Can Carnival Sail Safely through the Hurricane?

What’s interesting about Carnival is that its debt has swollen by 200% compared to pre-pandemic level

Download the full report as a PDF

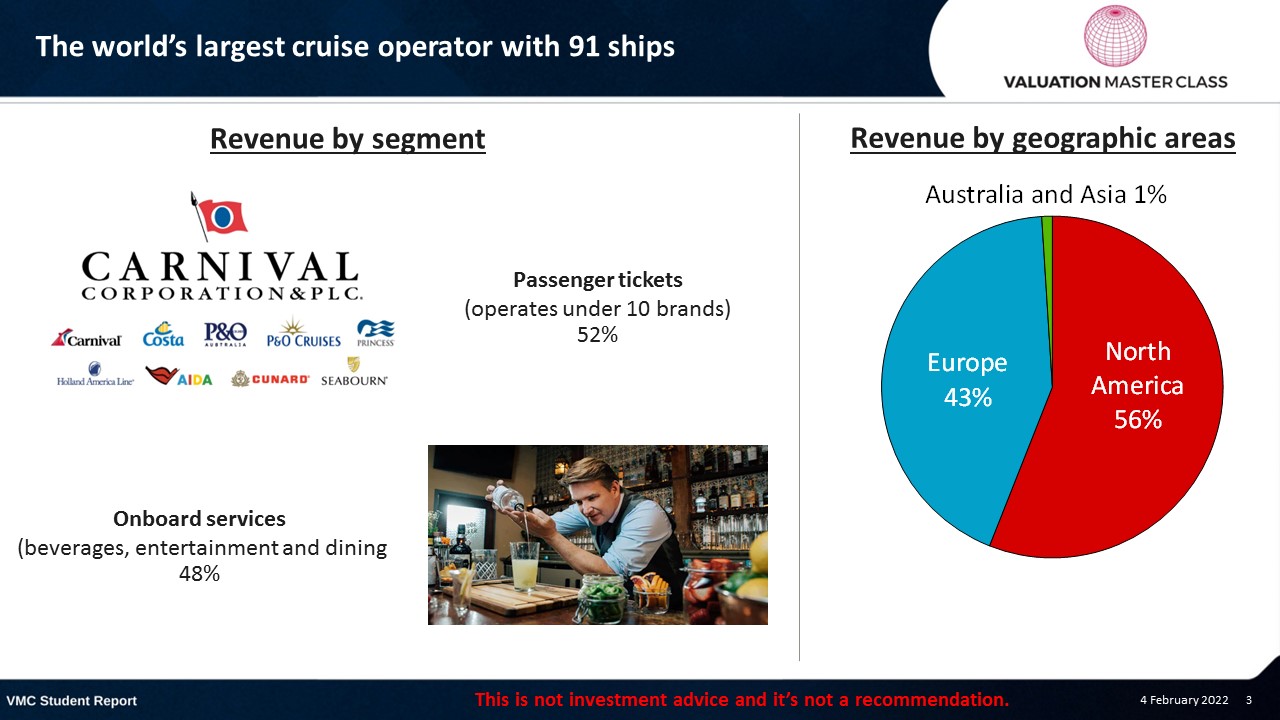

The world’s largest cruise operator with 91 ships

External events caused Carnival to struggle

- Carnival continues to face a tough recovery

- Due to the pandemic it had to stop its operations, while costs remained high

- On top of that, people might continue to avoid large crowds during holidays

- The outbreak of the Russian war led to additional cost pressures

- Fuel price have surged massively, which should result in further net losses during 2Q22 and onwards

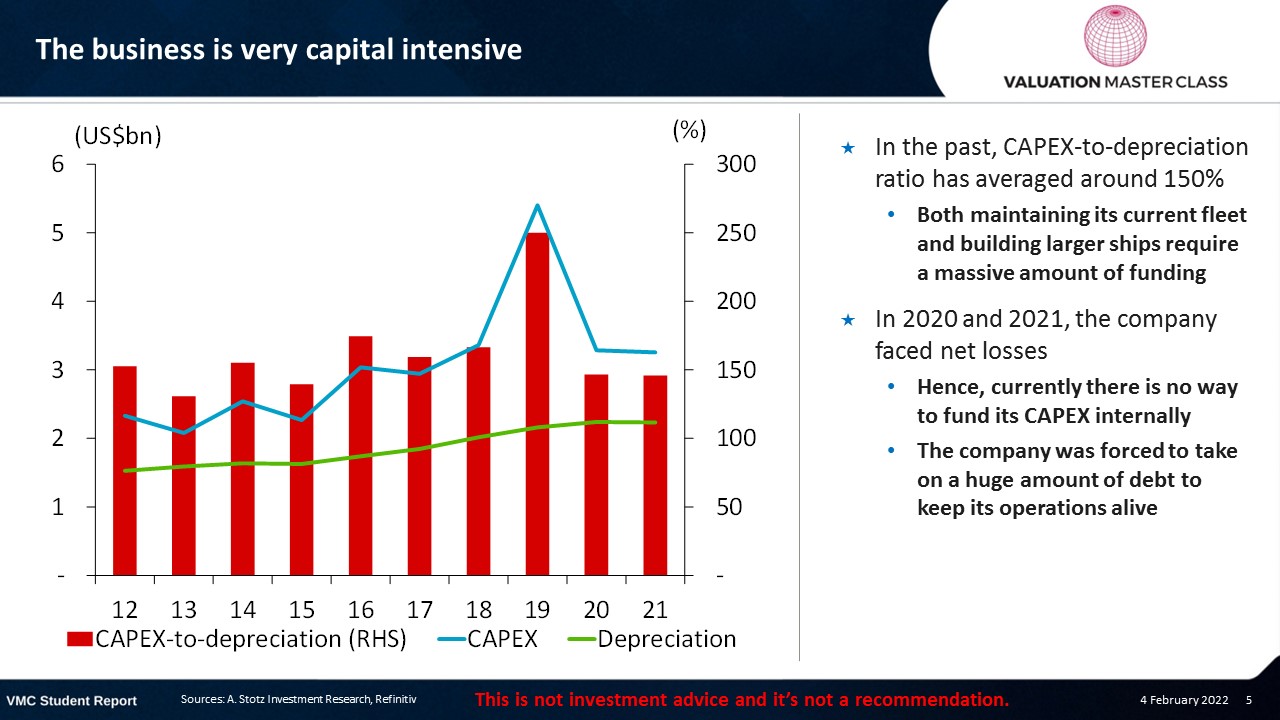

The business is very capital intensive

- In the past, CAPEX-to-depreciation ratio has averaged around 150%

- Both maintaining its current fleet and building larger ships require a massive amount of funding

- In 2020 and 2021, the company faced net losses

- Hence, currently there is no way to fund its CAPEX internally

- The company was forced to take on a huge amount of debt to keep its operations alive

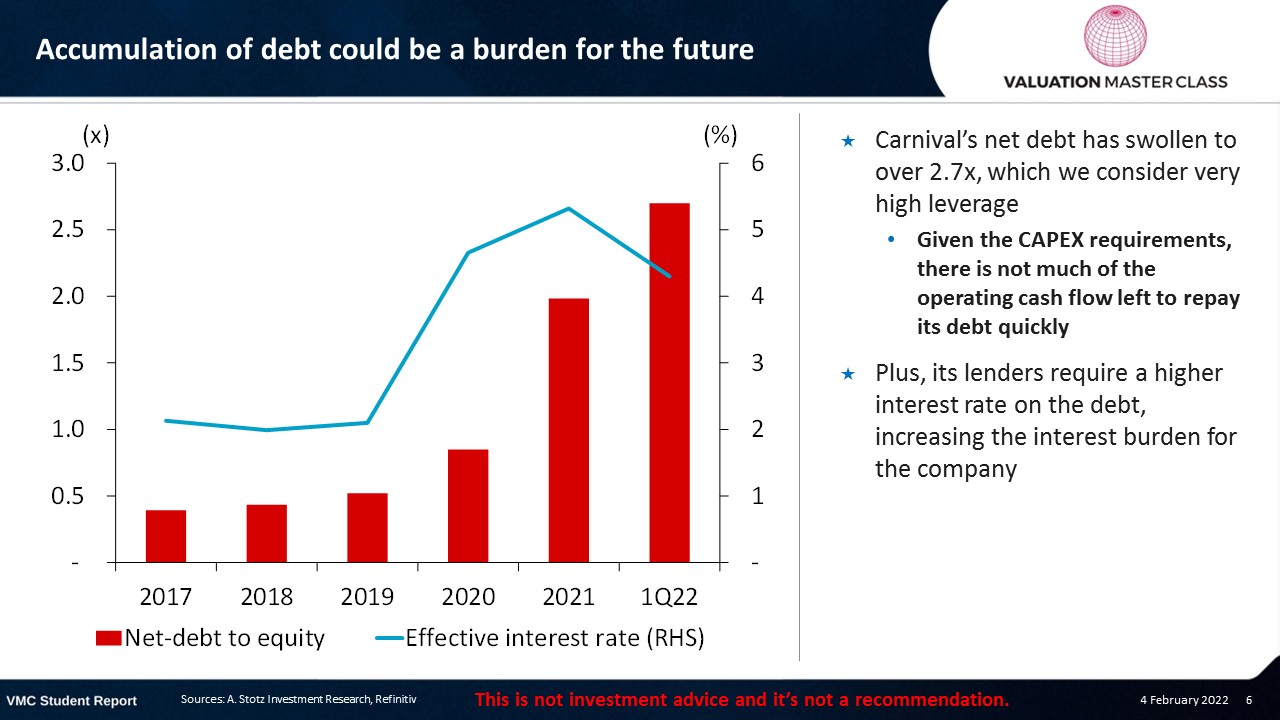

Accumulation of debt could be a burden for the future

- Carnival’s net debt has swollen to over 2.7x, which we consider very high leverage

- Given the CAPEX requirements, there is not much of the operating cash flow left to repay its debt quickly

- Plus, its lenders require a higher interest rate on the debt, increasing the interest burden for the company

Accumulation of debt could be a burden for the future

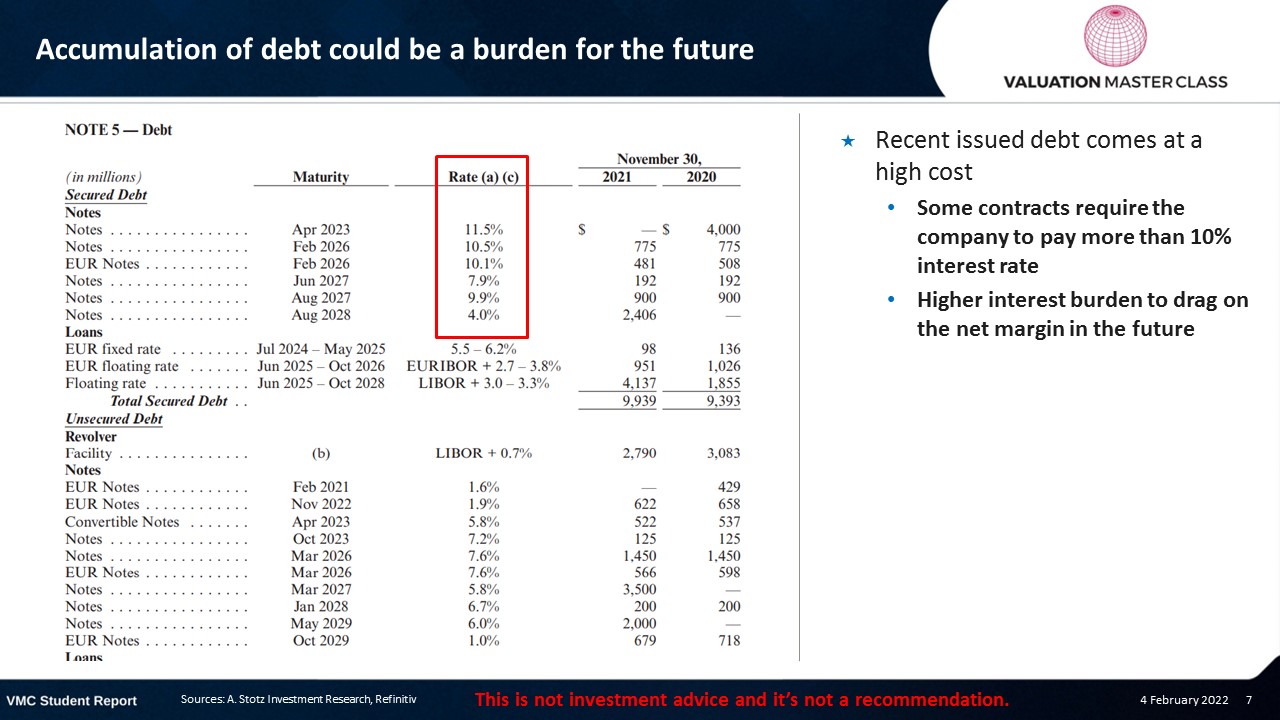

- Recent issued debt comes at a high cost

- Some contracts require the company to pay more than 10% interest rate

- Higher interest burden to drag on the net margin in the future

Accumulation of debt could be a burden for the future

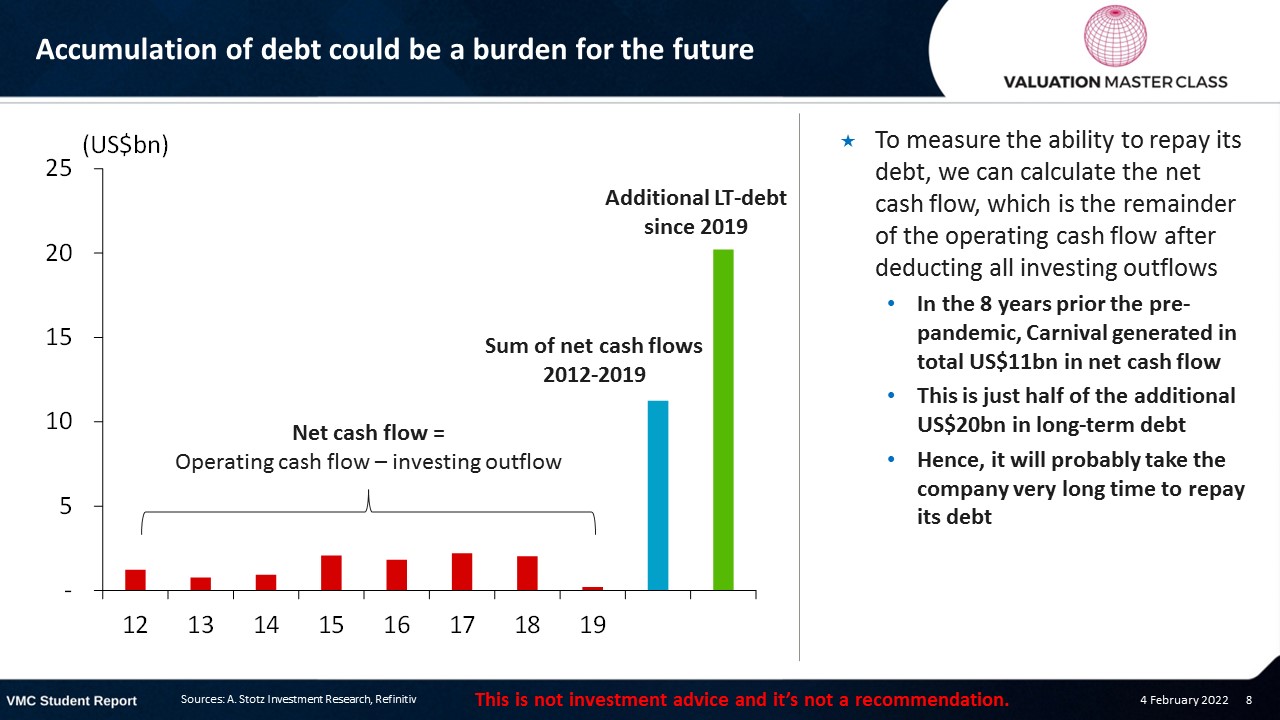

- To measure the ability to repay its debt, we can calculate the net cash flow, which is the remainder of the operating cash flow after deducting all investing outflows

- In the 8 years prior the pre-pandemic, Carnival generated in total US$11bn in net cash flow

- This is just half of the additional US$20bn in long-term debt

- Hence, it will probably take the company very long time to repay its debt

Cost pressures require restructuring of its fleet

- During the pandemic, Carnival has sold around 10% of its fleet size in its attempt to get rid off inefficient ships

- The future focus will be on the construction on larger and more efficient ships to keep costs low

Rumors to sell one of its brands showcases how much it struggles

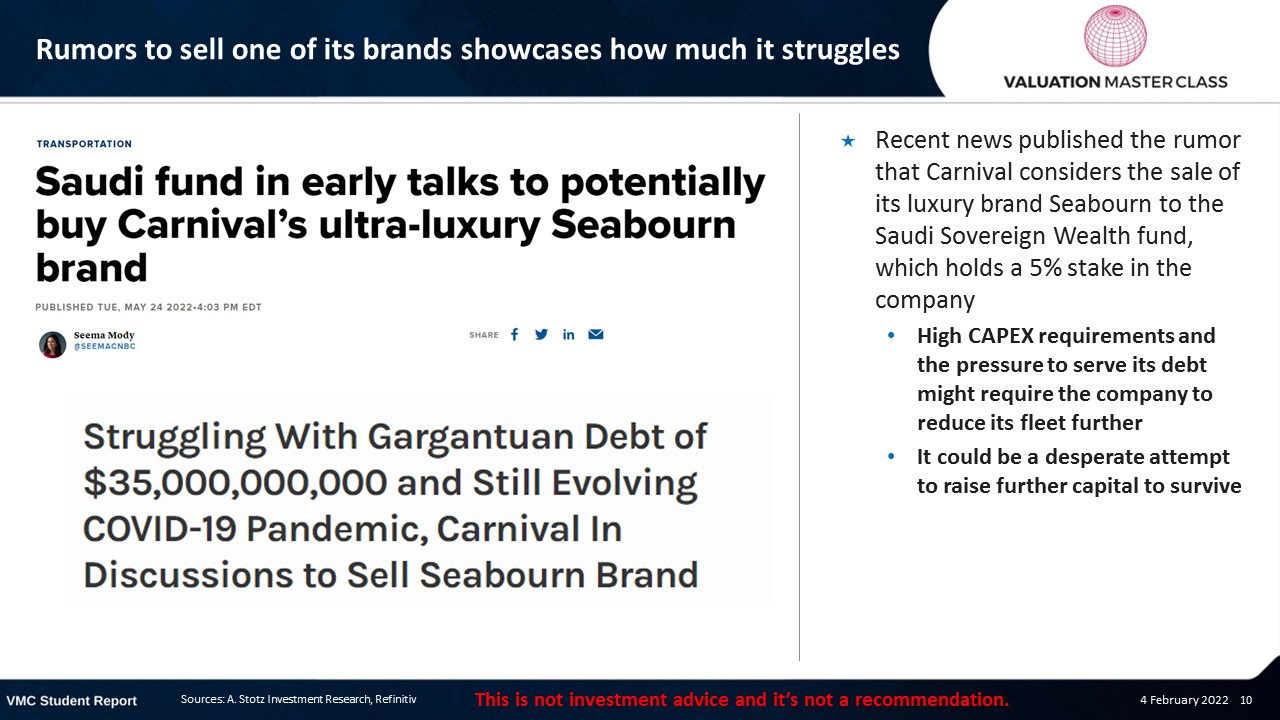

- Recent news published the rumor that Carnival considers the sale of its luxury brand Seabourn to the Saudi Sovereign Wealth fund, which holds a 5% stake in the company

- High CAPEX requirements and the pressure to serve its debt might require the company to reduce its fleet further

- It could be a desperate attempt to raise further capital to survive

Carnival needs its passengers to return urgently

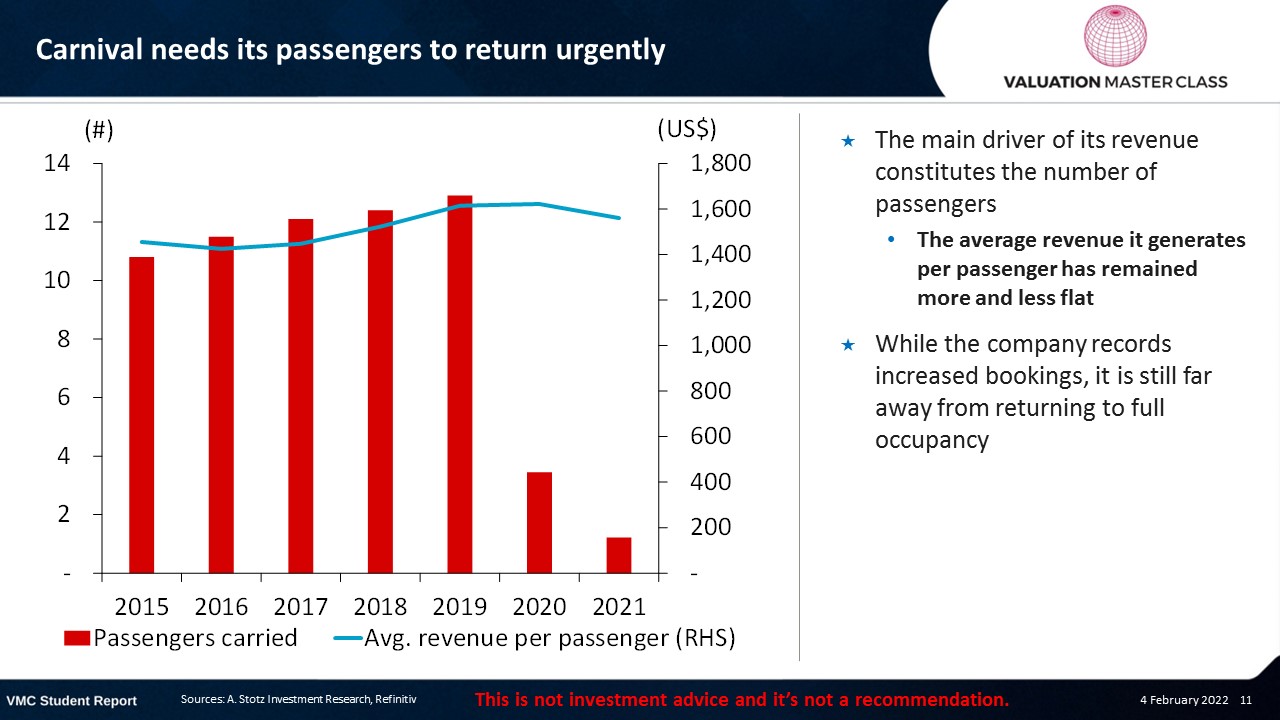

- The main driver of its revenue constitutes the number of passengers

- The average revenue it generates per passenger has remained more and less flat

- While the company records increased bookings, it is still far away from returning to full occupancy

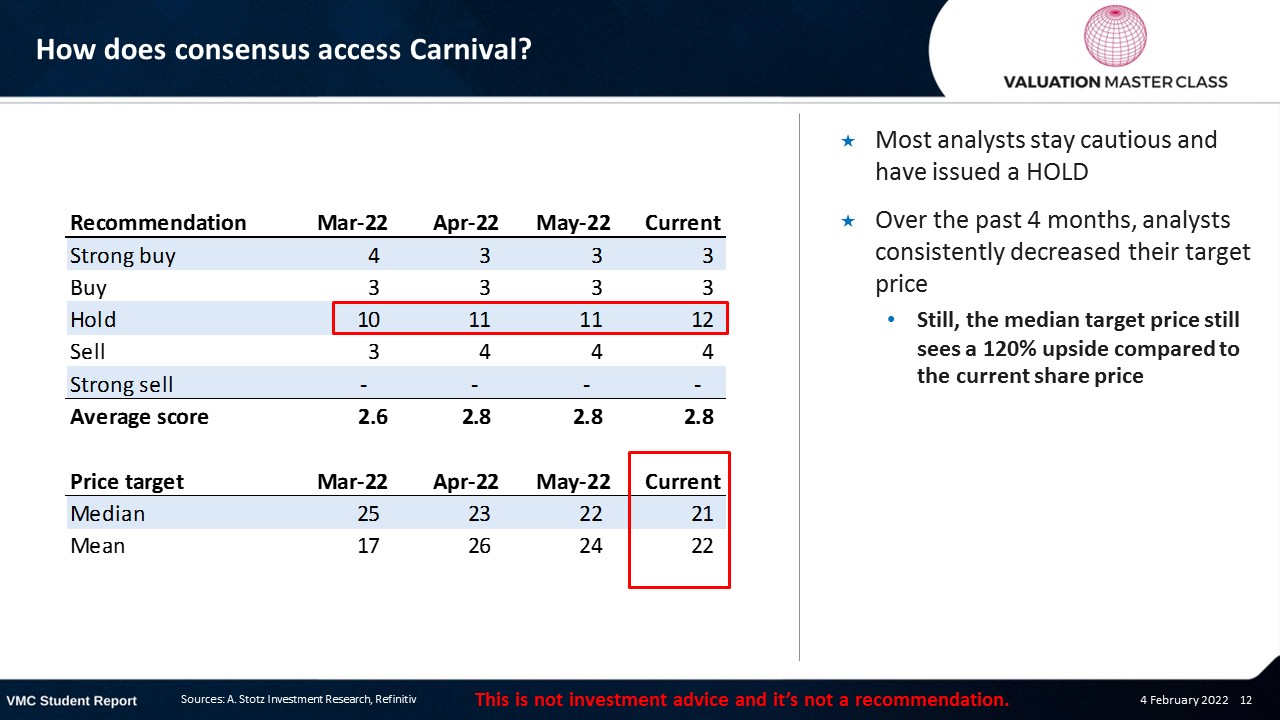

How does consensus access Carnival?

- Most analysts stay cautious and have issued a HOLD

- Over the past 4 months, analysts consistently decreased their target price

- Still, the median target price still sees a 120% upside compared to the current share price

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.