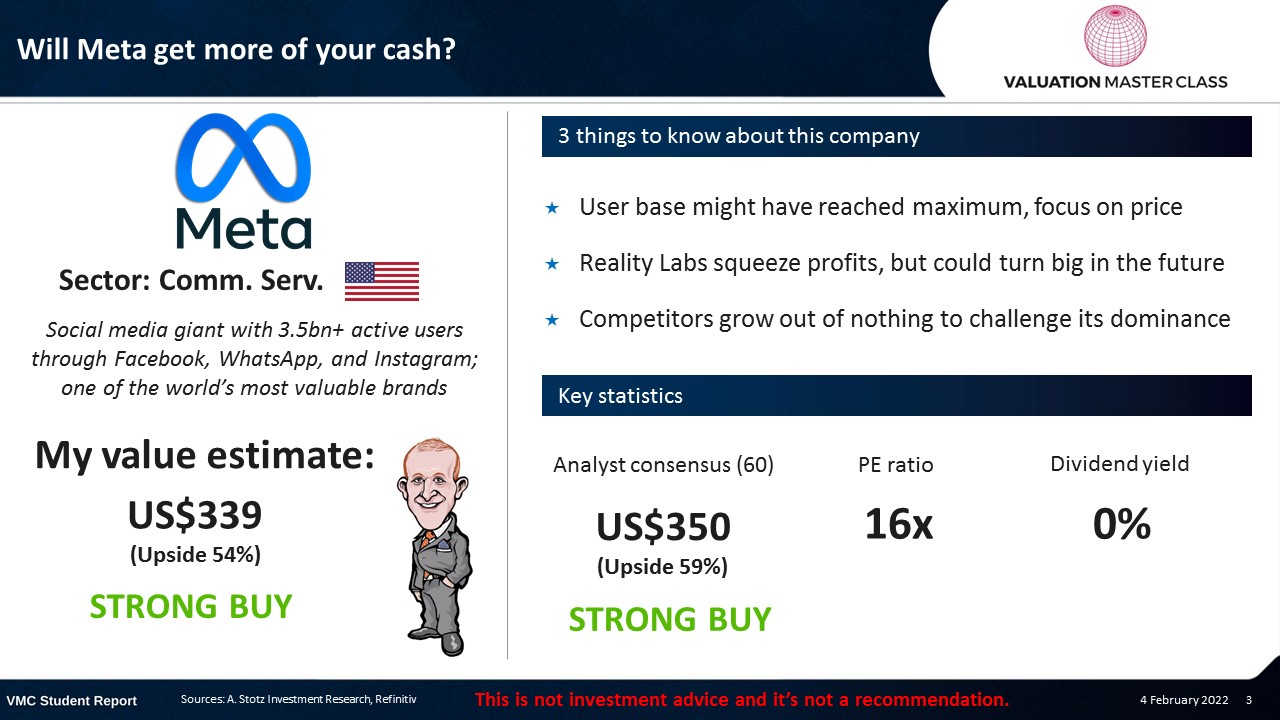

Will Meta get more of your cash?

Highlights:

- User base might have reached maximum, focus on price

- Reality Labs squeeze profits, but could turn big in the future

- Competitors grow out of nothing to challenge its dominance

Download the full report as a PDF

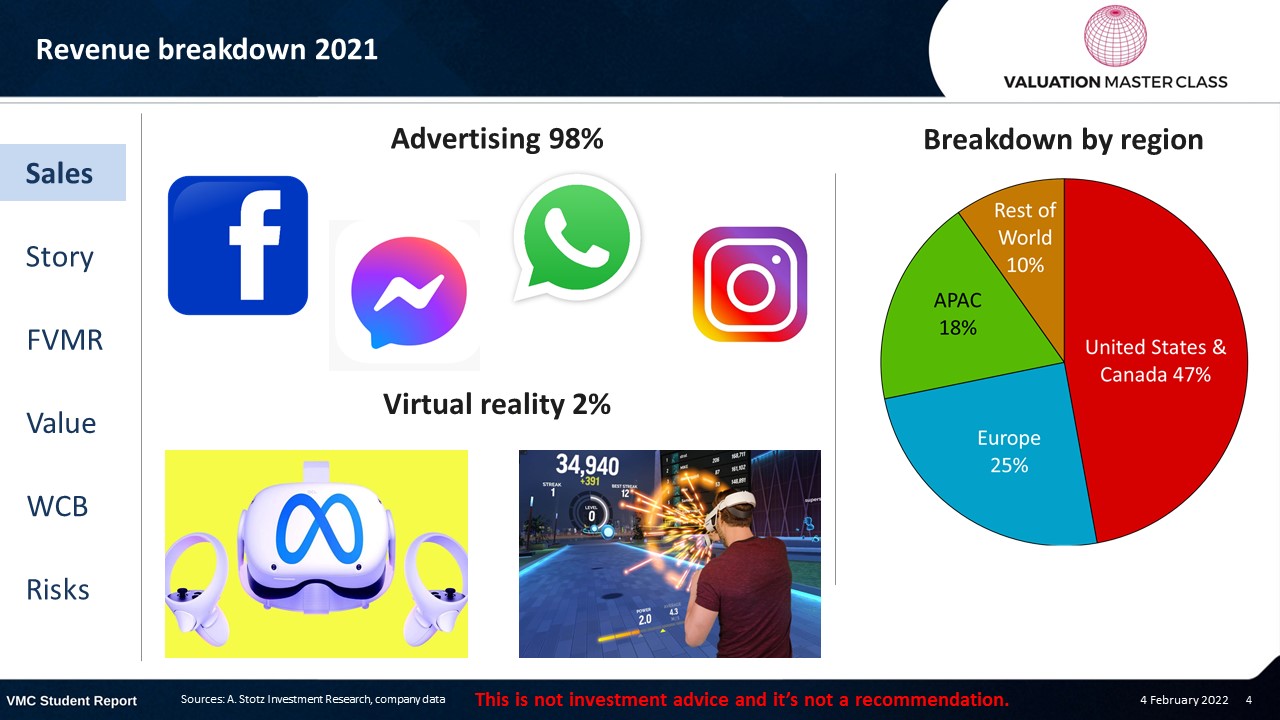

Meta Platforms’ revenue breakdown 2021

Price turned bearish but could turnaround soon

- In the first three quarters of 2021, Meta saw a strong bullish rally before its price has been corrected downward by the end of past year

- In January 2022, Meta saw its largest intra-day drop in its history with the share price down by 25%

- However, recently, the share price started to rebound and could do so further

- Volume RSI has been neutral recently, providing no clear signal yet

What did actually happen to Meta’s share price?

- On 3rd of January, Meta’s share price dropped by 25%, equaling around US$230bn in market cap

- Here is what happened:

- Meta reported a decline in daily active users for the first time

- Apple update on iOS devices makes it more difficult to track consumers, dragging Meta’s advertising revenue

- US$10bn loss from its new Reality Labs business unit

- Lower management profit forecast for 2022E

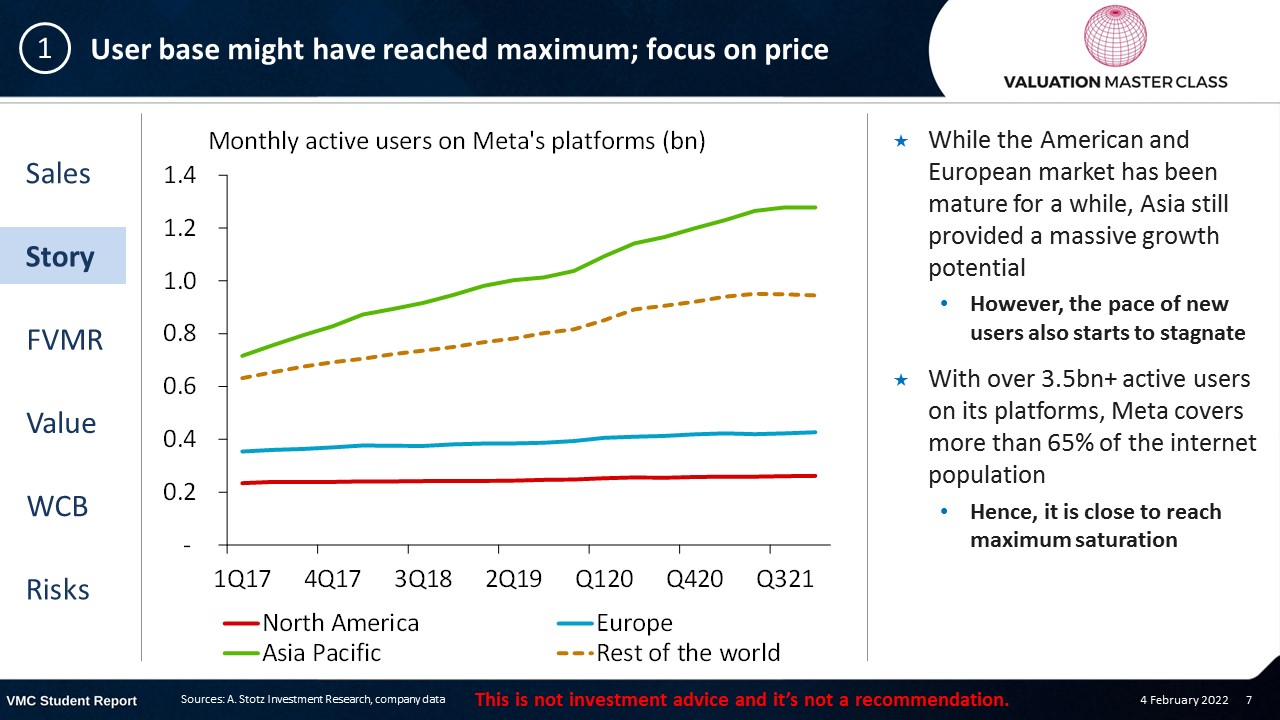

User base might have reached maximum; focus on price

- While the American and European market has been mature for a while, Asia still provided a massive growth potential

- However, the pace of new users also starts to stagnate

- With over 3.5bn+ active users on its platforms, Meta covers more than 65% of the internet population

- Hence, it is close to reach maximum saturation

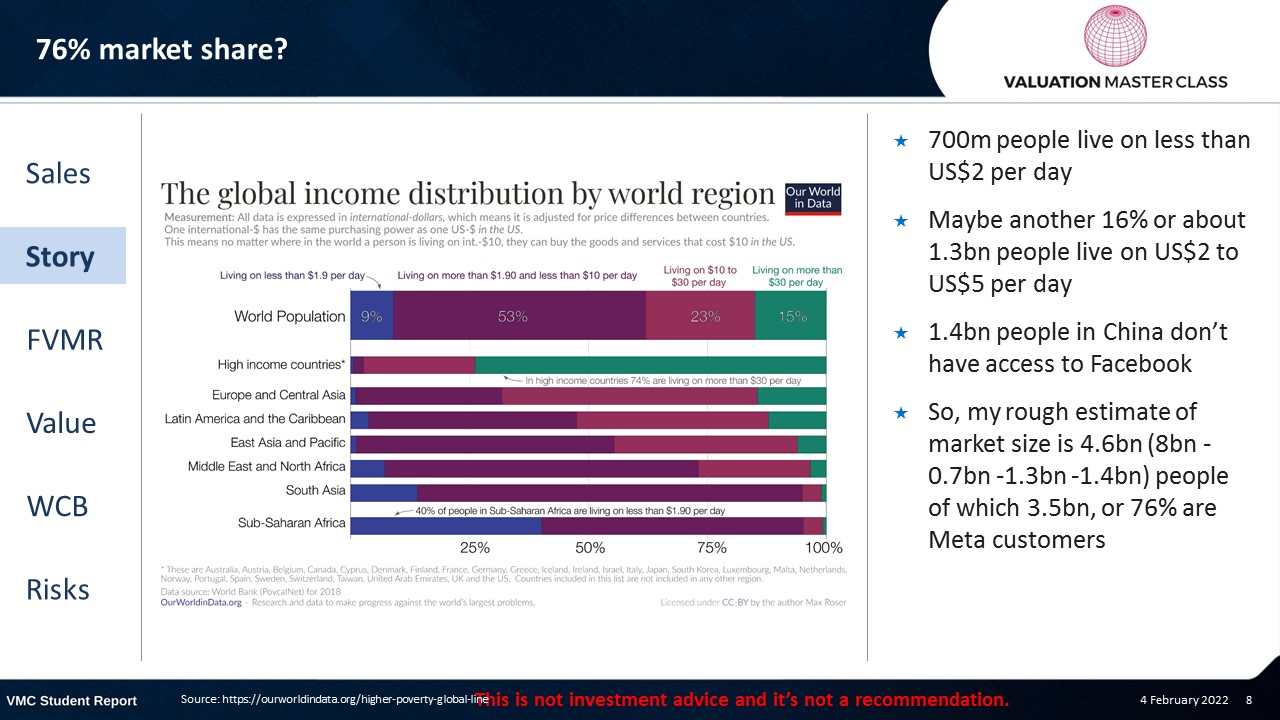

76% market share?

- 700m people live on less than US$2 per day

- Maybe another 16% or about 1.3bn people live on US$2 to US$5 per day

- 1.4bn people in China don’t have access to Facebook

- So, my rough estimate of market size is 4.6bn (8bn – 0.7bn -1.3bn -1.4bn) people of which 3.5bn, or 76% are Meta customers

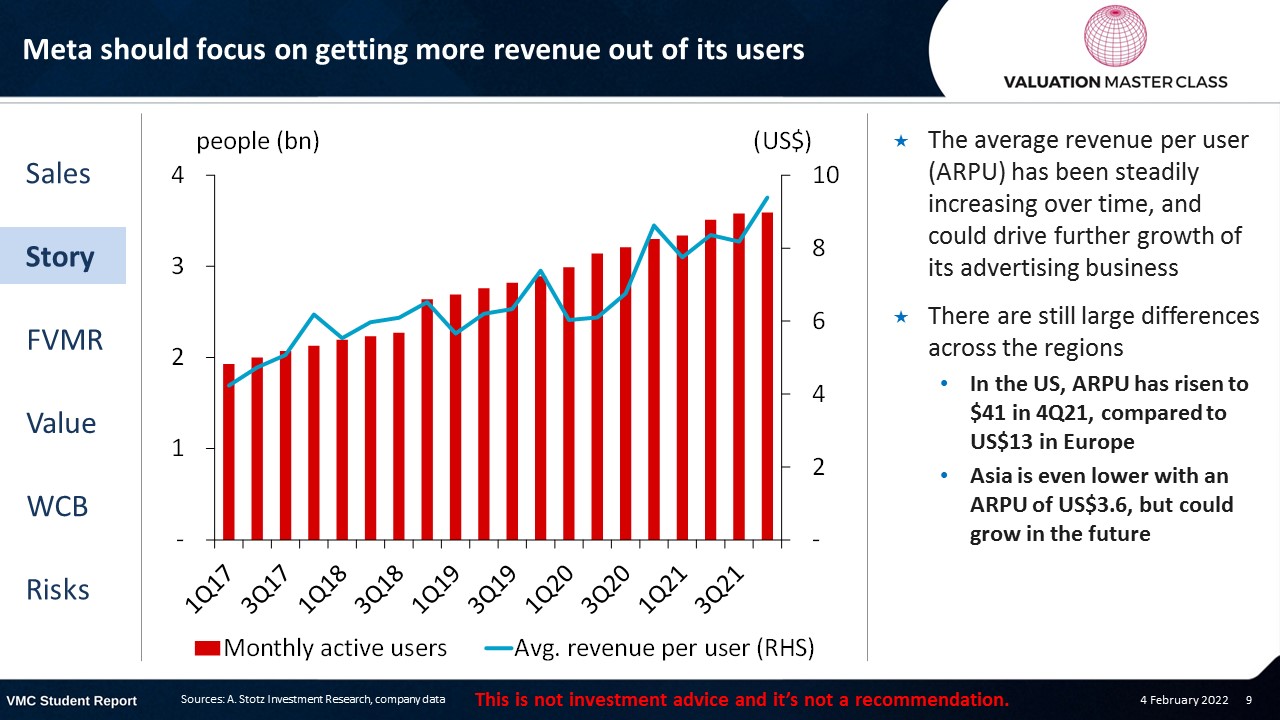

Meta should focus on getting more revenue out of its users

- The average revenue per user (ARPU) has been steadily increasing over time, and could drive further growth of its advertising business

- There are still large differences across the regions

- In the US, ARPU has risen to $41 in 4Q21, compared to US$13 in Europe

- Asia is even lower with an ARPU of US$3.6, but could grow in the future

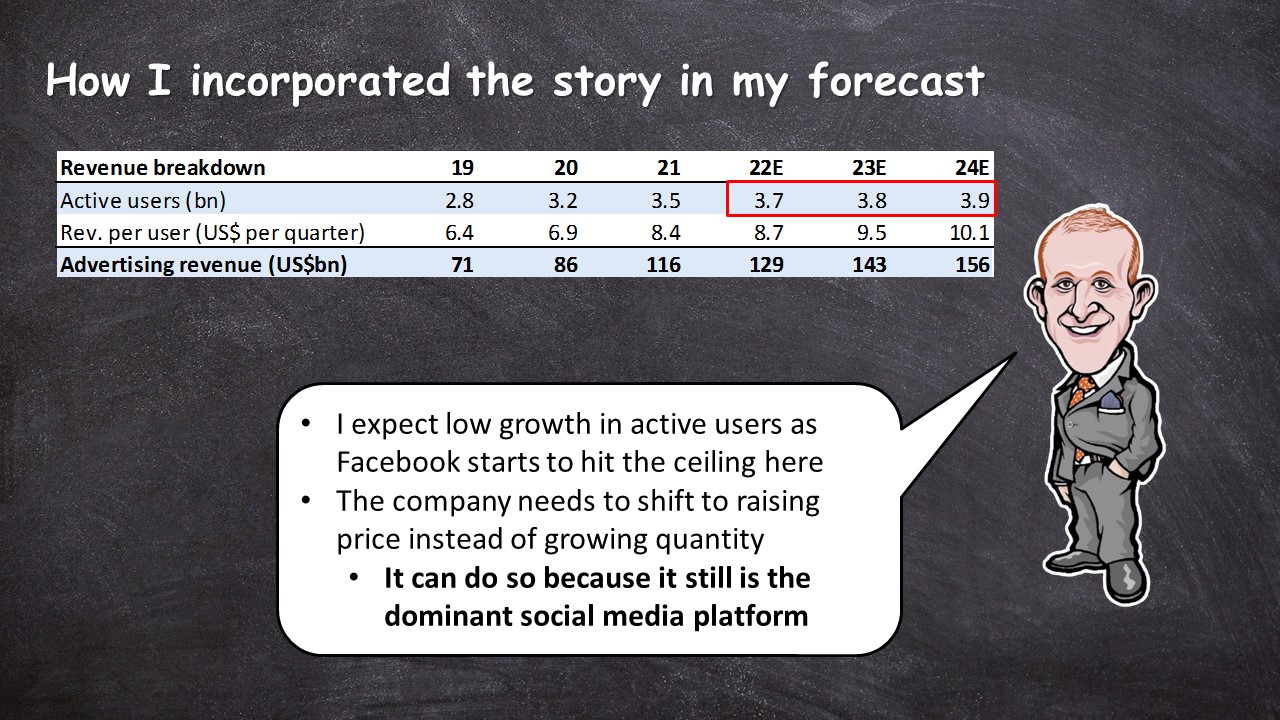

How I incorporated the story in my forecast

- I expect low growth in active users as Facebook starts to hit the ceiling here

- The company needs to shift to raising price instead of growing quantity

- It can do so because it still is the dominant social media platform

Reality Labs squeeze profits, but could turn big in the future

- The company’s strategy is to transition from a social platform into an entire virtual world called metaverse

- The main concept is to take the digital experience to a new level

- Therefore, Meta has created its new reporting unit “Reality Labs”

- Its product range covers virtual reality headsets and development of games, smart glasses, presence platforms, and work-related applications

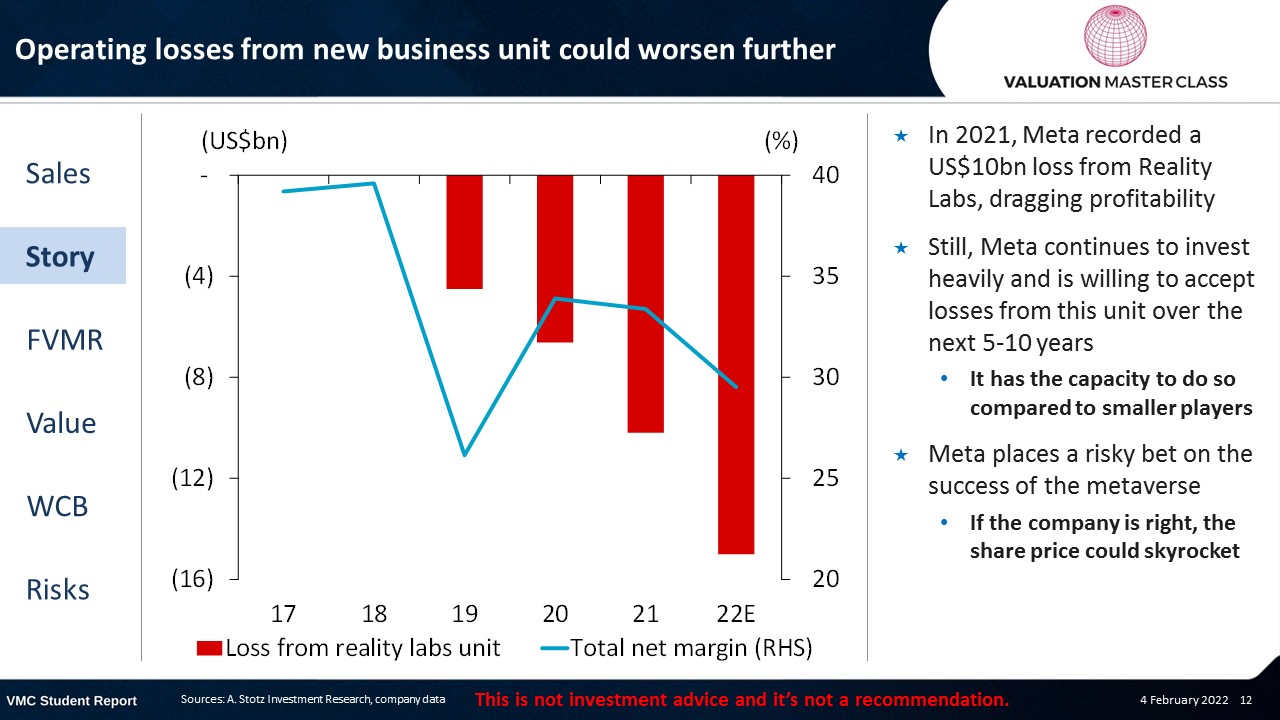

Operating losses from new business unit could worsen further

- In 2021, Meta recorded a US$10bn loss from Reality Labs, dragging profitability

- Still, Meta continues to invest heavily and is willing to accept losses from this unit over the next 5-10 years

- It has the capacity to do so compared to smaller players

- Meta places a risky bet on the success of the metaverse

- If the company is right, the share price could skyrocket

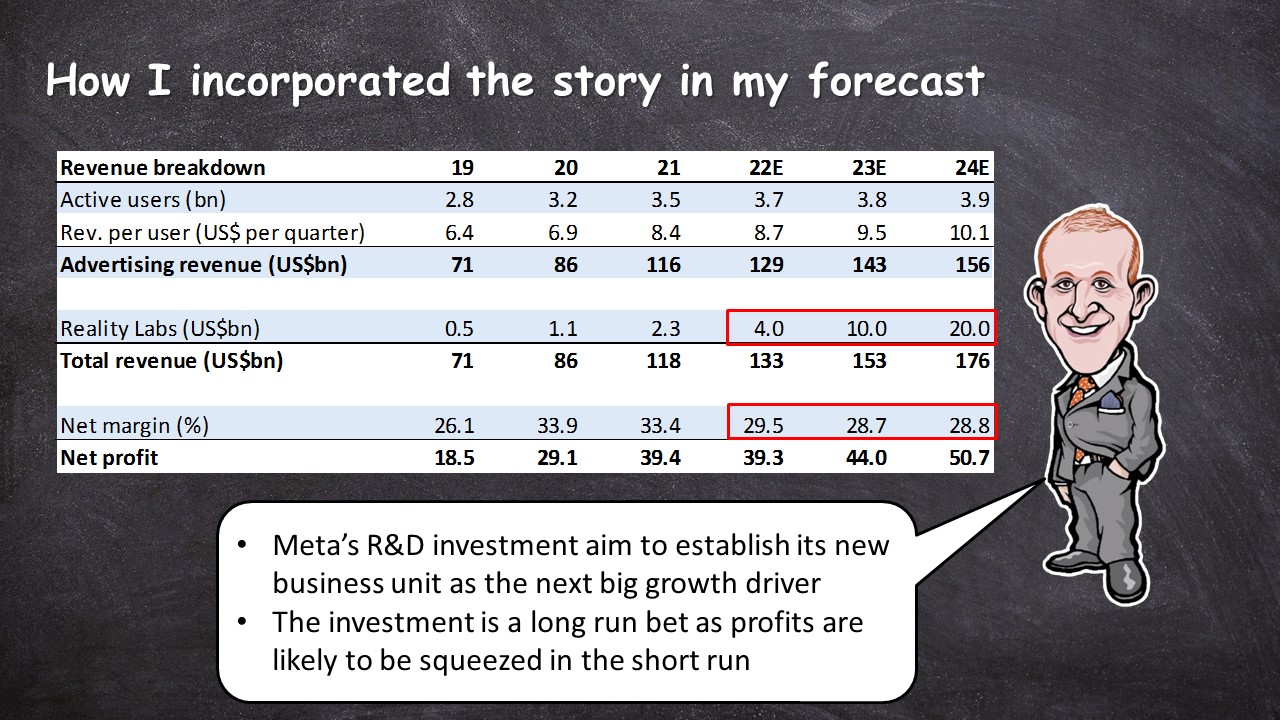

How I incorporated the story in my forecast

- Meta’s R&D investment aim to establish its new business unit as the next big growth driver

- The investment is a long run bet as profits are likely to be squeezed in the short run

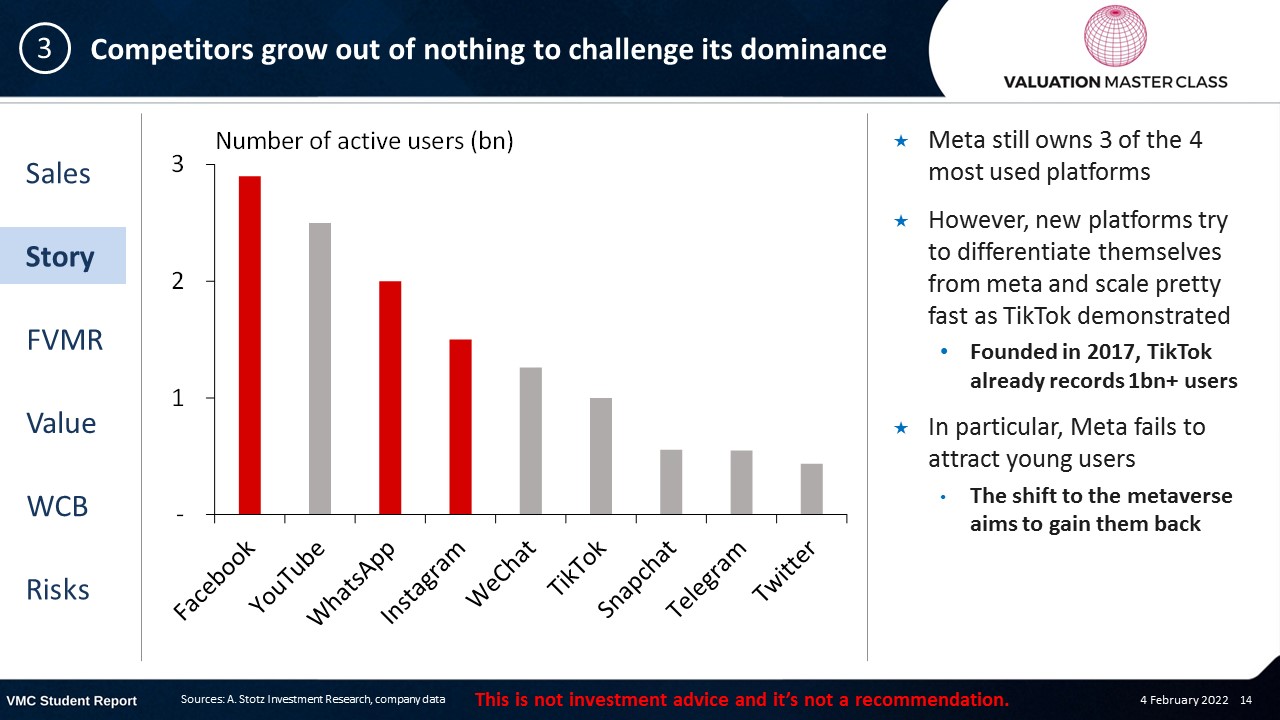

Competitors grow out of nothing to challenge its dominance

- Meta still owns 3 of the 4 most used platforms

- However, new platforms try to differentiate themselves from meta and scale pretty fast as TikTok demonstrated

- Founded in 2017, TikTok already records 1bn+ users

- In particular, Meta fails to attract young users

- The shift to the metaverse aims to gain them back

Copycats are nipping at their heels

- Even I got put in Facebook jail!

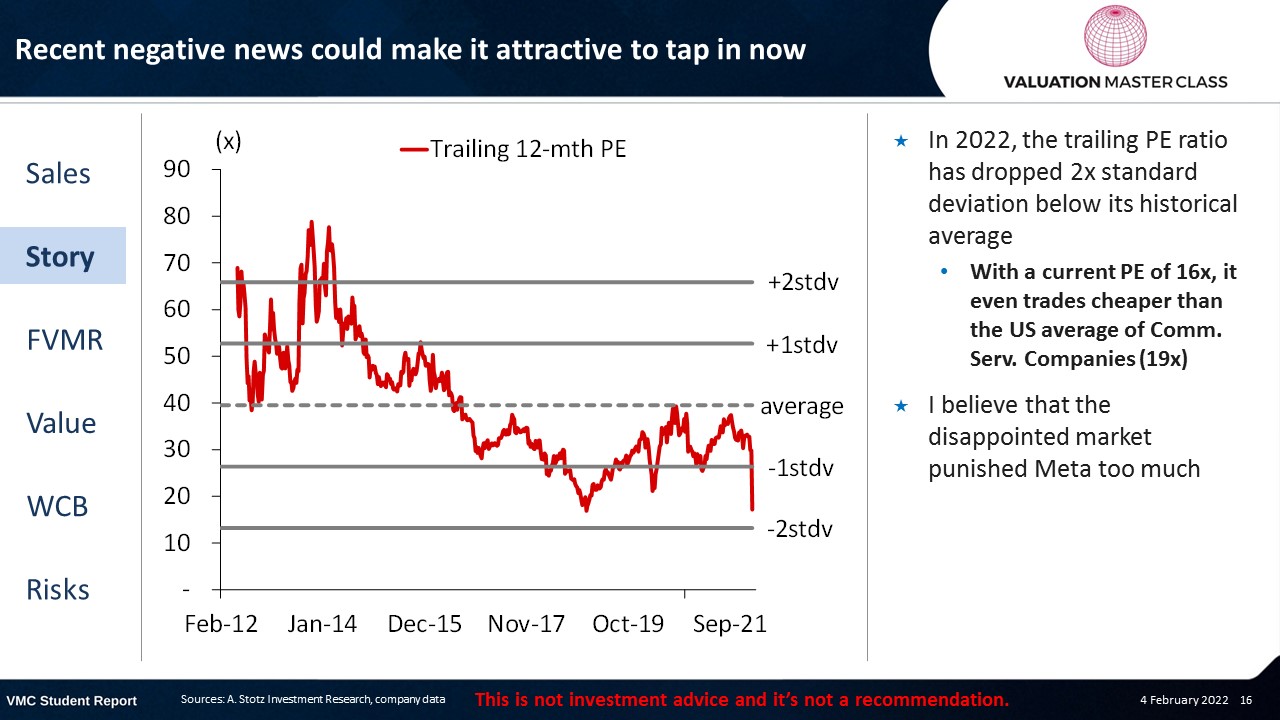

Recent negative news could make it attractive to tap in now

- In 2022, the trailing PE ratio has dropped 2x standard deviation below its historical average

- With a current PE of 16x, it even trades cheaper than the US average of Comm. Serv. Companies (19x)

- I believe that the disappointed market punished Meta too much

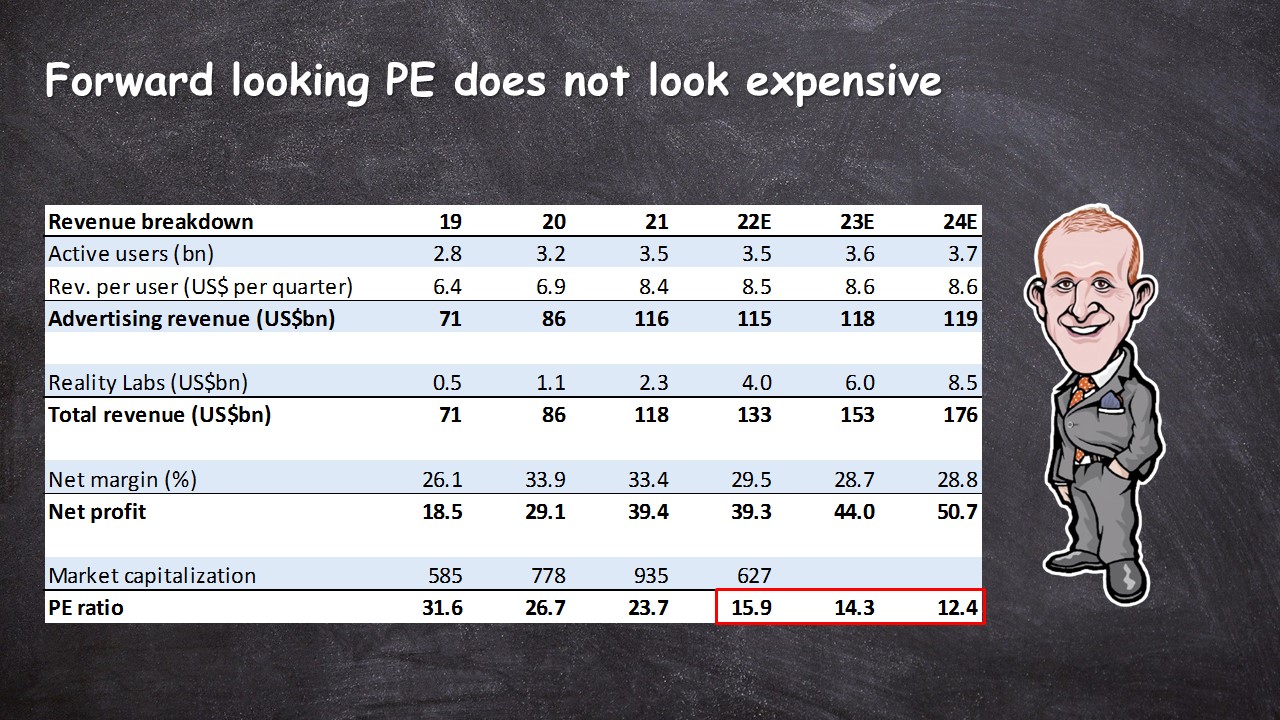

Forward looking PE does not look expensive

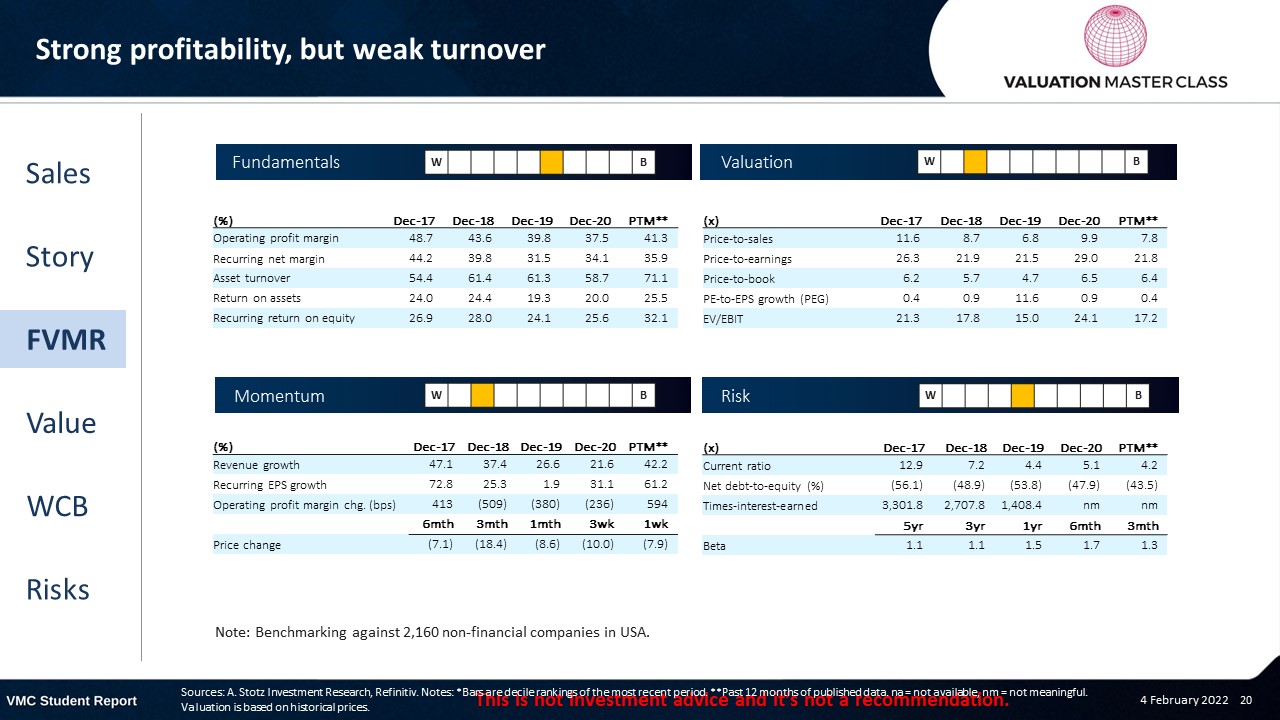

FVMR Scorecard – Meta Platforms

- A stock’s attractiveness relative to stocks in that country or region

- Attractiveness is based on four elements

- Fundamentals, Valuation, Momentum, and Risk (FVMR)

- Scale from 1 (Best) to 10 (Worst)

Consensus is bullish

- Most analysts has a BUY recommendation, as it sees a massive potential after the share price has been beaten down

- Consensus has already incorporated a significant drop in margin due to the loss-making Reality Lab business unit

Get financial statements and assumptions in the full report

P&L – Meta Platforms

- In line with management forecast, I don’t expect a profit growth in 22E as the Reality Labs unit could make growing losses

Balance sheet – Meta Platforms

- Meta announced to continue investing heavily in data infrastructure and development of new virtual reality products

- Also, it has a large, US$50bn amount of cash, equaling 1/3 of its total assets

- Meta is net cash and has very low debt, which is quite typical for fast-growing companies

Ratios – Meta Platforms

- Meta has a remarkable consistent profitability, which is far above the sector average ROE of 18%

- Profitability is dragged in the short run

- However, in the long run, the contribution of the metaverse business could bring profitability back to its previous heights

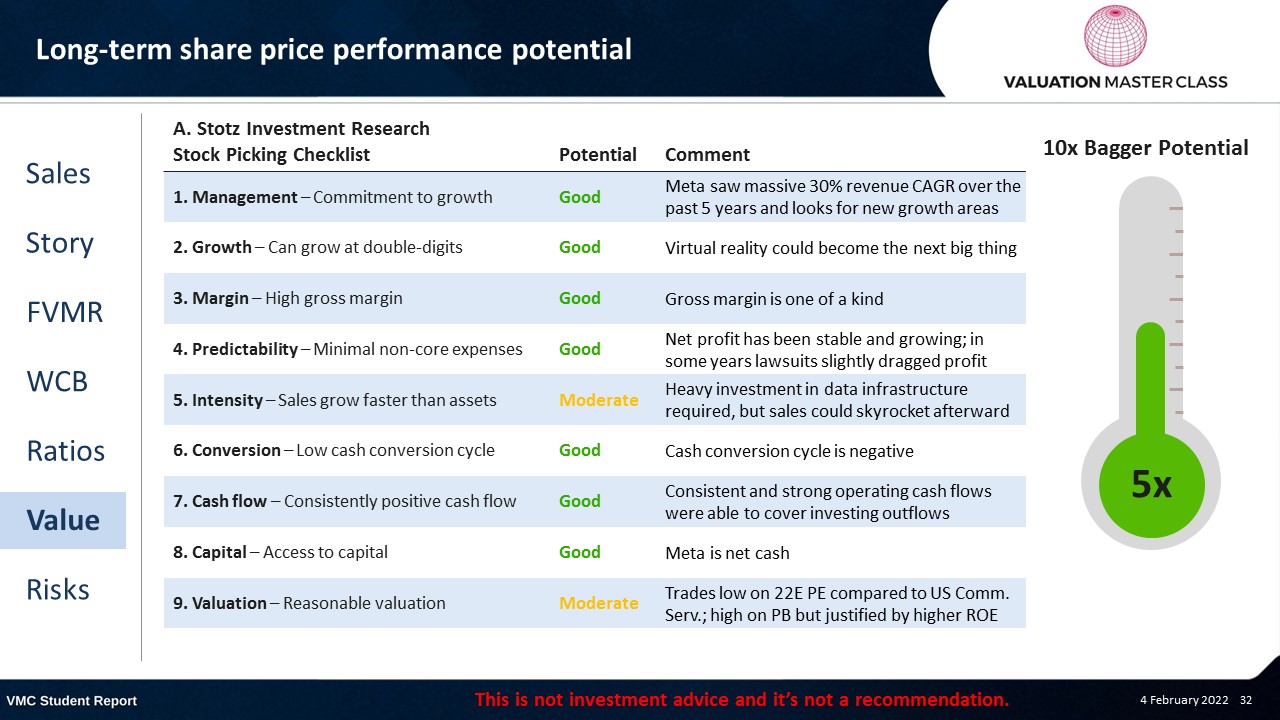

Long-term share price performance potential

Free cash flow – Meta Platforms

- Meta has delivered strongly on cash flow in the past and I expect rising FCFF in the future

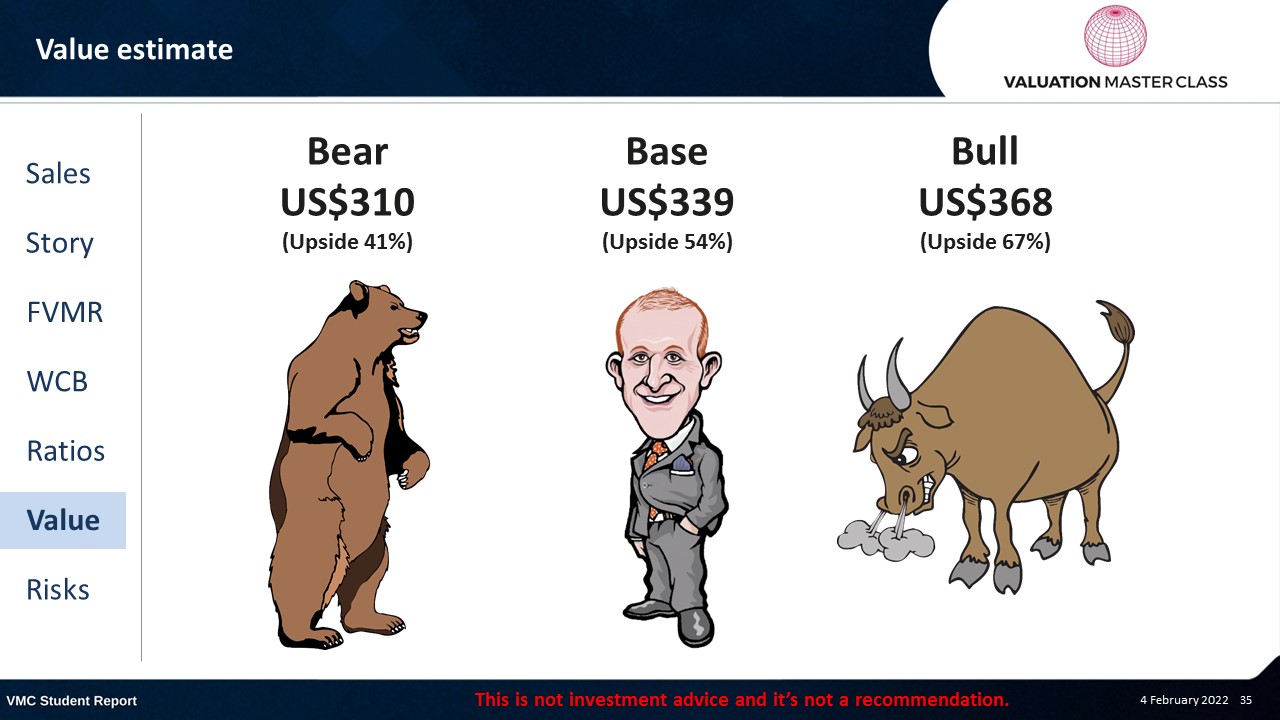

Value estimate – Meta Platforms

- I expect similar revenue growth compared to the consensus

- However, I am a bit more optimistic with regards to the margin in the short run

- Meta’s ability to increase prices for ads could offset the losses from the metaverse segment better than expected

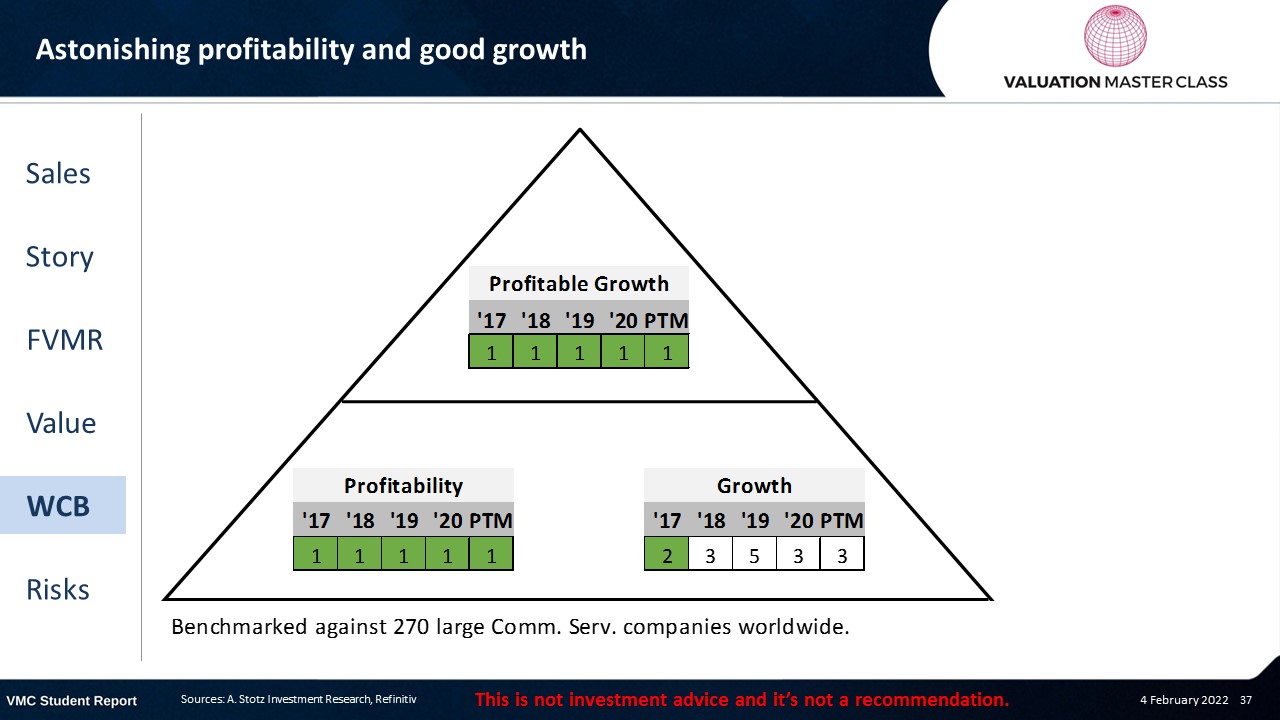

World Class Benchmarking Scorecard – Meta Platforms

- Identifies a company’s competitive position relative to global peers

- Combined, composite rank of profitability and growth, called “Profitable Growth”

- Scale from 1 (Best) to 10 (Worst)

Key risk is losing active users

- Failure to attract young people to its social media platforms

- Rising competition that grows out of nothing

- Metaverse could just be a bubble waiting to explode

- Regulatory pressure

Conclusions

- High pricing power could offset slowing pace of new user addition

- Investment in Metaverse is risky, but could become a double-digit growth engine

- Massive ROE makes it an attractive play

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.