Can the World’s Least Profitable Carmaker Turnaround?

Highlights:

- Restructuring is challenged by immense cost pressures

- Pure play approach to ride EV momentum

- Easing of supply constraints fosters revenue rebound

Download the full report as a PDF

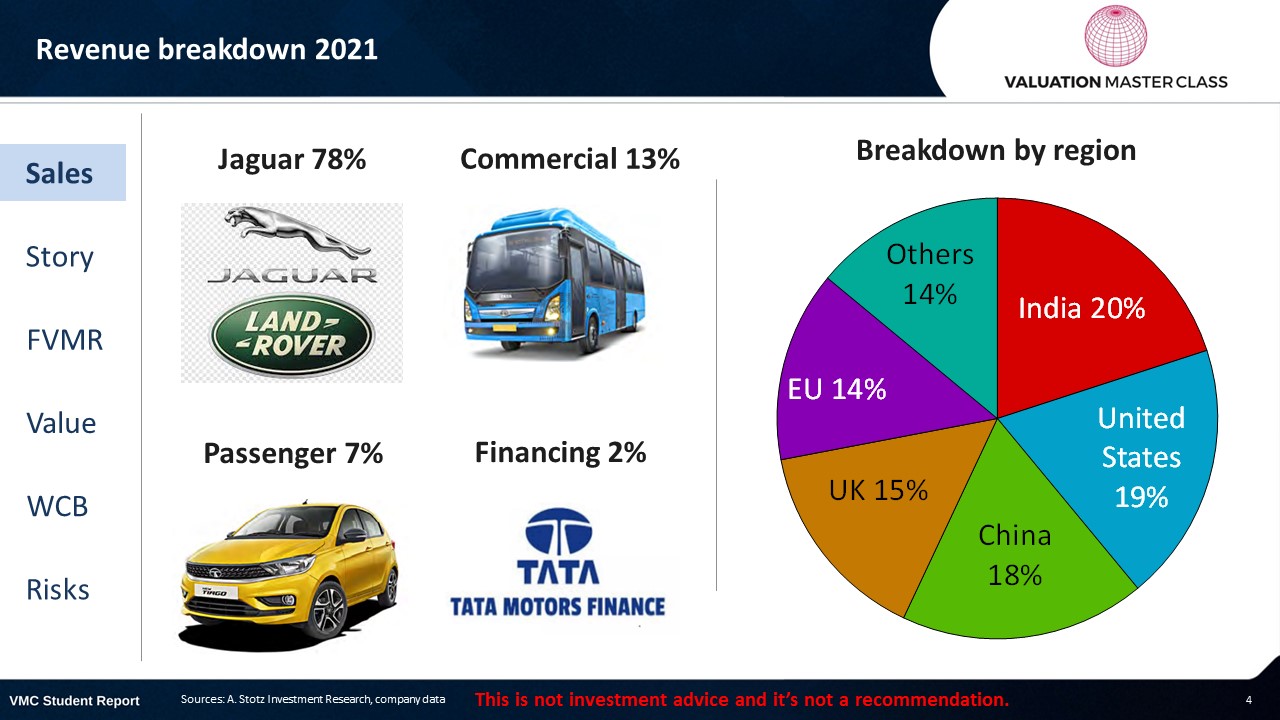

Tata Motors’ revenue breakdown 2021

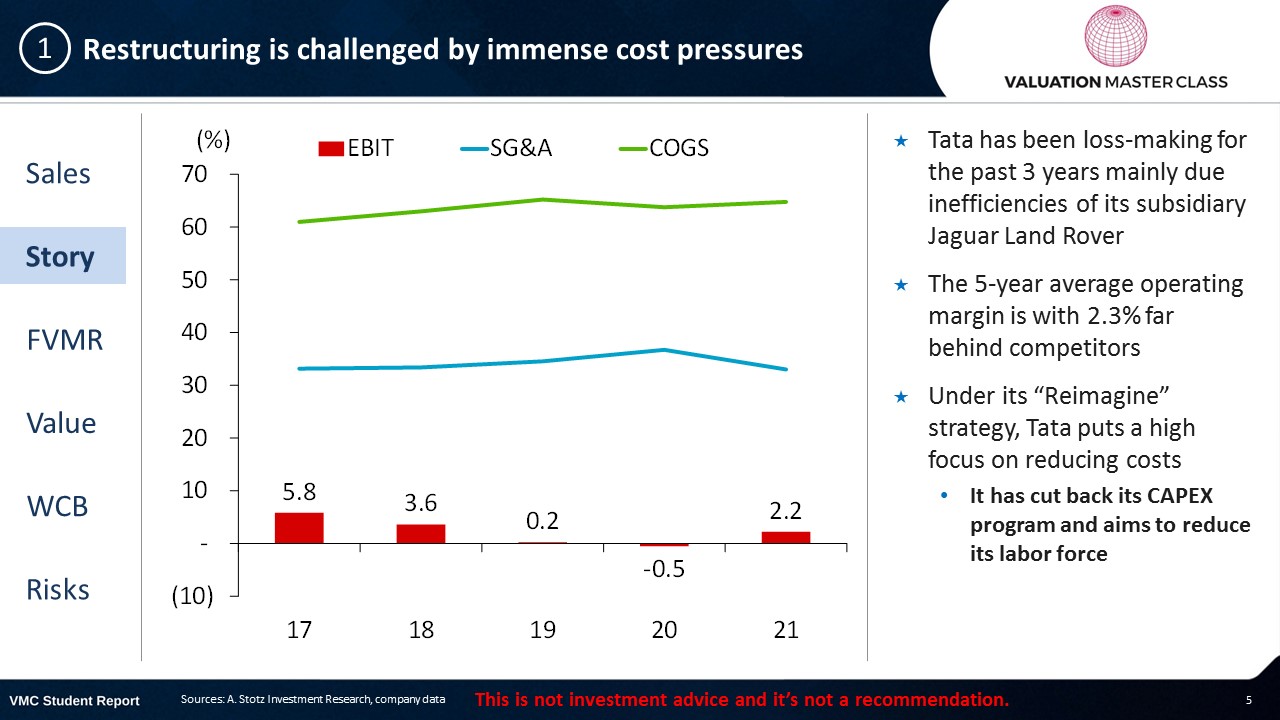

Restructuring is challenged by immense cost pressures

- Tata has been loss-making for the past 3 years mainly due inefficiencies of its subsidiary Jaguar Land Rover

- The 5-year average operating margin is with 2.3% far behind competitors

- Under its “Reimagine” strategy, Tata puts a high focus on reducing costs

- It has cut back its CAPEX program and aims to reduce its labor force

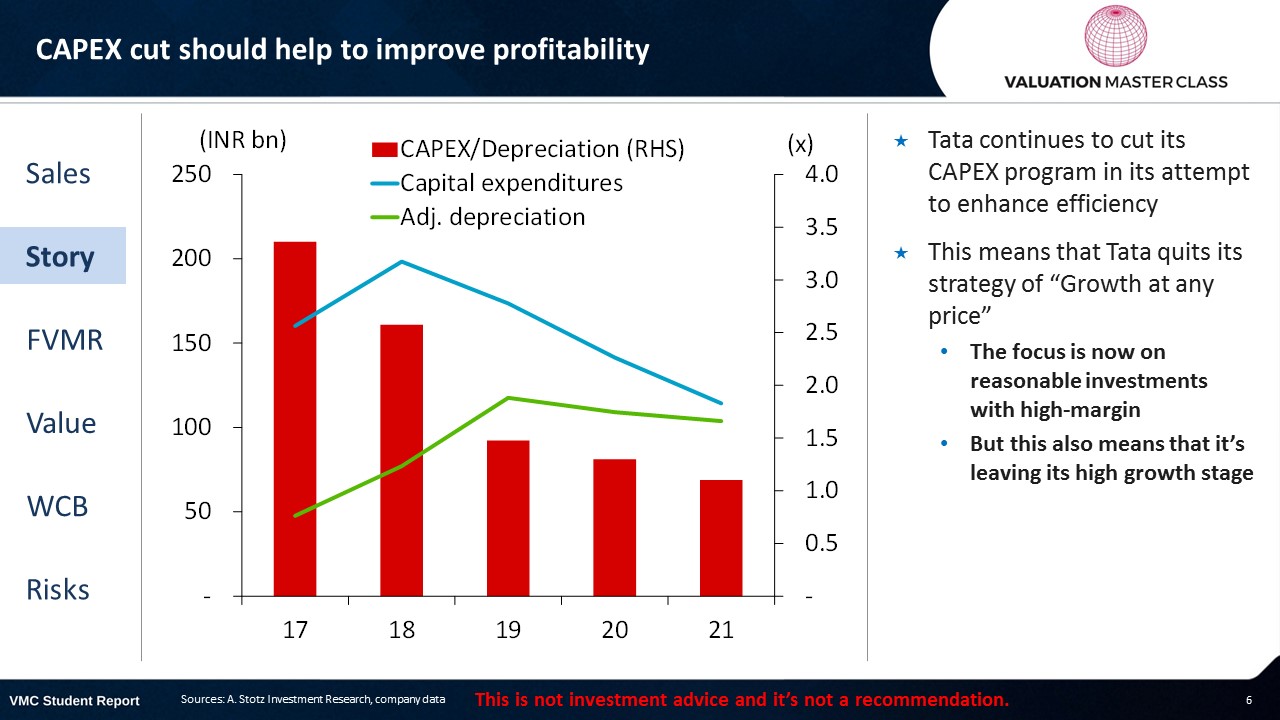

CAPEX cut should help to improve profitability

- Tata continues to cut its CAPEX program in its attempt to enhance efficiency

- This means that Tata quits its strategy of “Growth at any price”

- The focus is now on reasonable investments with high-margin

- But this also means that it’s leaving its high growth stage

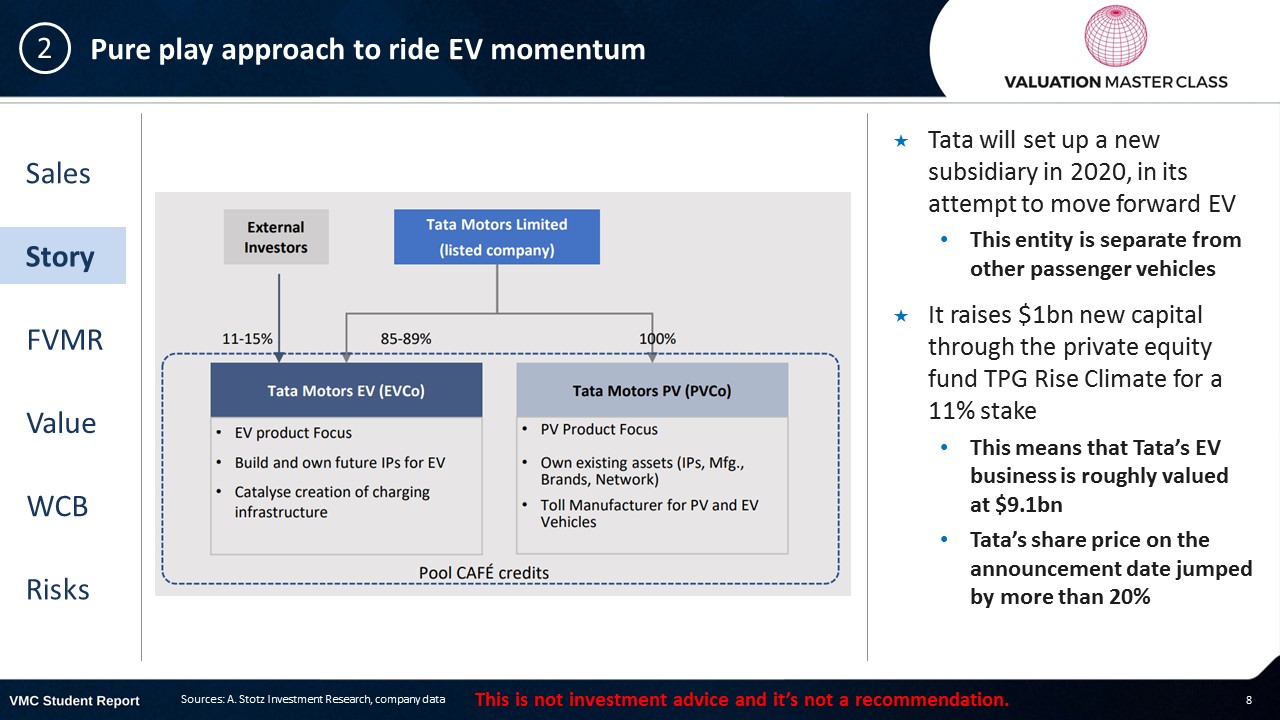

Pure play approach to ride EV momentum

- Tata will set up a new subsidiary in 2020, in its attempt to move forward EV

- This entity is separate from other passenger vehicles

- It raises $1bn new capital through the private equity fund TPG Rise Climate for a 11% stake

- This means that Tata’s EV business is roughly valued at $9.1bn

- Tata’s share price on the announcement date jumped by more than 20%

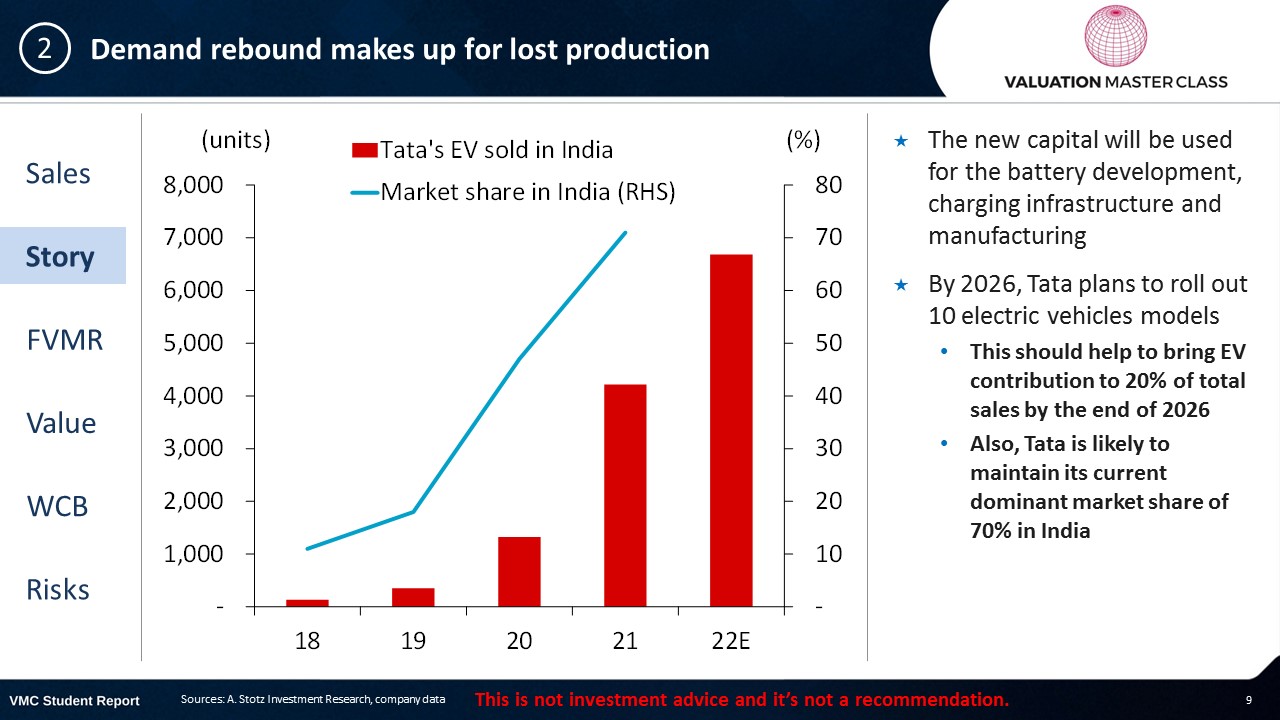

Demand rebound makes up for lost production

- The new capital will be used for the battery development, charging infrastructure and manufacturing

- By 2026, Tata plans to roll out 10 electric vehicles models

- This should help to bring EV contribution to 20% of total sales by the end of 2026

- Also, Tata is likely to maintain its current dominant market share of 70% in India

Easing of supply constraints fosters revenue rebound

- Semiconductor shortages have led to a limited production of 64k vehicles of its subsidiary Jaguar Land Rover in 2Q22

- This is down 18% YoY

- However, at the same time, it recognized a record order of 125k, which ensures strong revenue in the near term

- Riding the demand wave could bring double-digit revenue growth for the next 2 years

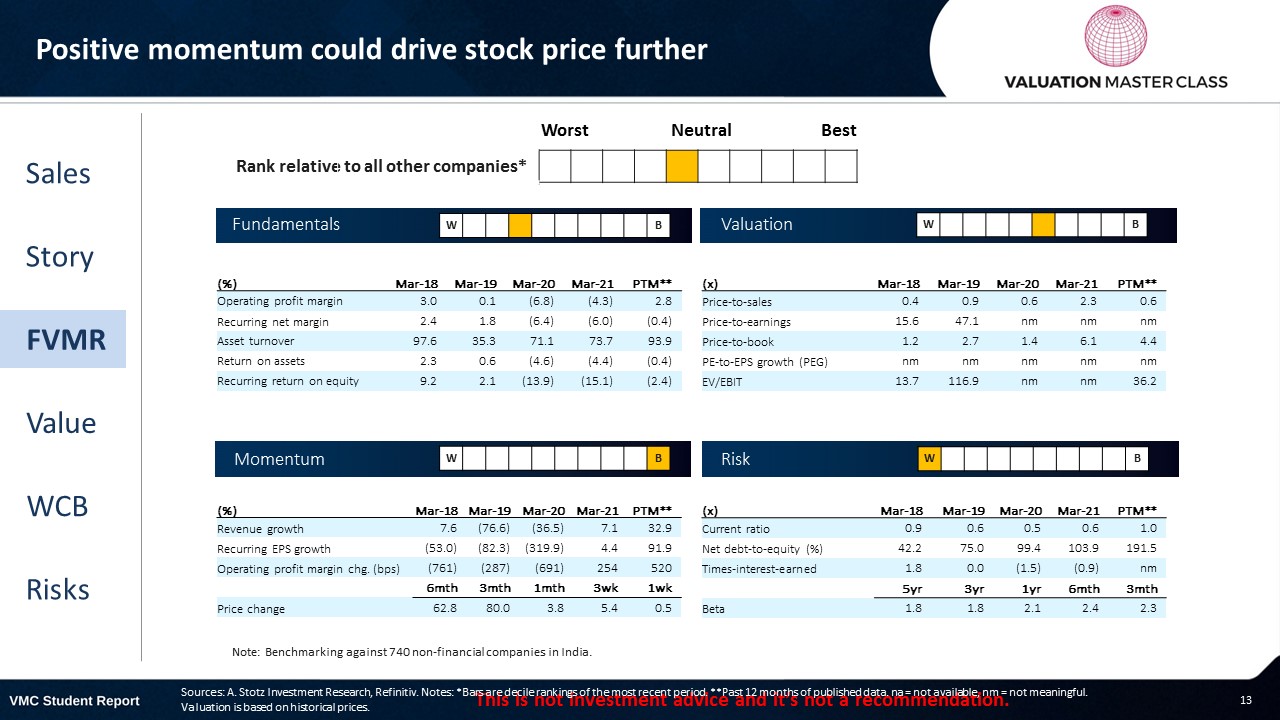

FVMR Scorecard – Tata Motors

- A stock’s attractiveness relative to stocks in that country or region

- Attractiveness is based on four elements

- Fundamentals, Valuation, Momentum, and Risk (FVMR)

- Scale from 1 (Best) to 10 (Worst)

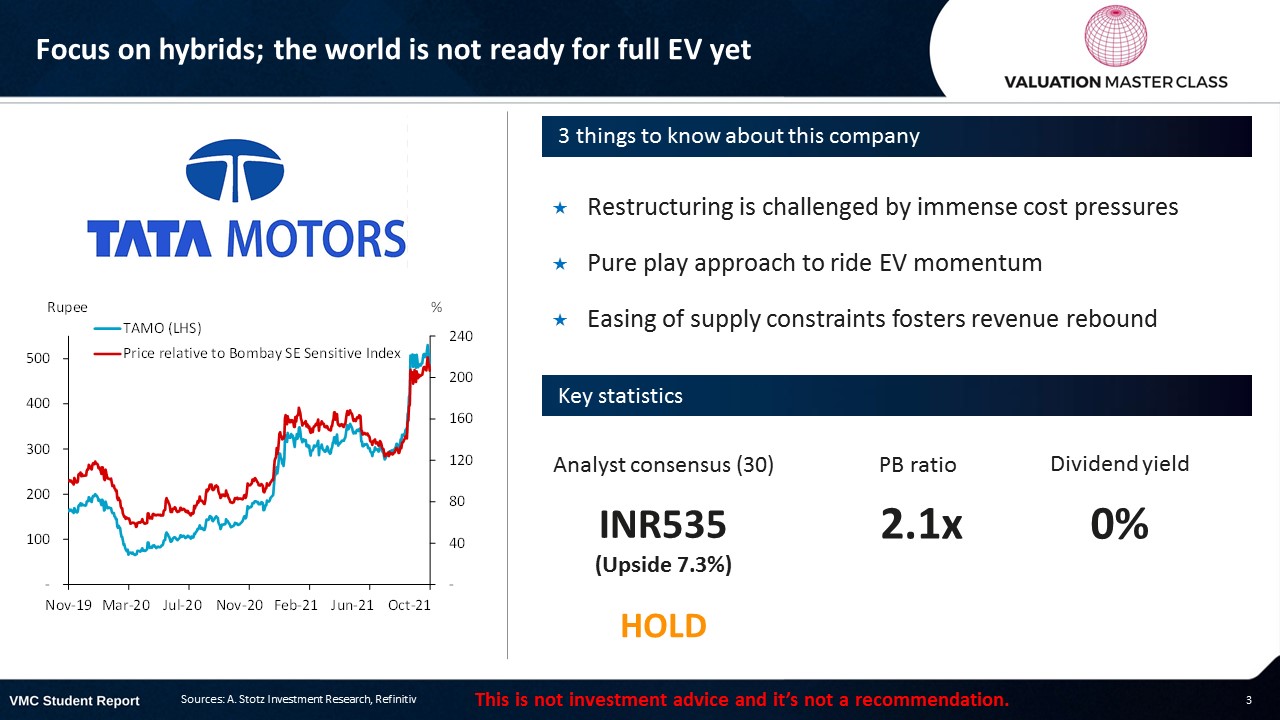

Consensus remains optimistic regarding carmaker recovery

- Analyst consensus does not see much further upside

- The stock price has shown strong momentum recently

- They are optimistic that Tata can converge its profitability to its peers over time

Get financial statements and assumptions in the full report

P&L – Tata Motors

- Tata is likely to recognize in 2022 for the 4th year in a row

- However, we expect that the company can turnaround its profitability in 2023

- Strong car sales and enhanced cost-cutting program should lead to a higher margin

Balance sheet – Tata Motors

- The company has a strong cash position, holding around 19% of its assets in cash as of 2021

- Net fixed assets grow gradually as Tata committed to a slowing CAPEX program

- Tata has a relatively high leverage

- Liabilities-to-assets ratio stood at 82% in 2021

- Retained earnings continue to decline in 2022 as Tata is likely to record a net loss again; we expect a turnaround in 2023

Cash flow – Tata Motors

- Given its losses over the past years, it did not pay out any dividends since 2016

- We assume that there will be no dividends at least for the next 3 years

Ratios – Tata Motors

- Revenue was hit during the pandemic, but order backlog is sufficient to generate double-digit revenue growth at least for the next 2 years

- Net margin could finally turn positive in 2023

- Tata has been among the worst profitable car companies in the past years

- It will be a challenge for the company to drive its EBIT margin to the industry average of 7-9%

- The company has relatively high leverage

Free cash flow – Tata Motors

- Despite the net losses, FCFF remained positive throughout the pandemic

- CAPEX is likely to stay much lower than 2017 to 2019 level

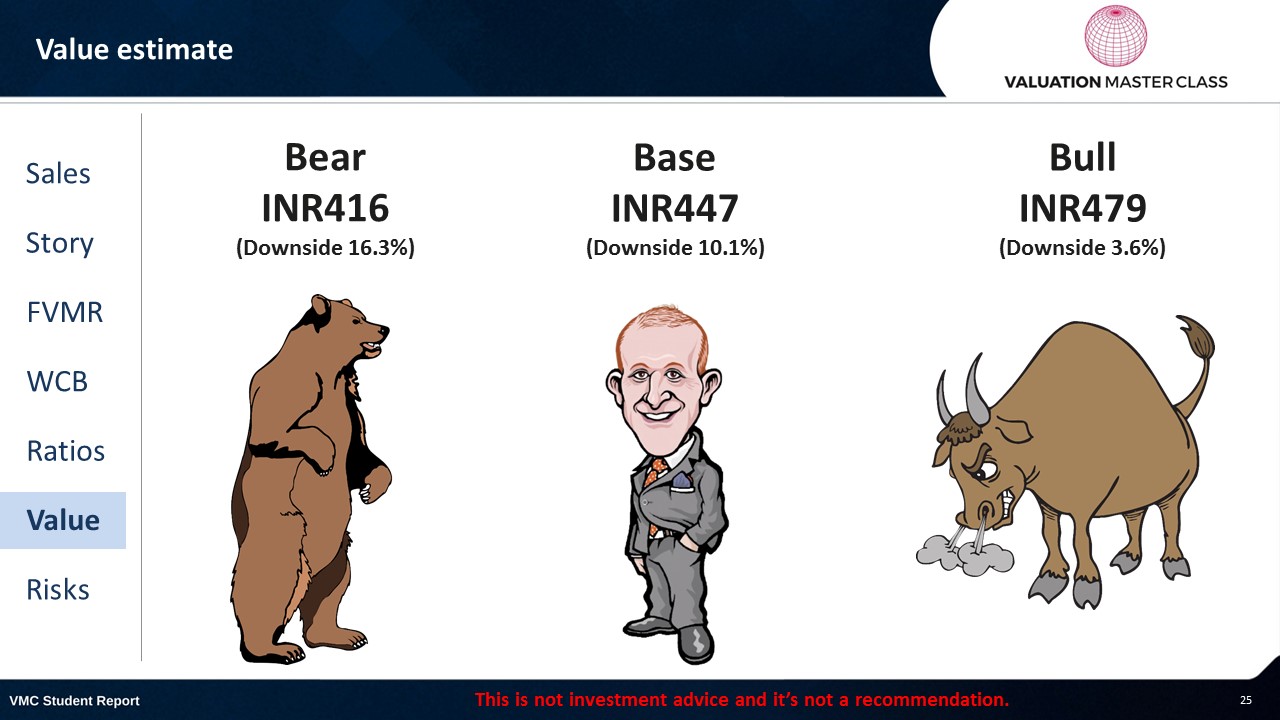

Value estimate – Tata Motors

- Global car sales likely to see strong rebound over the next 3 years

- Profitability is suppressed in the short run by higher raw material prices and semiconductor shortages

- Plus, cost cutting measures implemented by Tata may take time to turn beneficial

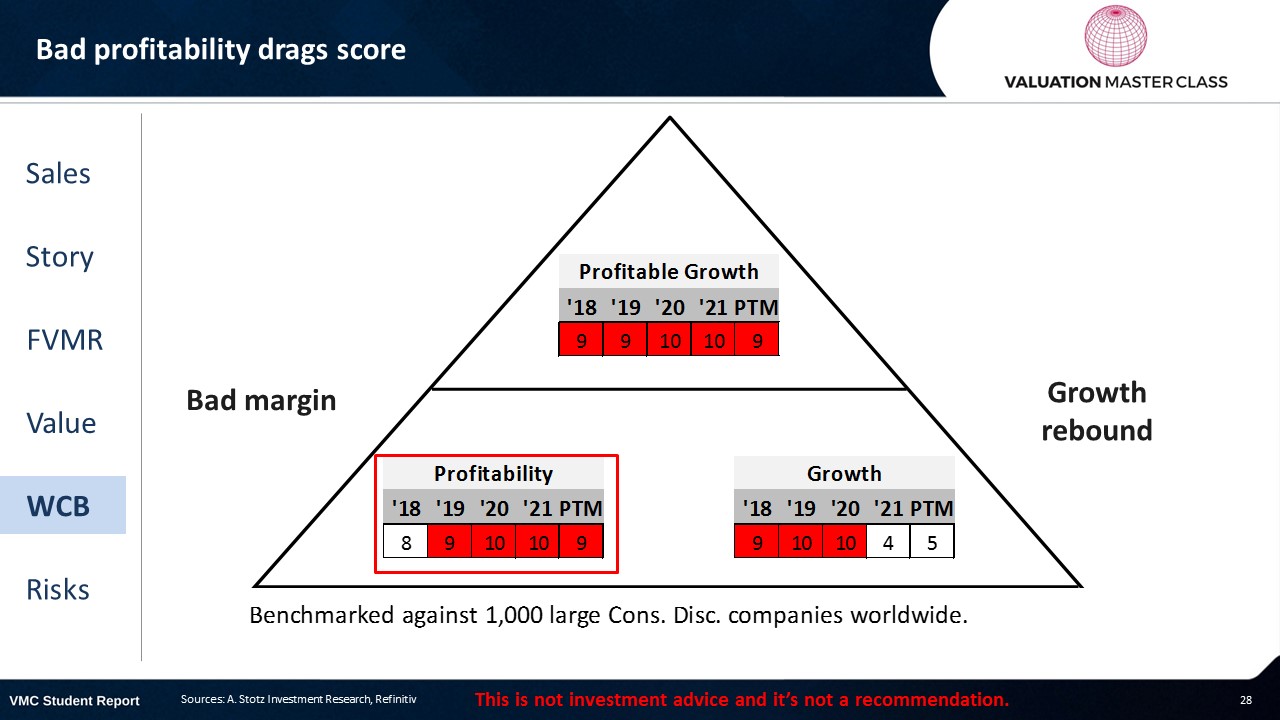

World Class Benchmarking Scorecard – Tata Motors

- Identifies a company’s competitive position relative to global peers

- Combined, composite rank of profitability and growth, called “Profitable Growth”

- Scale from 1 (Best) to 10 (Worst)

Key risk is ongoing supply chain disruptions

- Ongoing supply chain disruptions create shortages (e.g., semiconductor chips) and increase production costs

- Failure to implement adequate cost cutting measures

- EV investment could not be sufficient to keep up with competitors

Conclusions

- Value addition through newly formed EV subsidiary might be overhyped

- Slowing CAPEX plan could constraint production growth

- No dividend policy requires return generation from price

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.