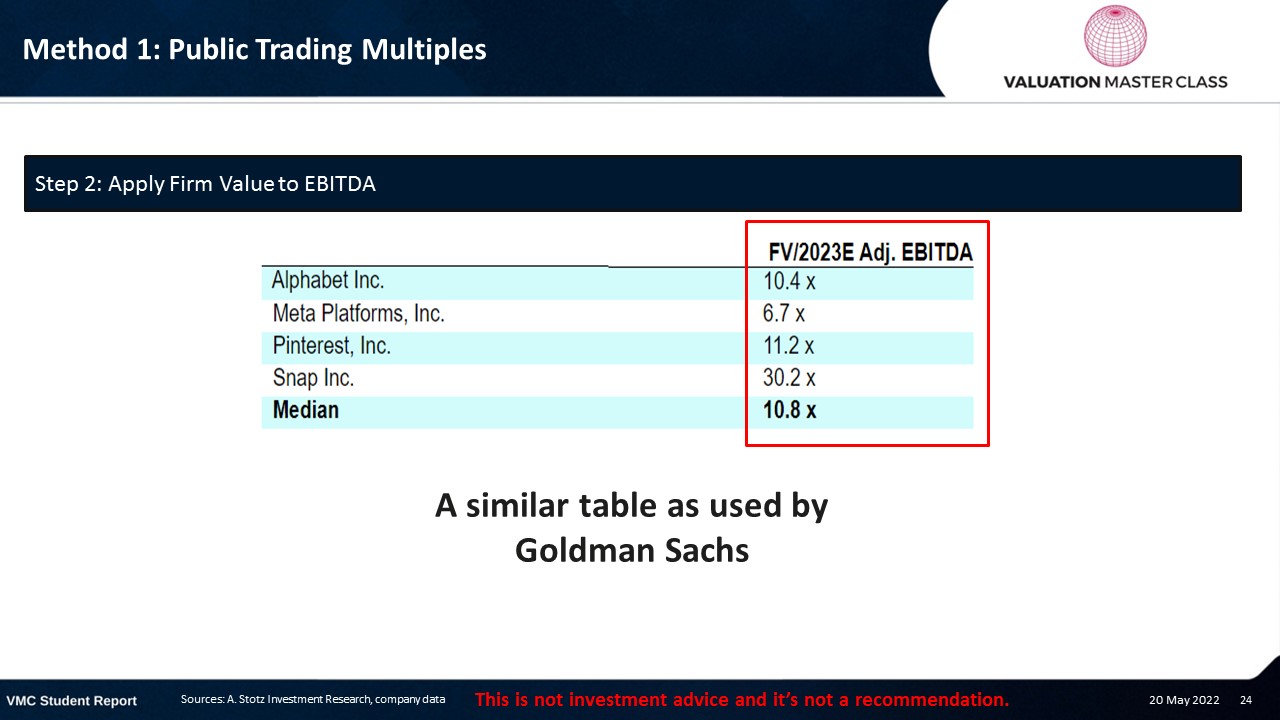

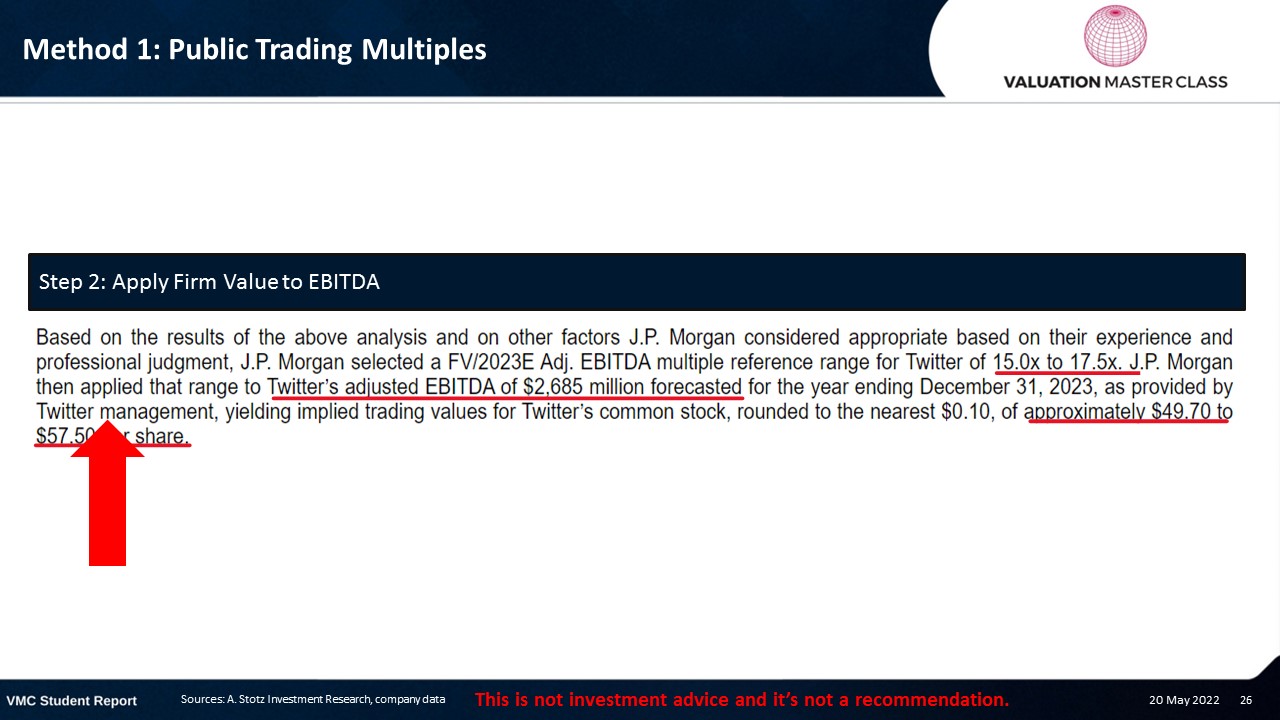

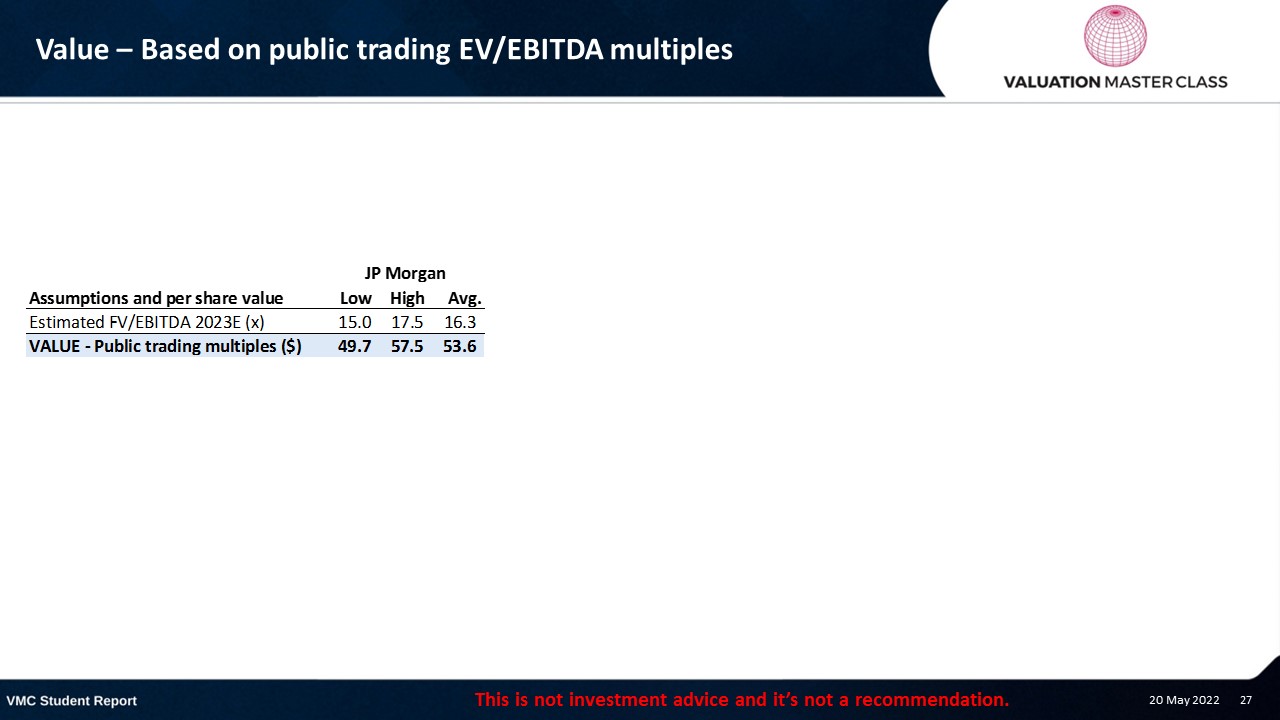

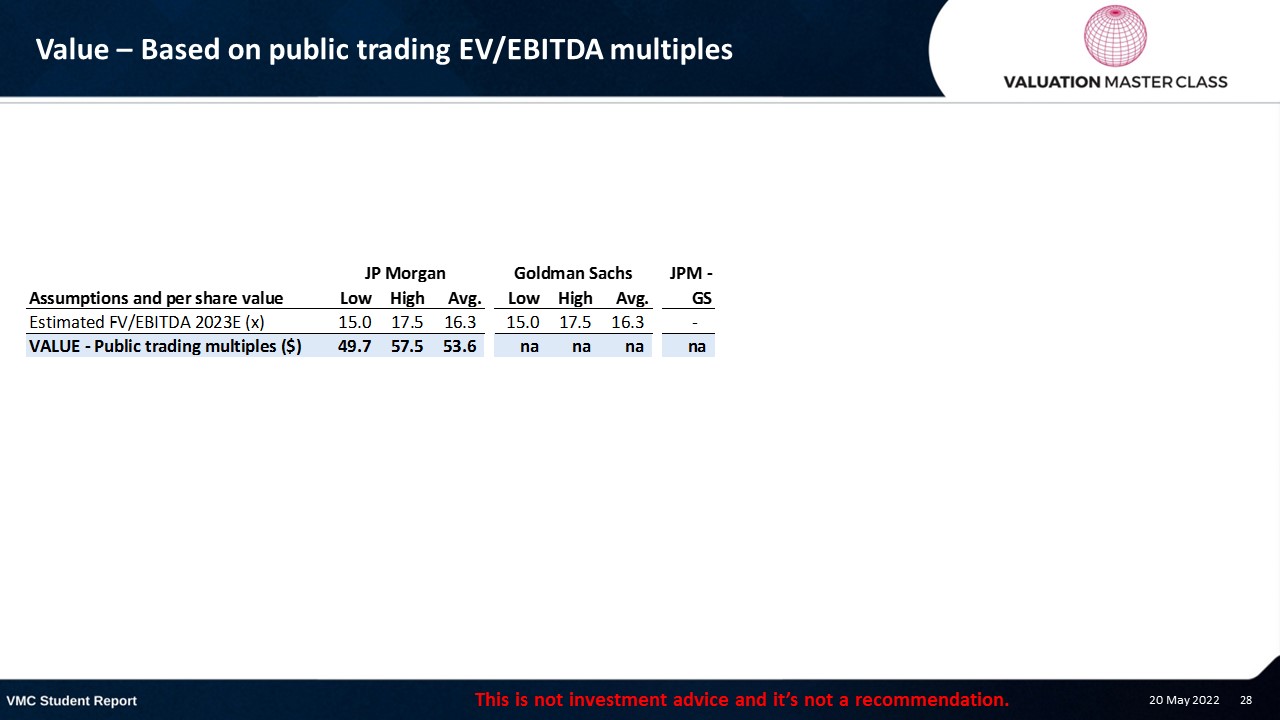

Method 1: Public Trading Multiples

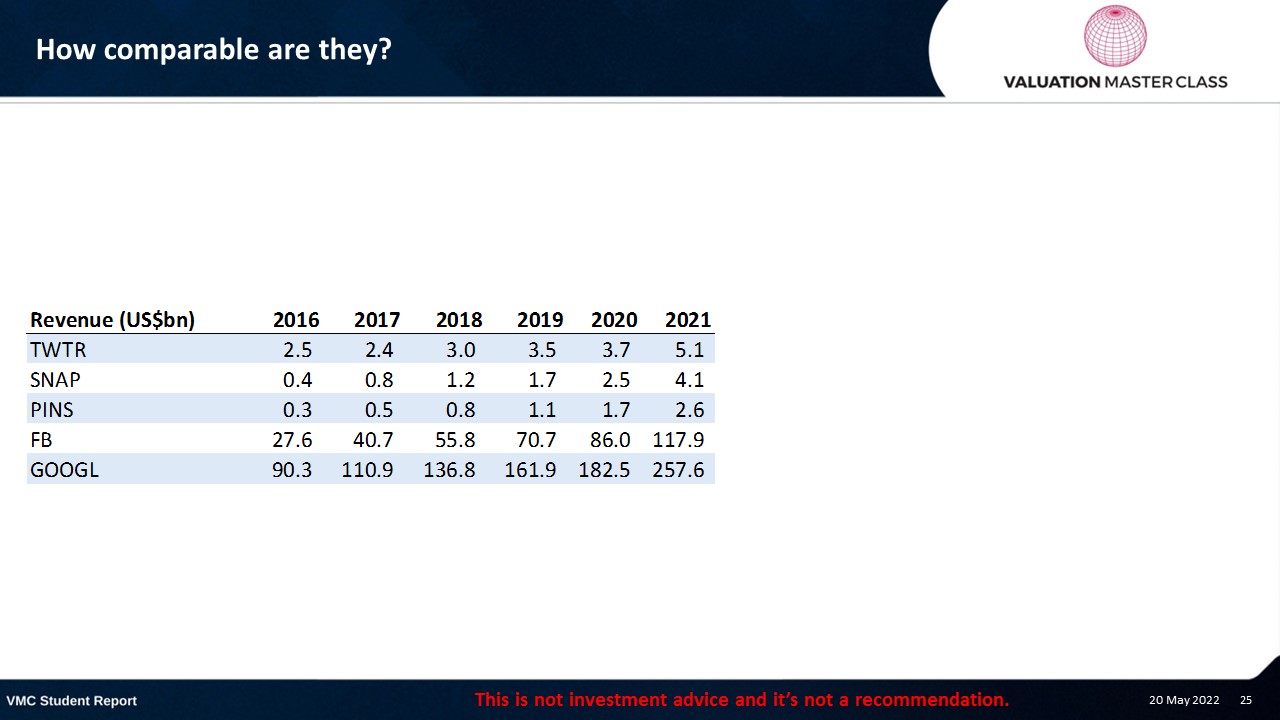

How Comparable Are They?

Value – Based on Public Trading EV/EBITDA Multiples

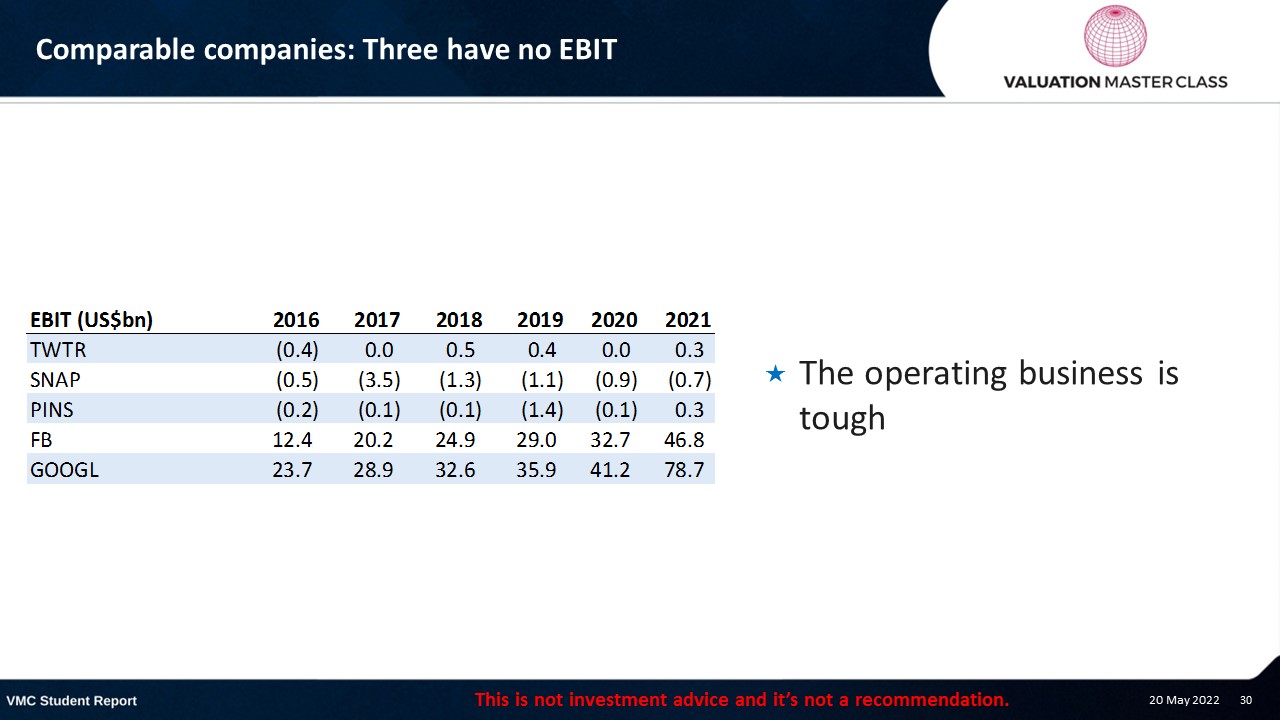

Comparable Companies: Three Have No EBIT

- The operating business is tough

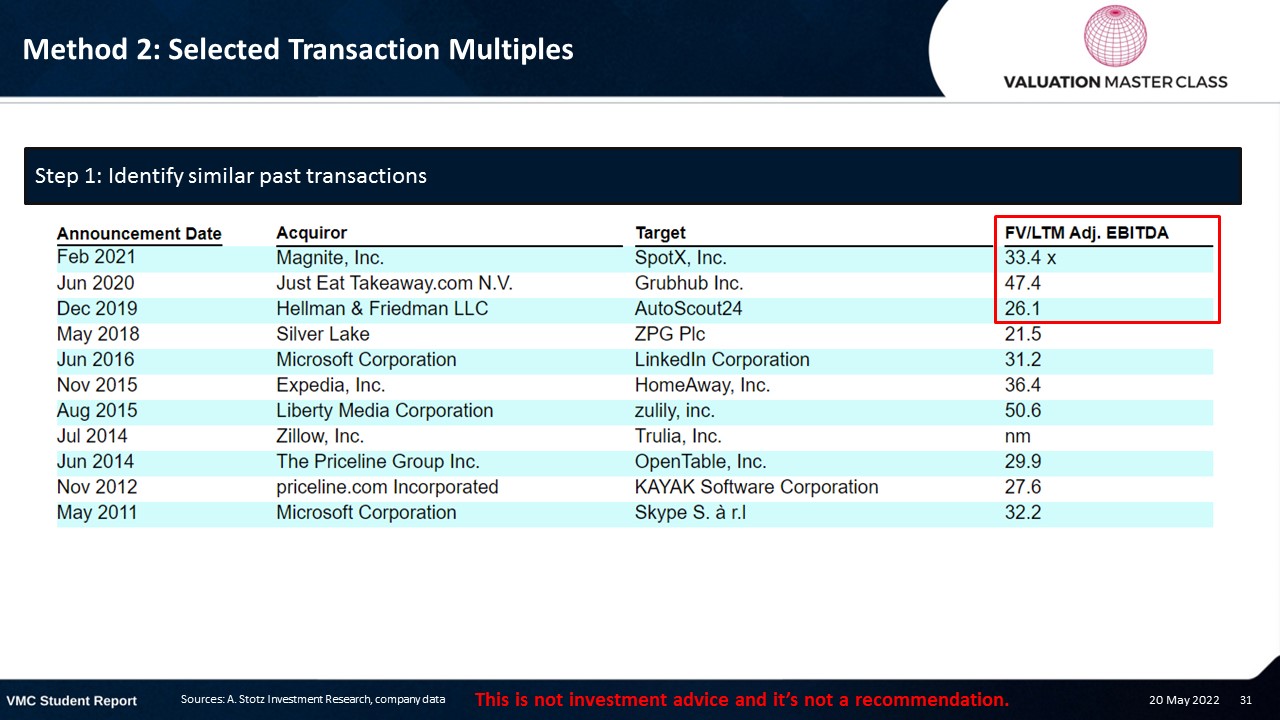

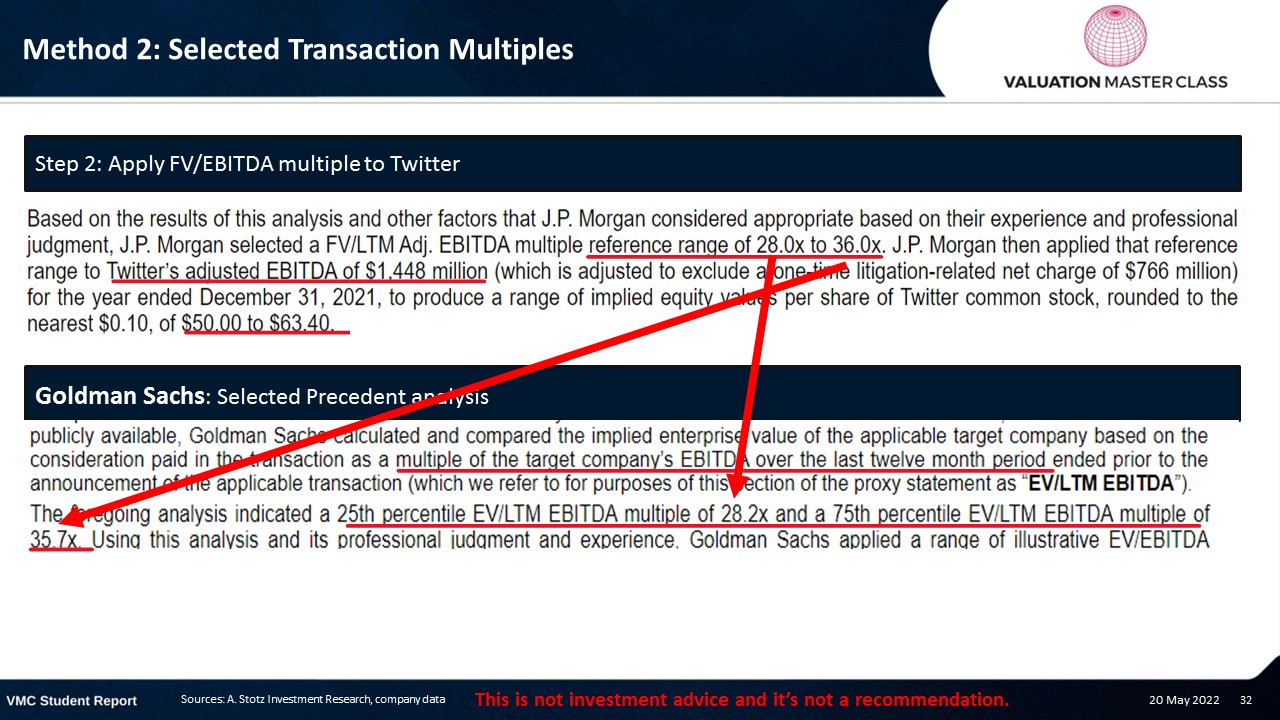

Method 2: Selected Transaction Multiples

Comparable Companies: Three Are Loss-Making

- 2018/9 Twitter made money

- 2018 US$0.845bn Inc. tax benefit (Release of valuation allowance from Brazil)

- 2019 Income tax benefit of US$1.2bn – Establishment of deferred tax assets from intra-entity transfer of intangible assets

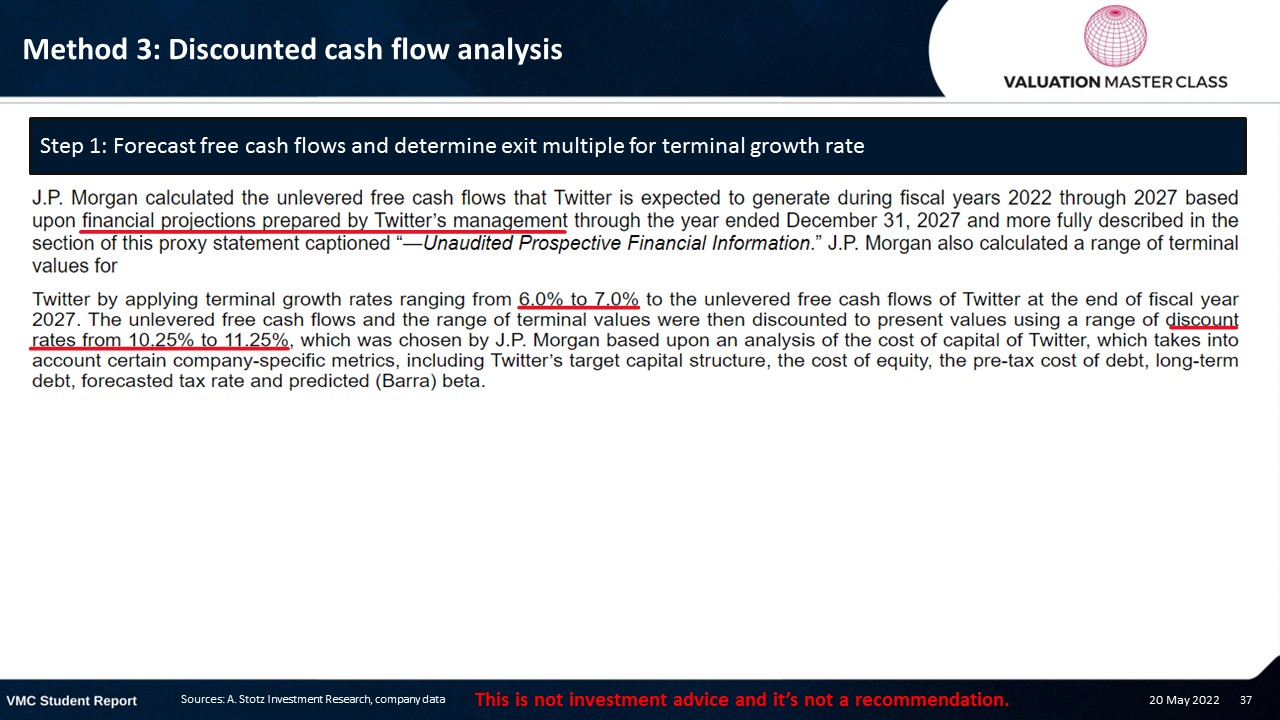

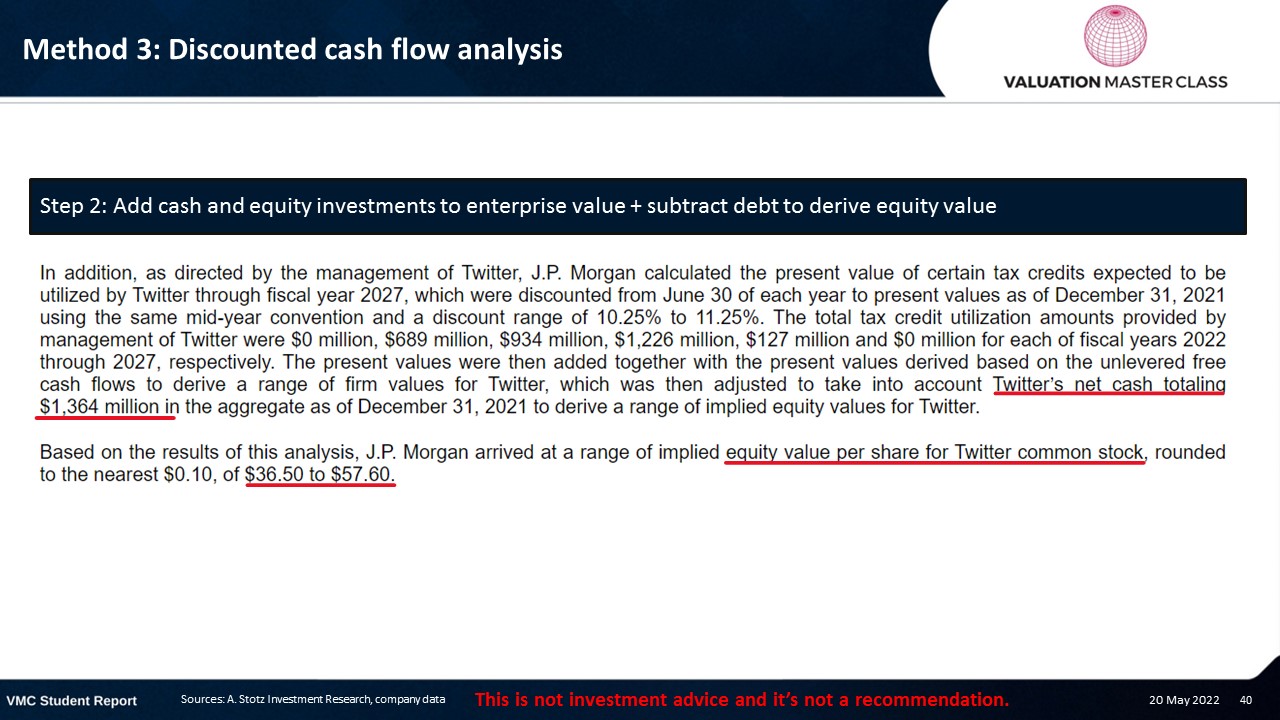

Method 3: Discounted Cash Flow Analysis

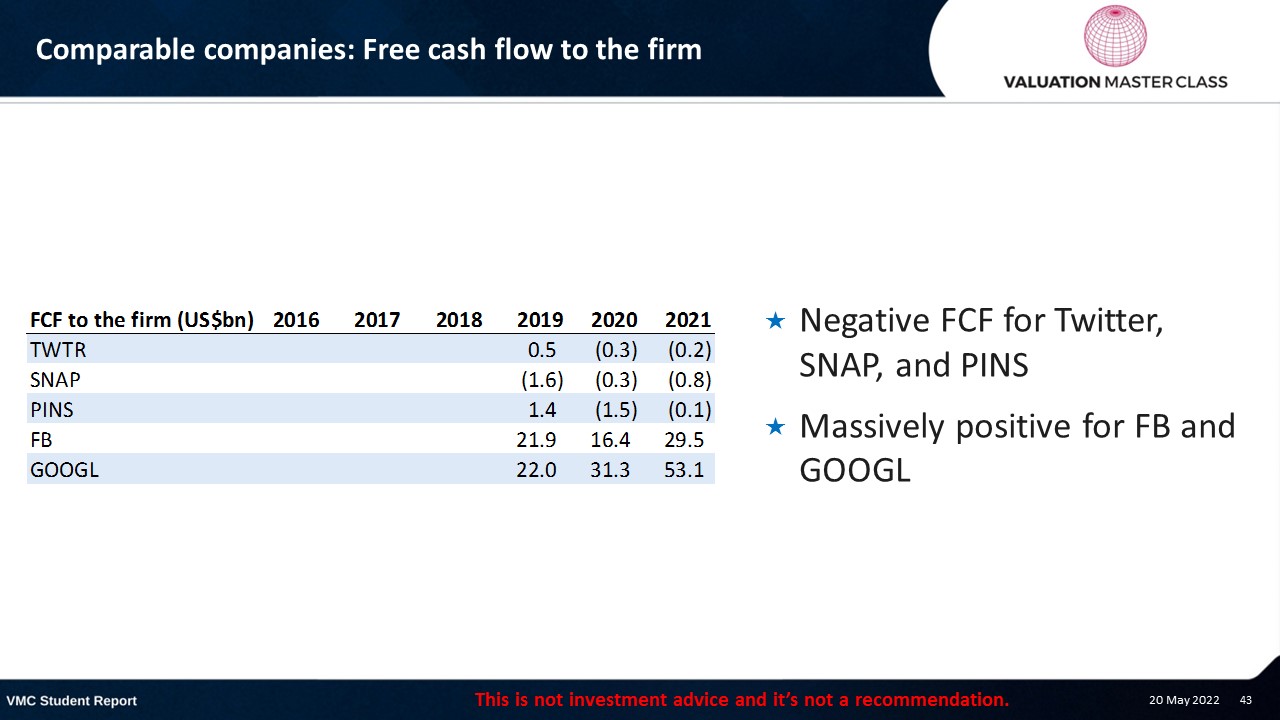

Comparable Companies: Free Cash Flow to the Firm

- Negative FCF for Twitter, SNAP, and PINS

- Massively positive for FB and GOOGL

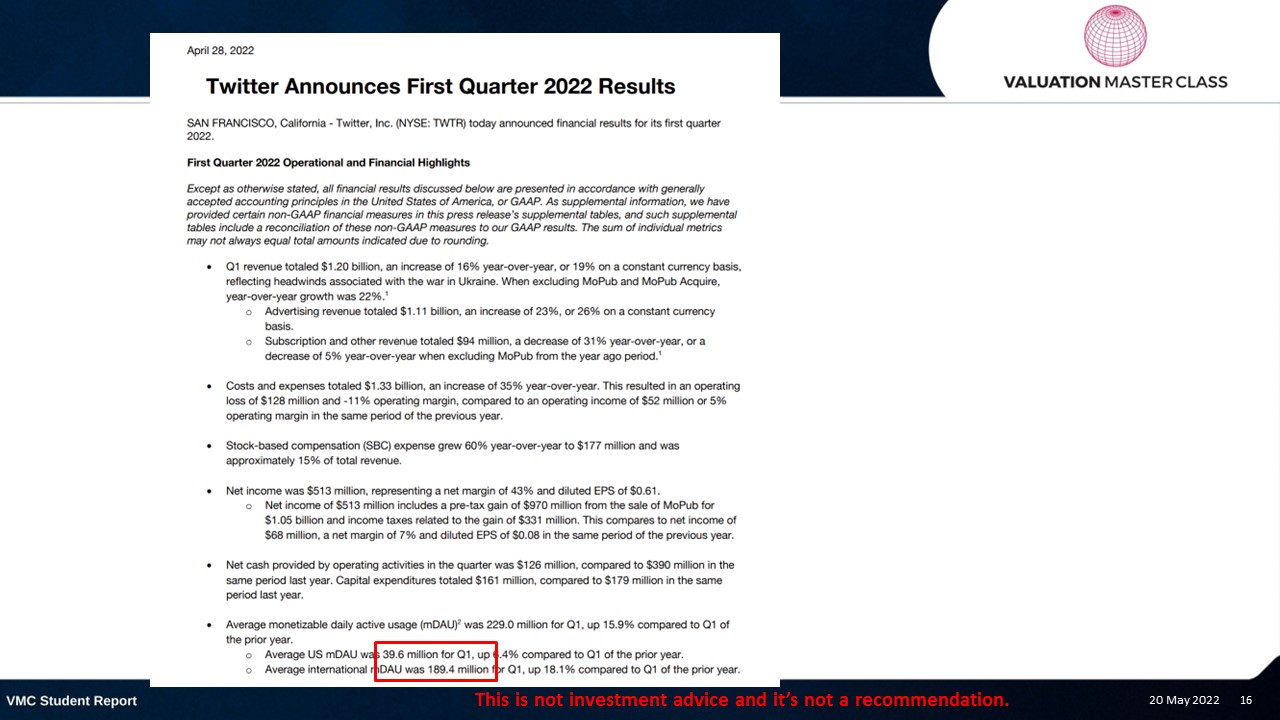

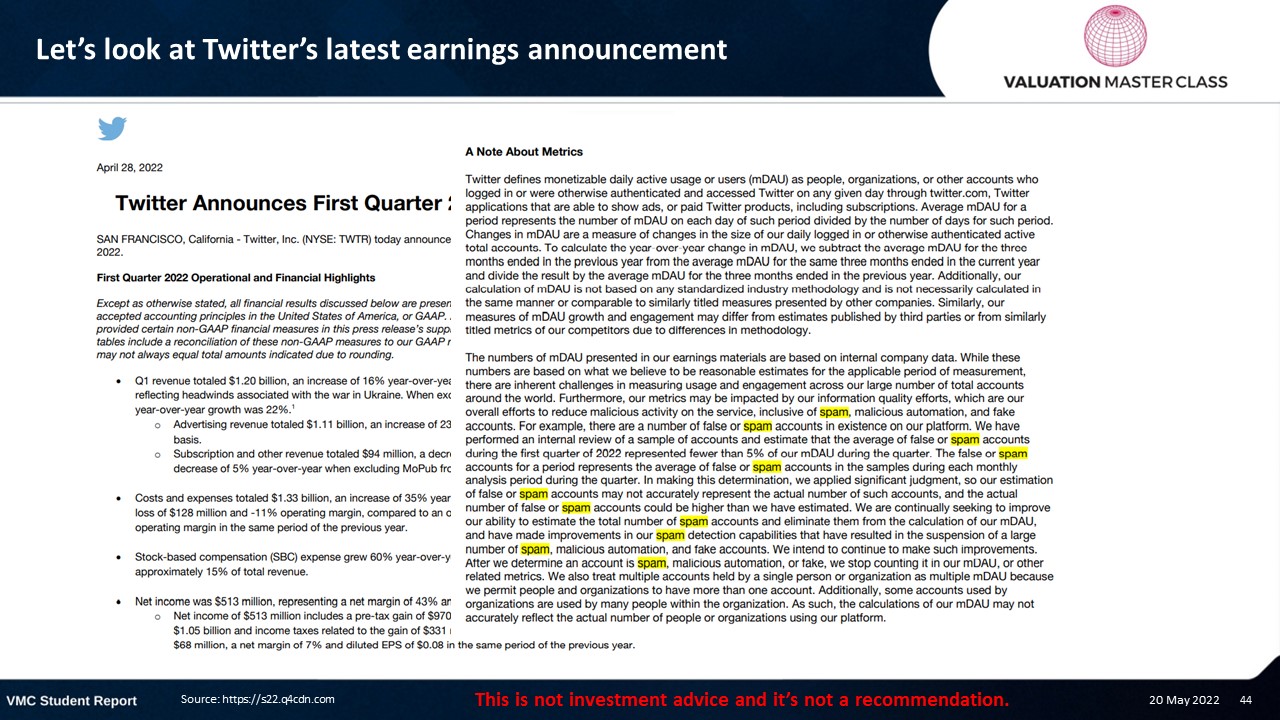

Let’s Look at Twitter’s Latest Earnings Announcement

False or Spam Accounts Discussion from 1Q22 Release

- “(…) there are a number of false or spam accounts in existence on our platform

- “We have performed an internal review of a sample of accounts and estimate that the average of false or spam accounts during the first quarter of 2022 represented fewer than 5% of our mDAU during the quarter.”

- “In making this determination, we applied significant judgment, so our estimation of false or spam accounts may not accurately represent the actual number of such accounts, and the actual number of false or spam accounts could be higher than we have estimated.”

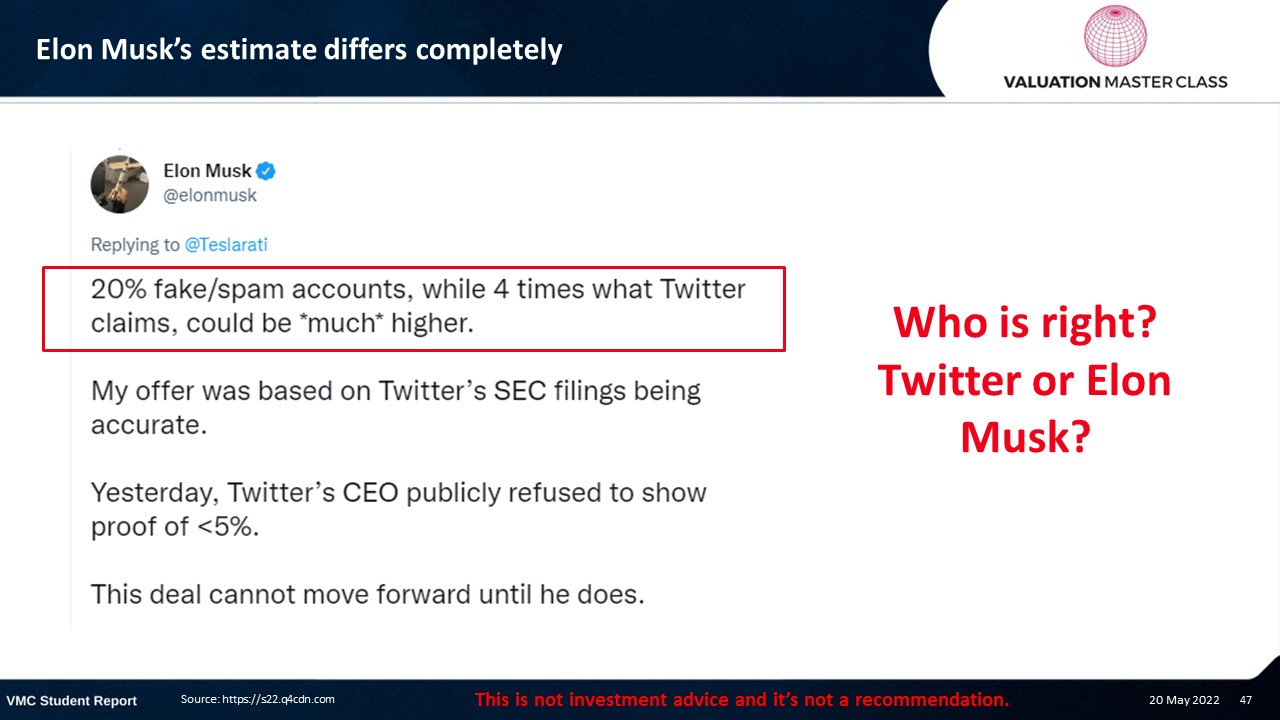

Elon Musk’s Estimate Differs Completely

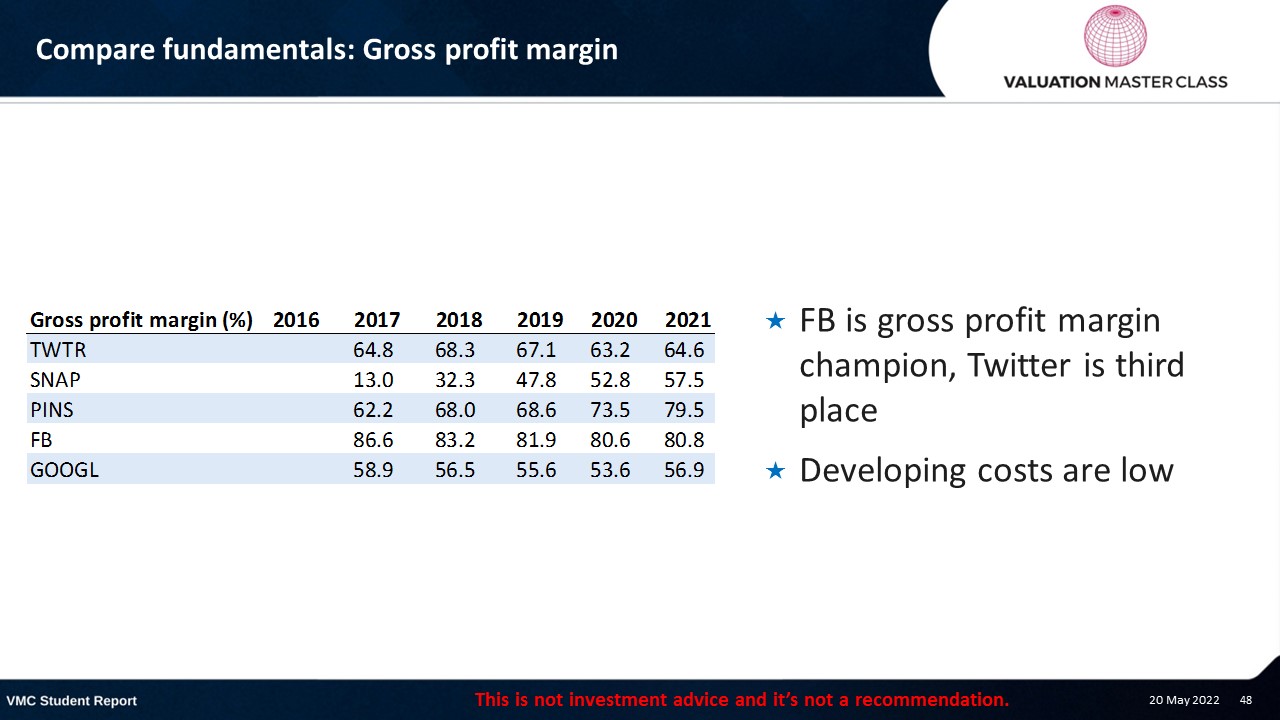

Compare Fundamentals: Gross Profit Margin

- FB is the gross profit margin champion, and Twitter is in third place

- Developing costs are low

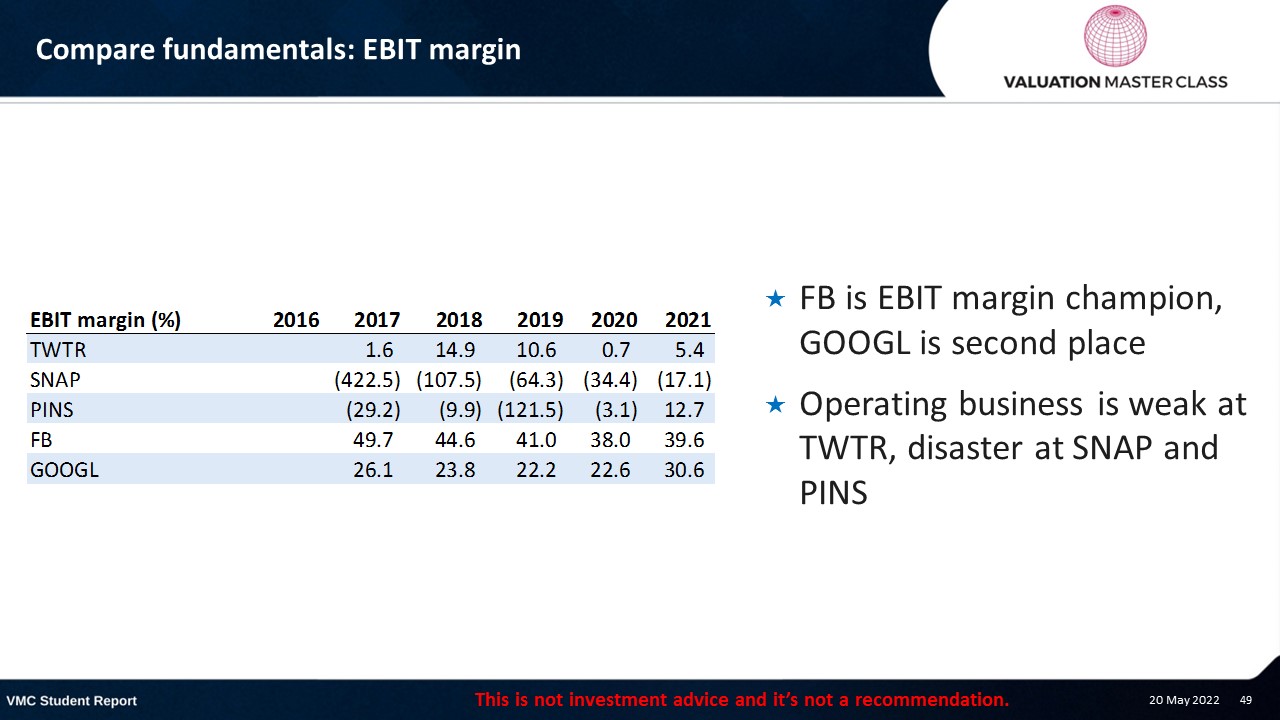

Compare Fundamentals: EBIT Margin

- FB is the EBIT margin champion, GOOGL is in second place

- Operating business is weak at TWTR, a disaster at SNAP, and PINS

Compare Fundamentals: Net margin

- SNAP has never made a profit, Twitter only in 2018 and 2019 because of tax adjustments

- FB and GOOGL are killing it

Compare Fundamentals: Free Cash Flow to the Firm

- SNAP is bleeding

- Twitter’s return to investors has been tiny

- FB and GOOGL are massive value generators

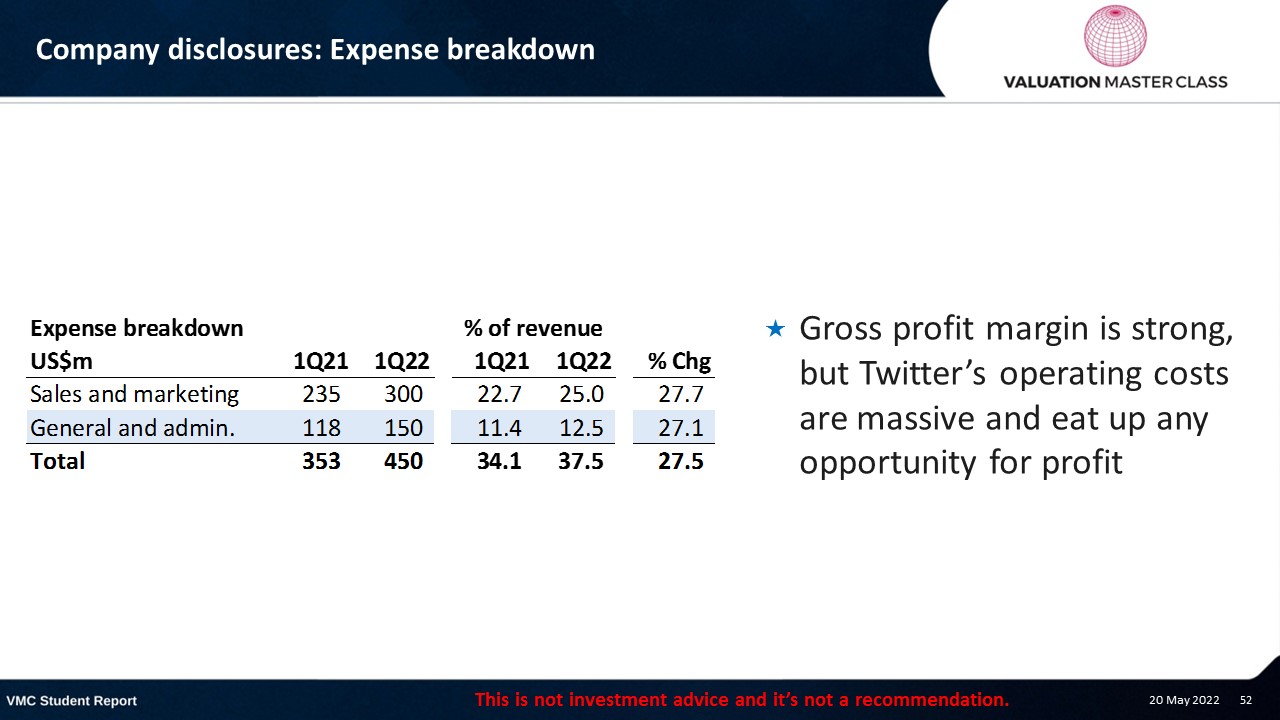

Company Disclosures: Expense Breakdown

- Gross profit margin is strong, but Twitter’s operating costs are massive and eat up any opportunity for profit

How to Apply This 3-Method Framework to Any Acquisition

Twitter’s valuation wasn’t unique in its methodology; J.P. Morgan used the same three-method approach that investment banks apply to virtually every major acquisition. Here’s how you can use the same framework:

Step 1: Build Your Comparable Company Set

Select 4-6 public companies that compete in the same market. For Twitter, J.P. Morgan chose Meta (Facebook), Alphabet (Google), Snap, and Pinterest. The key is finding companies with similar:

- Revenue models (advertising-driven)

- Growth profiles

- Market positioning

Watch out: Not all comparables are truly comparable. Three of Twitter’s comps had no EBIT, making EV/EBITDA comparisons unreliable. Always check whether your comps are profitable at the same level you’re analyzing.

Step 2: Select Your Multiples

The most common multiples for tech/media acquisitions are:

- EV/Revenue: Useful when companies are pre-profit

- EV/EBITDA: Standard for profitable companies

- EV/EBIT: Stricter, excludes depreciation adjustments

Apply the median and mean of your comp set to the target company’s financials. This gives you a valuation range, not a single number.

Step 3: Cross-Check with Precedent Transactions

Find M&A deals in the same sector from the past 3-5 years. Calculate what multiples acquirers actually paid. Transaction multiples are typically higher than public trading multiples because they include a control premium.

Step 4: Build a DCF as Your Anchor

While multiples tell you what the market thinks, DCF tells you what the company is intrinsically worth based on projected cash flows. Build a 5-year projection of free cash flow to the firm, apply a terminal value, and discount everything back at the appropriate WACC.

Step 5: Triangulate and Form a View

No single method gives you “the answer.” Professional valuations present a range of all three methods and form a judgment. In Twitter’s case:

- Public multiples suggested one range

- Transaction multiples suggested a higher range (reflecting control premium)

- DCF provided the fundamental anchor

The final fairness opinion synthesized all three. This triangulation approach is what separates professional analysis from back-of-envelope estimates.

Ready to advance?

If you already understand public multiples, transaction analysis, and DCF but want deeper practical valuation skills, the Advancer Program helps mid-career professionals sharpen their valuation skills and stand out for promotions or lateral moves into investment roles.

Common Mistakes When Valuing a Company for Acquisition

Based on the Twitter case and broader valuation practice, here are the pitfalls that trip up analysts:

- Using non-comparable comparables: Three of Twitter’s peer companies had no EBIT. Applying EBIT multiples from profitable companies to loss-making ones distorts the result. Always verify that your comps operate at the same profitability level.

- Ignoring the control premium: Public trading multiples reflect minority share prices. Acquisition valuations require a control premium (typically 20-40%) because the buyer gains full control. Failing to adjust means undervaluing the target.

- Conflating revenue growth with profit growth: Twitter doubled its user base over six years but couldn’t convert that growth into profit. Revenue growth without margin expansion doesn’t translate to value creation. Check the EBIT margin trend, not just the top line.

- Trusting management projections blindly: DCF models rely on future cash flow projections, which are inherently uncertain. Twitter’s bot/spam account disclosure showed that even basic user metrics can be disputed. Stress-test your assumptions.

- Using a single valuation method: Relying on only multiples or only DCF gives you a false sense of precision. The whole point of the three-method approach is to see where the ranges overlap; that convergence zone is your best estimate of fair value. For more on this, see our guide on common valuation mistakes.

Frequently Asked Questions About Twitter’s Valuation

How much did Elon Musk pay for Twitter?

Elon Musk acquired Twitter in October 2022 for approximately $44 billion, or $54.20 per share. The deal was structured as a leveraged buyout with Musk contributing personal equity and securing debt financing. Twitter’s board engaged J.P. Morgan to issue a fairness opinion confirming the offer price was within a reasonable range based on public multiples, transaction multiples, and DCF analysis.

What valuation methods did J.P. Morgan use for Twitter?

J.P. Morgan used three standard methods: public trading multiples (comparing Twitter’s EV/EBITDA and EV/Revenue to Meta, Alphabet, Snap, and Pinterest), selected transaction multiples (analyzing precedent M&A deals in digital media), and discounted cash flow analysis (projecting Twitter’s future free cash flows). Each method produced a different valuation range, and the fairness opinion weighed all three to determine whether Musk’s $54.20 per share offer was fair.

Was Twitter profitable before the Musk acquisition?

Barely. Twitter was only profitable in 2018 and 2019, and some of that profitability came from tax adjustments rather than operating improvements. Its gross profit margins were strong, but massive operating costs, particularly in R&D and sales, consumed nearly all the margin. Compared to peers, Meta and Alphabet generated vastly higher EBIT and net margins, while Twitter’s profitability was closer to Pinterest’s and well above Snapchat’s consistent losses.

What is a fairness opinion in M&A?

A fairness opinion is an independent assessment by an investment bank confirming that an acquisition price is fair to shareholders from a financial perspective. It’s required in most public company acquisitions and is filed as part of the SEC proxy statement (Schedule 14A). The opinion is based on multiple valuation methods and protects the board from allegations that they sold the company too cheaply.

How do you choose comparable companies for a valuation?

Select companies that share the same industry, revenue model, growth profile, and market position as the target. For Twitter, J.P. Morgan chose Meta, Alphabet, Snap, and Pinterest, all advertising-driven social platforms. The challenge is that no two companies are identical. In Twitter’s case, three of four comparables had no EBIT, making certain multiples unreliable. The key is acknowledging comparability limitations and adjusting accordingly.

What can I learn from the Twitter acquisition about valuation?

The Twitter case demonstrates three critical lessons: (1) always use multiple valuation methods rather than relying on a single approach, (2) check whether your comparable companies are truly comparable at the metric level you’re analyzing, and (3) revenue growth without profit growth does not create shareholder value. These principles apply to any company valuation, not just M&A. You can learn to apply these methods hands-on through the Valuation Master Class Boot Camp.

Switching into finance from another field?

If you are transitioning into finance and need structured credibility building, our Switcher Program is designed for career changers who need to build practical valuation skills fast, even without a finance background.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.

Ready to Take the Next Step?

Join 5,000+ finance professionals who’ve leveled up with Valuation Master Class.