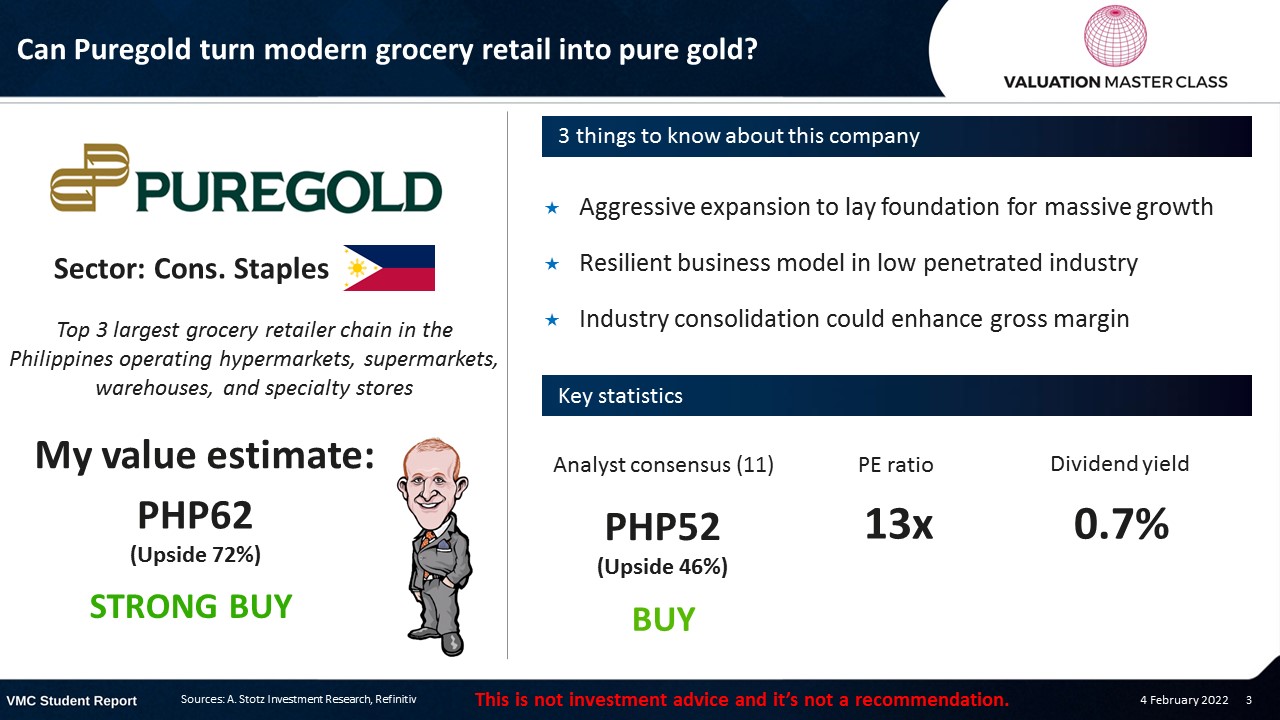

Can Puregold Turn Philippine Grocery Retail Into Pure Gold?

Highlights:

- Aggressive expansion to lay foundation for massive growth

- Resilient business model in low penetrated industry

- Industry consolidation could enhance gross margin

Download the full report as a PDF

Puregold Price Club’s revenue breakdown 2020

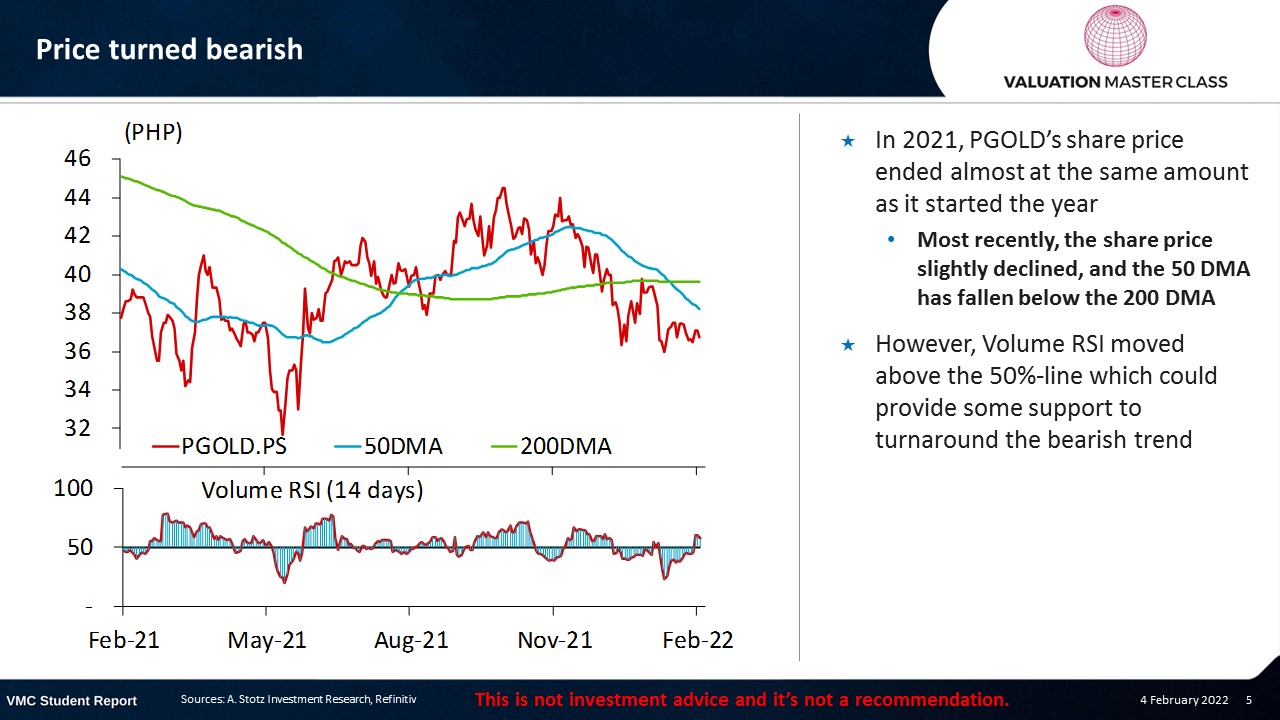

Price turned bearish

- In 2021, PGOLD’s share price ended almost at the same amount as it started the year

- Most recently, the share price slightly declined, and the 50 DMA has fallen below the 200 DMA

- However, Volume RSI moved above the 50%-line which could provide some support to turnaround the bearish trend

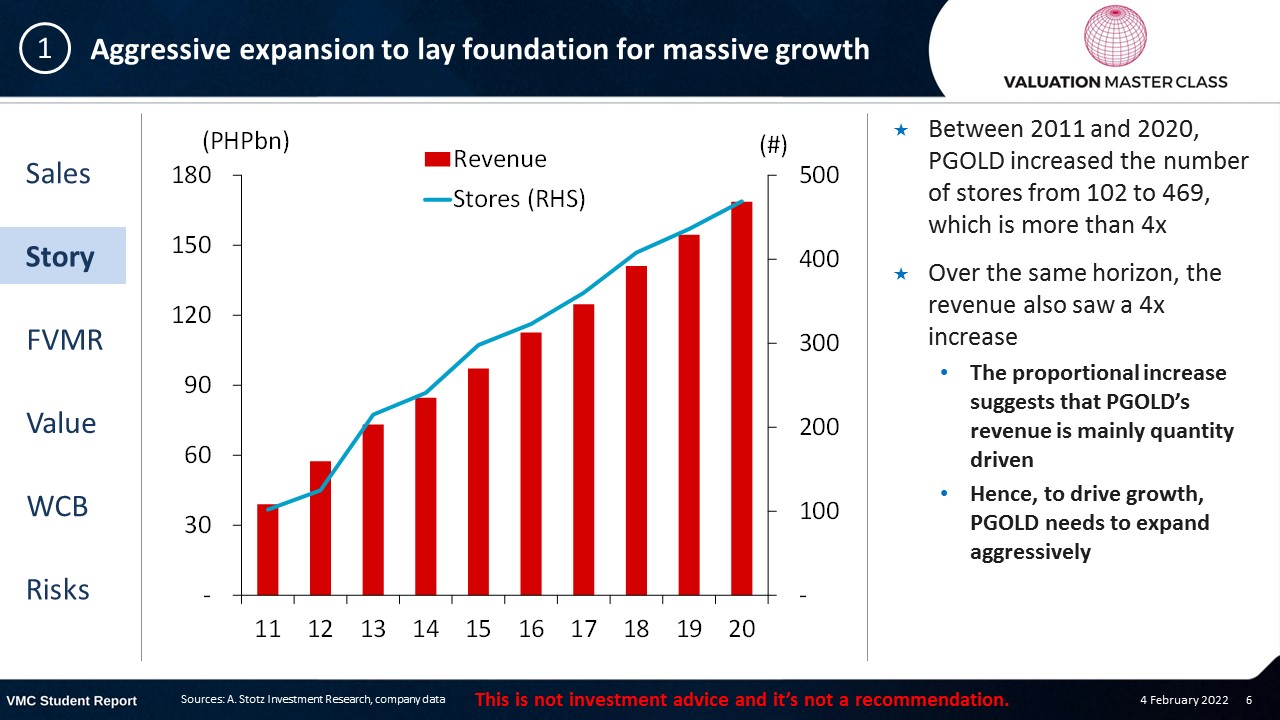

Aggressive expansion to lay foundation for massive growth

- Between 2011 and 2020, PGOLD increased the number of stores from 102 to 469, which is more than 4x

- Over the same horizon, the revenue also saw a 4x increase

- The proportional increase suggests that PGOLD’s revenue is mainly quantity driven

- Hence, to drive growth, PGOLD needs to expand aggressively

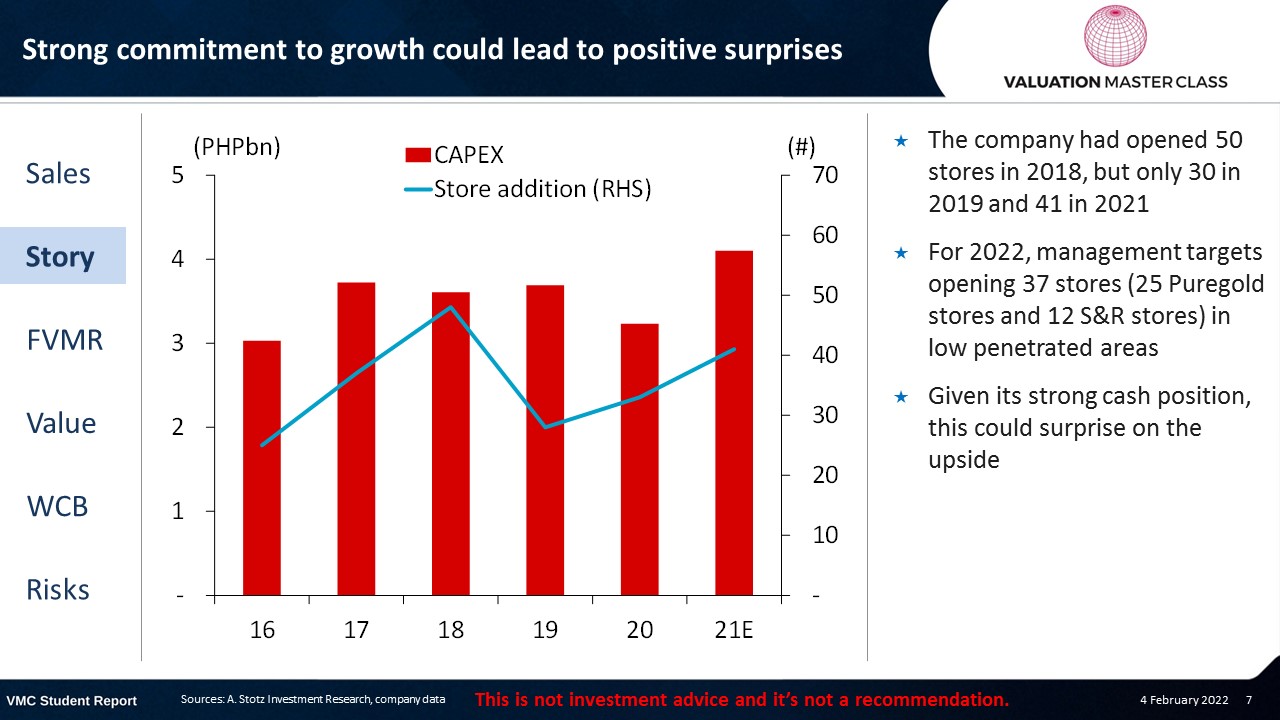

Strong commitment to growth could lead to positive surprises

- The company had opened 50 stores in 2018, but only 30 in 2019 and 41 in 2021

- For 2022, management targets opening 37 stores (25 Puregold stores and 12 S&R stores) in low penetrated areas

- Given its strong cash position, this could surprise on the upside

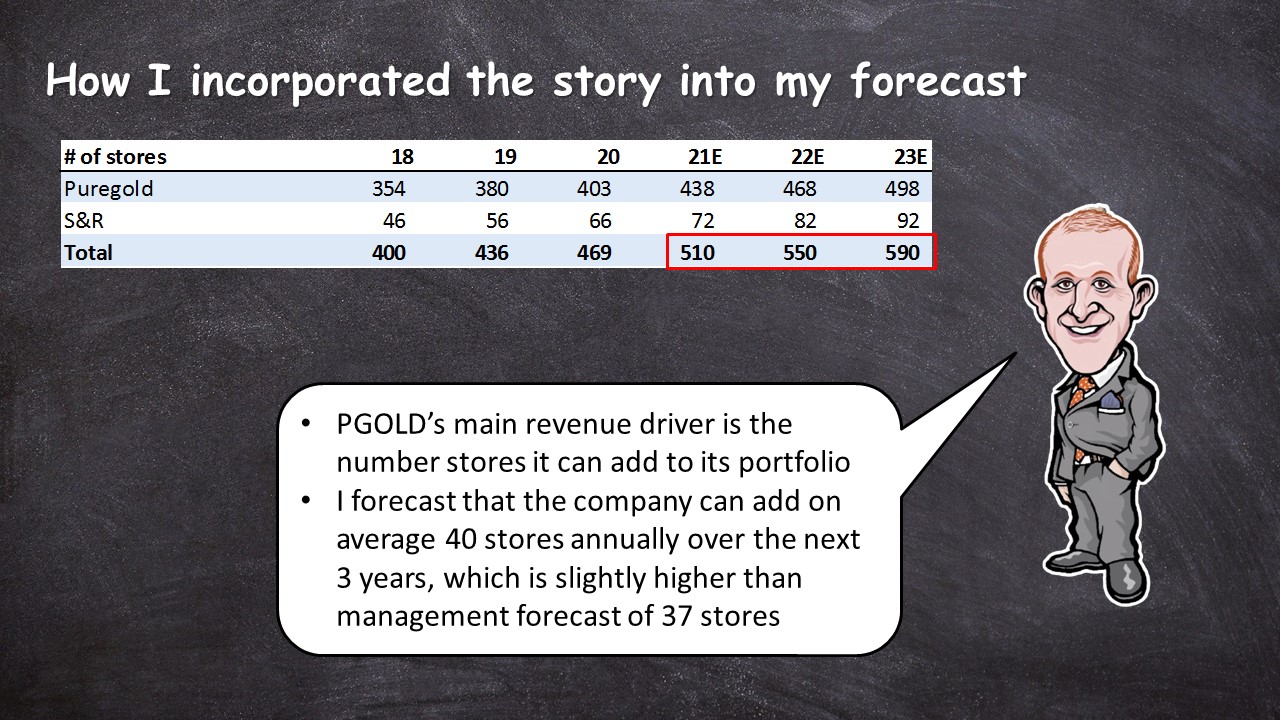

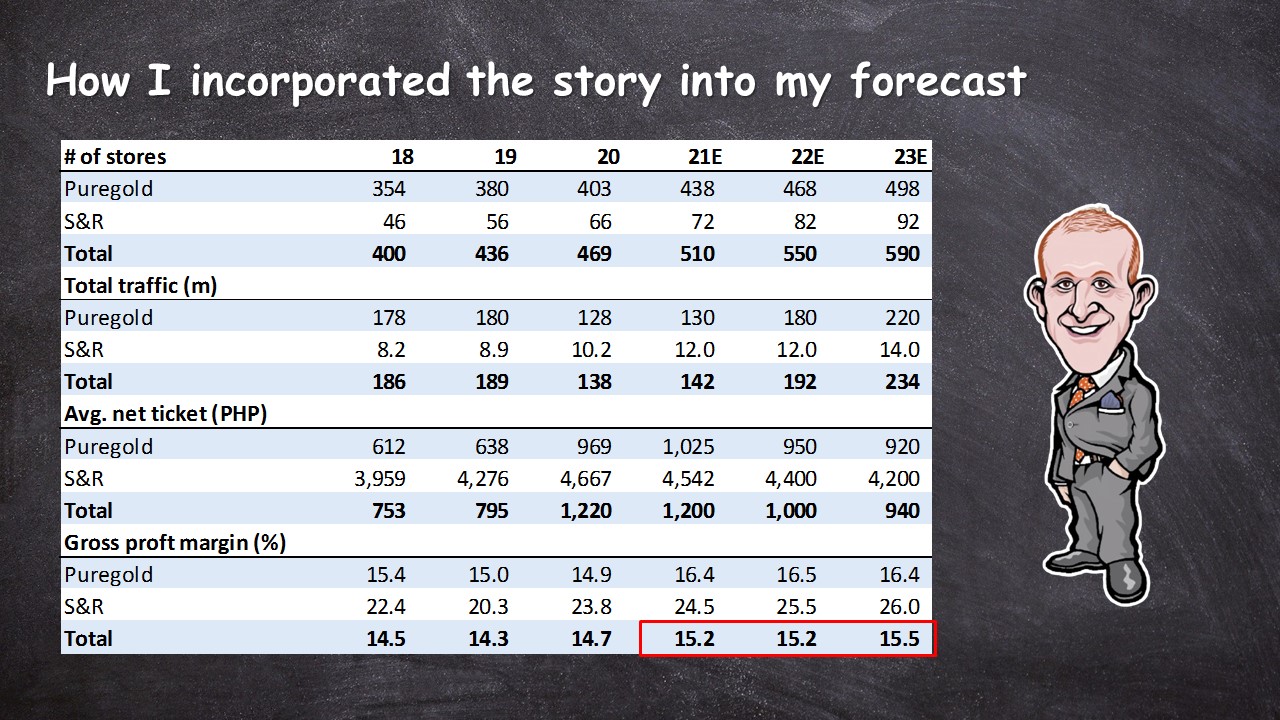

How I incorporated the story into my forecast

- PGOLD’s main revenue driver is the number stores it can add to its portfolio

- I forecast that the company can add on average 40 stores annually over the next 3 years, which is slightly higher than management forecast of 37 stores

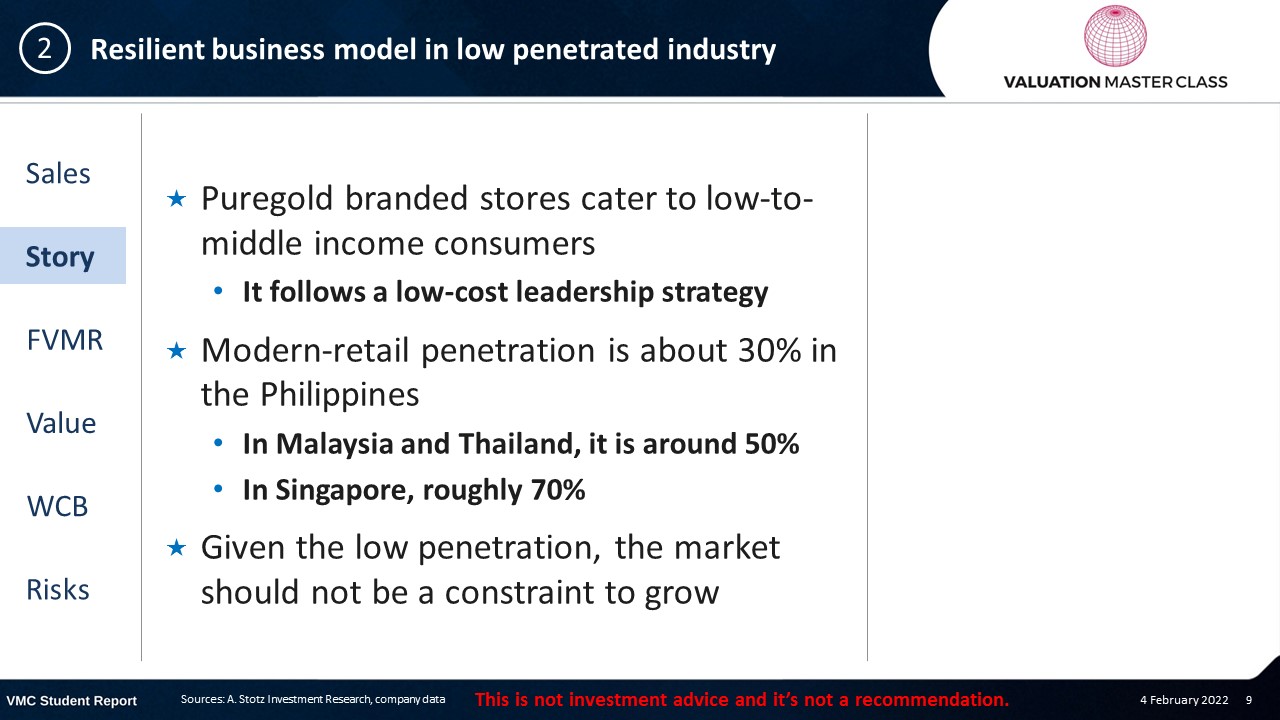

Resilient business model in low penetrated industry

- Puregold branded stores cater to low-to-middle income consumers

- It follows a low-cost leadership strategy

- Modern-retail penetration is about 30% in the Philippines

- In Malaysia and Thailand, it is around 50%

- In Singapore, roughly 70%

- Given the low penetration, the market should not be a constraint to grow

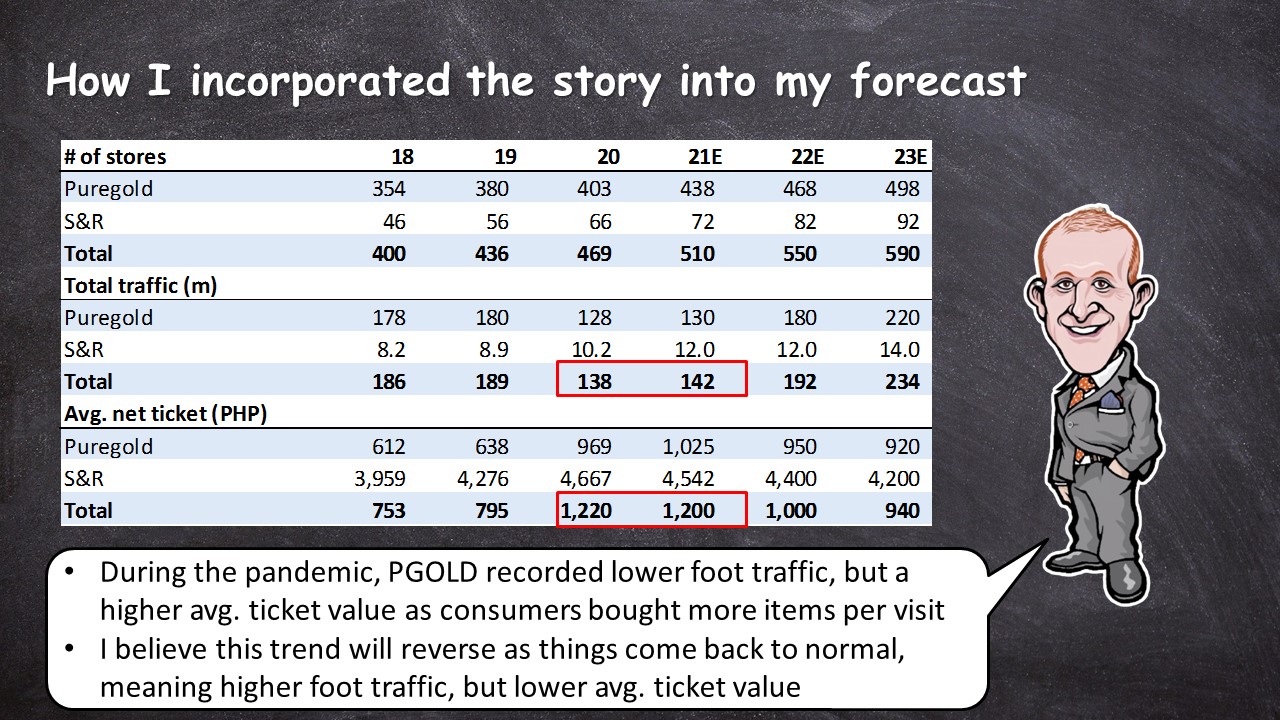

How I incorporated the story into my forecast

- During the pandemic, PGOLD recorded lower foot traffic, but a higher avg. ticket value as consumers bought more items per visit

- I believe this trend will reverse as things come back to normal, meaning higher foot traffic, but lower avg. ticket value

Industry consolidation could enhance gross margin

- The Philippine grocery retail market is still fragmented, but starting to consolidate

- The biggest competitors engage in material M&A activities to operate more stores under their own brand

- PGOLD responded with several acquisitions:

- 2012: S&R

- 2015: Budgetlane

- 2017: B&W stores

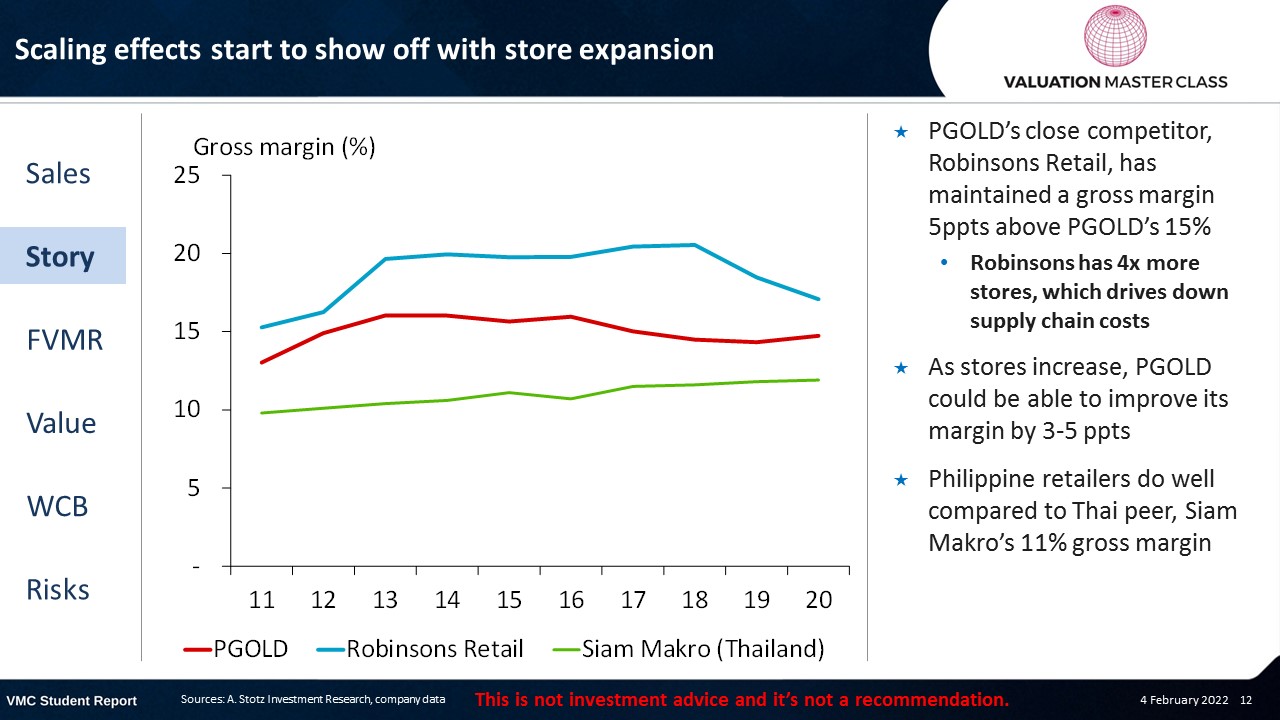

Scaling effects start to show off with store expansion

- PGOLD’s close competitor, Robinsons Retail, has maintained a gross margin 5ppts above PGOLD’s 15%

- Robinsons has 4x more stores, which drives down supply chain costs

- As stores increase, PGOLD could be able to improve its margin by 3-5 ppts

- Philippine retailers do well compared to Thai peer, Siam Makro’s 11% gross margin

How I incorporated the story into my forecast

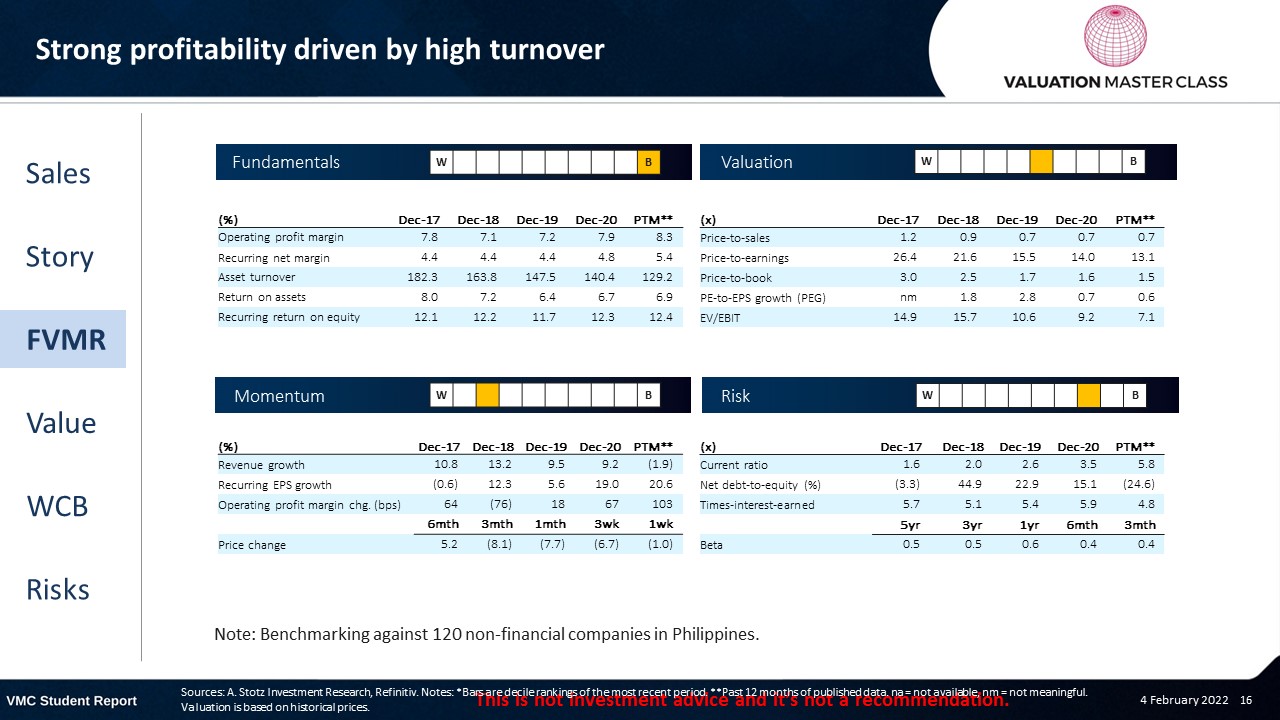

FVMR Scorecard – Puregold Price Club

- A stock’s attractiveness relative to stocks in that country or region

- Attractiveness is based on four elements

- Fundamentals, Valuation, Momentum, and Risk (FVMR)

- Scale from 1 (Best) to 10 (Worst)

Consensus is strongly bullish

- Most analysts have a BUY recommendation, as the company continues to deliver on its expansion plans

- Consensus is rewarding management’s efforts by forecasting high growth from 22E onward

- Also, analysts assume a slightly higher margin compared to the past

Get financial statements and assumptions in the full report

P&L – Puregold Price Club

- While revenue stayed flat in 21E, it should continue to see high growth from 22E onward

- New stores open and foot traffic should normalize

Balance sheet – Puregold Price Club

- Defensive balance sheet with ¼ of its assets in cash helps when it’s time to play offense

- Net fixed assets grow in line with its annual target for store openings

- I don’t expect the company to accumulate more debt over time as it has a high cash generation ability to fund growth internally

Ratios – Pureclub Price Club

- Like most retailers PGOLD has strong asset turnover of 130-150, which means sales grow faster than assets

- This measure should start to recover as revenue recovers

- Scale effects should show up in the gross margin over time

- I expect PGOLD to raise its margin to the same levels as its competitor Robinsons Retail (17-20%)

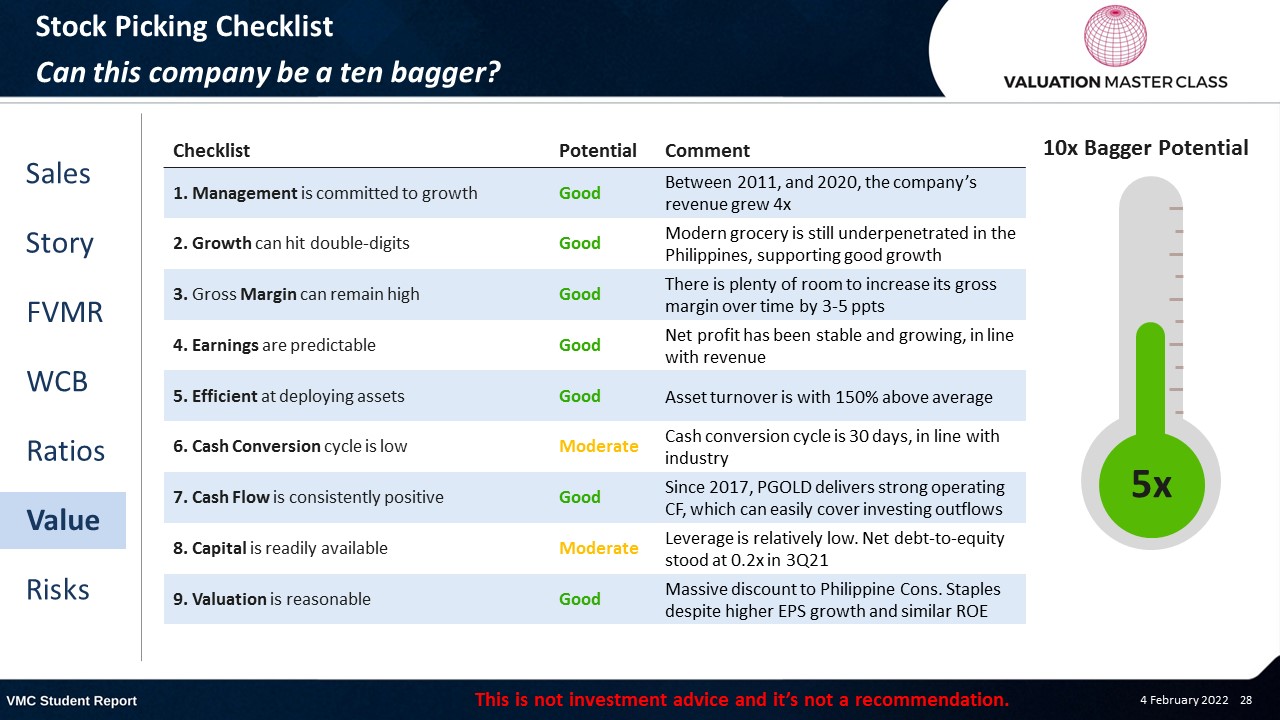

Stock Picking Checklist: Can this company be a ten bagger?

Free cash flow – Puregold Price Club

- Since 2017, PGOLD delivers consistent positive FCFF and should continue to do so over the next few years

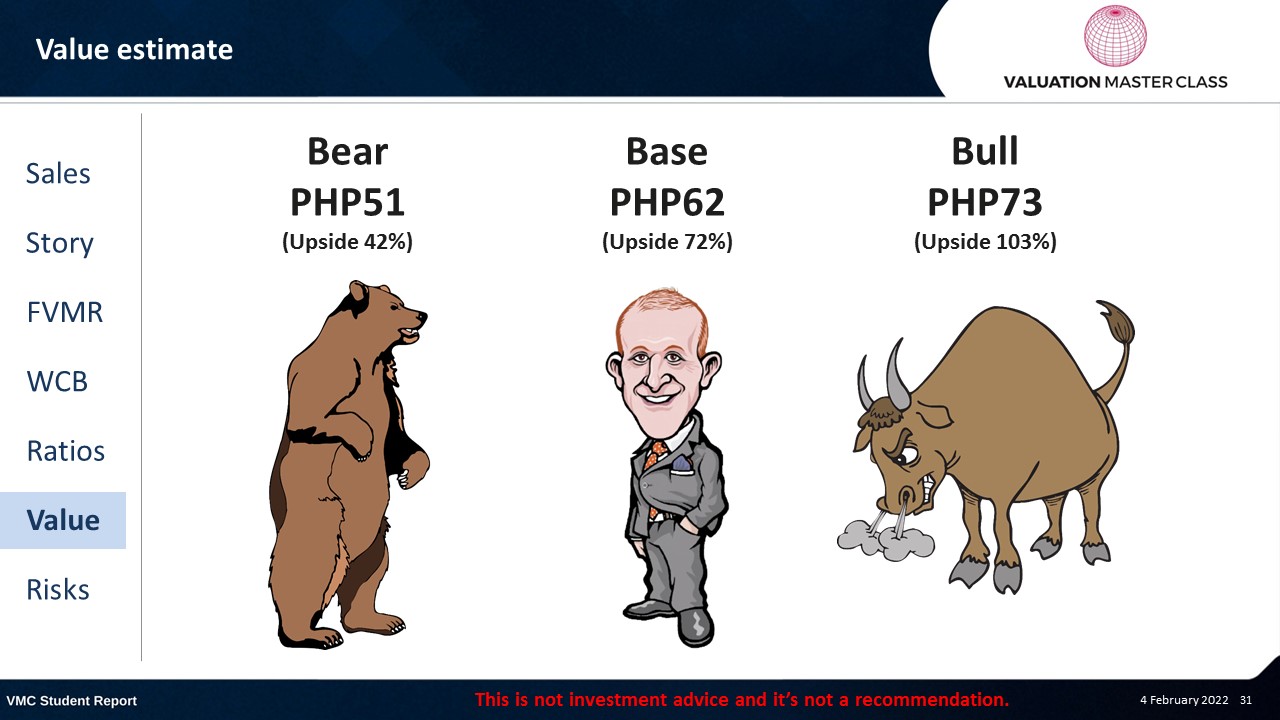

Value estimate – Puregold Price Club

- I expect faster revenue growth than consensus as PGOLD’s balance sheet allows for fast-than-expected store expansion

- Also, I am more optimistic with regards to the margin

- I don’t see any constraint why PGOLD could not close the margin gap to its competitor over time

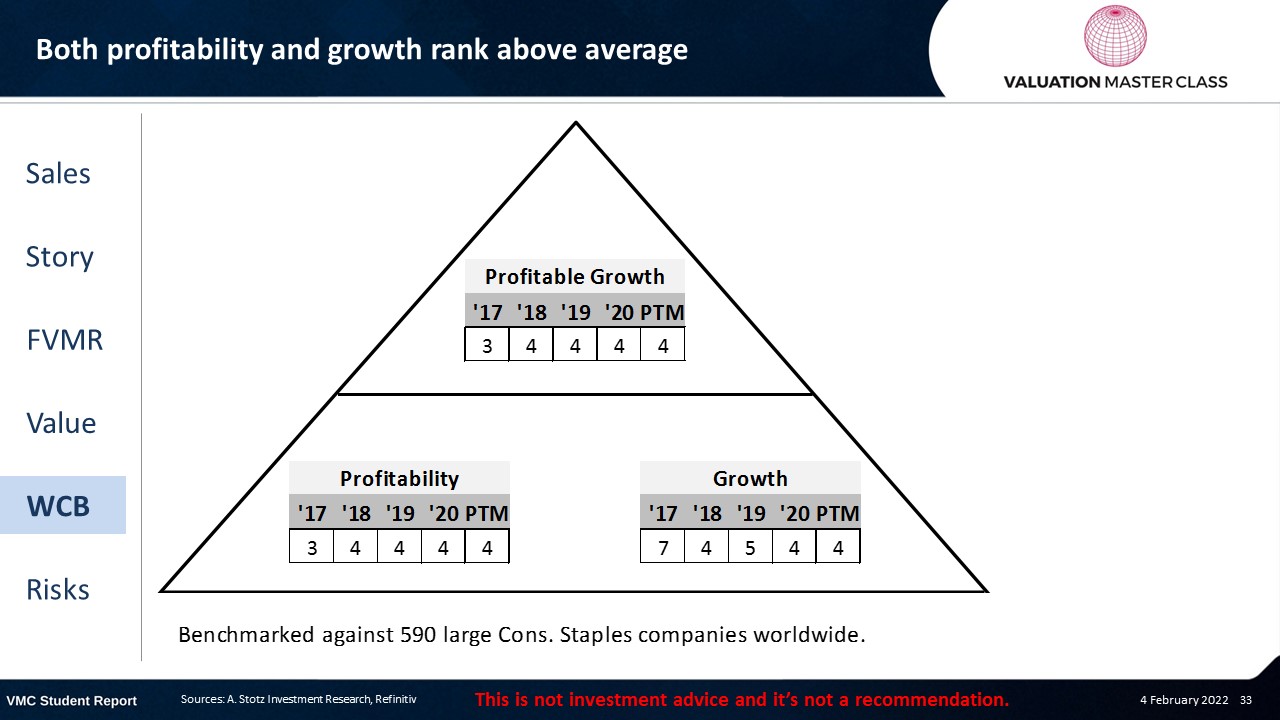

World Class Benchmarking Scorecard – Puregold Price Club

- Identifies a company’s competitive position relative to global peers

- Combined, composite rank of profitability and growth, called “Profitable Growth”

- Scale from 1 (Best) to 10 (Worst)

Key risk is lower-than-expected growth

- Failure to execute its growth strategy

- Industry consolidation could intensify competition

- Limited ability to pass on higher costs as PGOLD targets low-income segment

Conclusions

- Expansion could progress faster than the market expects

- If PGOLD can increase its gross margin to its competitor’s level, it would provide a solid upside

- Valuation is surprisingly cheap as it trades at a 55% discount on PE

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.