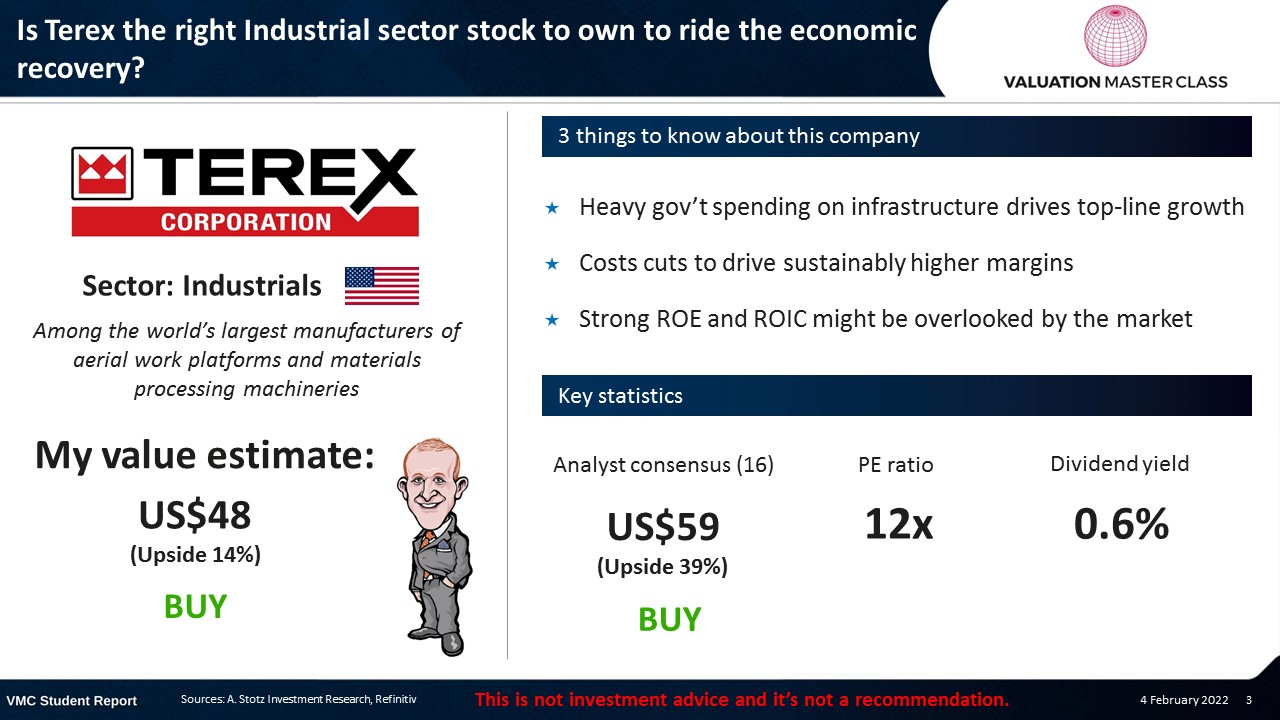

Is Terex the Right Industrial Sector Stock to Own to Ride the Economic Recovery?

Highlights:

- Heavy gov’t spending on infrastructure drives top-line growth

- Costs cuts to drive sustainably higher margins

- Strong ROE and ROIC might be overlooked by the market

Download the full report as a PDF

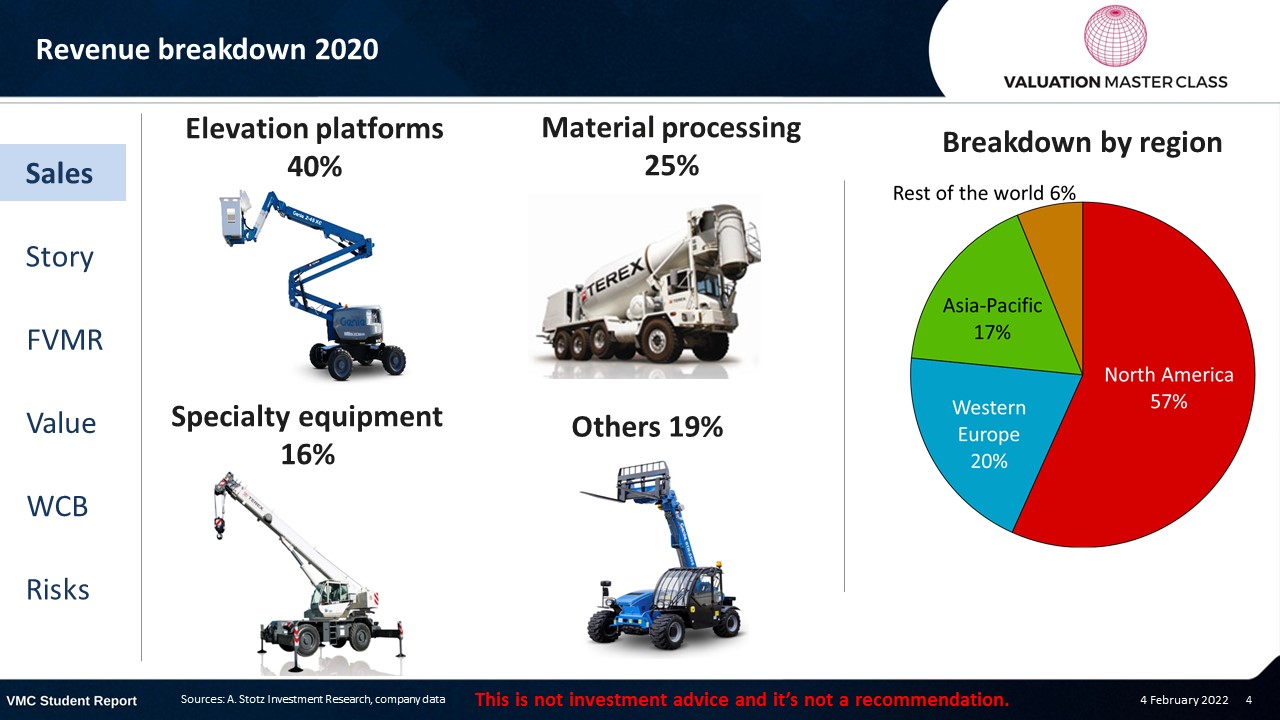

Terex Corporation’s revenue breakdown 2020

Sideward movement could last much longer

- Throughout the past year, the stock price mainly moved sideward

- Since 3Q21, the 50DMA moved in line with 200DMA, providing no clear signal yet

- Volume RSI has been weak recently

- Currently, it is at the 50%-line, which also does not help to derive a meaningful conclusion

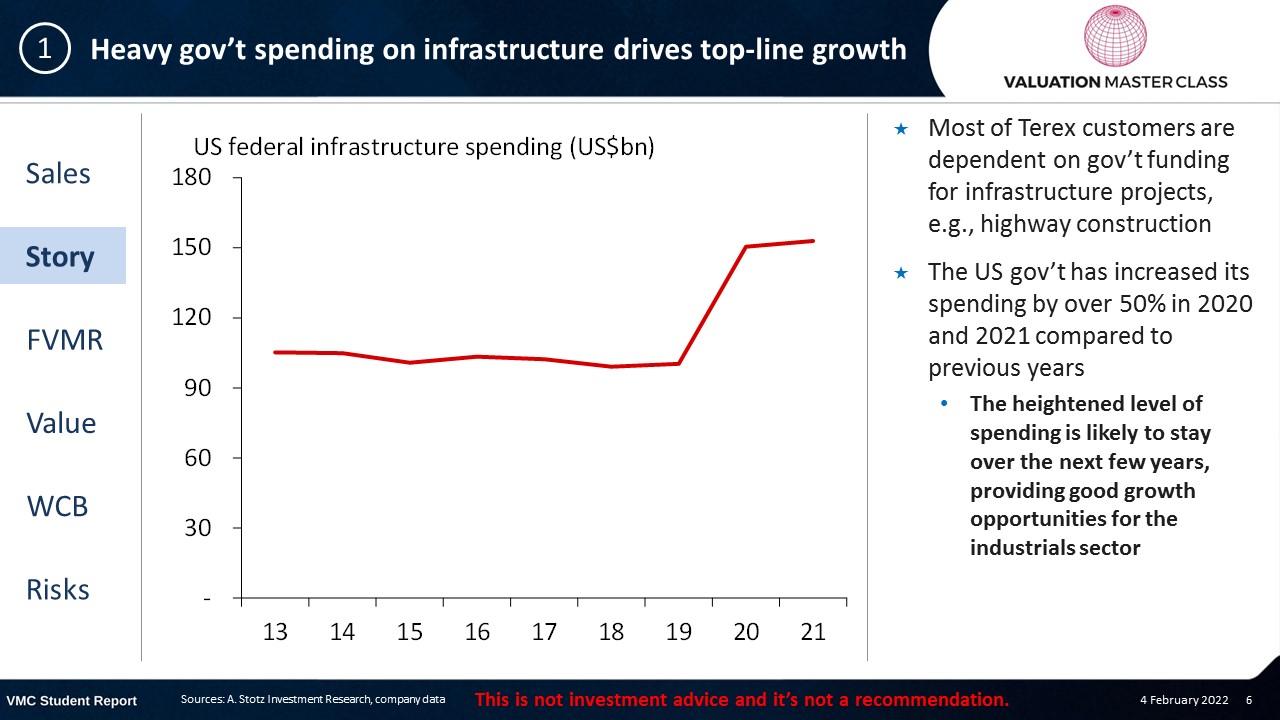

Heavy gov’t spending on infrastructure drives top-line growth

- Most of Terex customers are dependent on gov’t funding for infrastructure projects, e.g., highway construction

- The US gov’t has increased its spending by over 50% in 2020 and 2021 compared to previous years

- The heightened level of spending is likely to stay over the next few years, providing good growth opportunities for the industrials sector

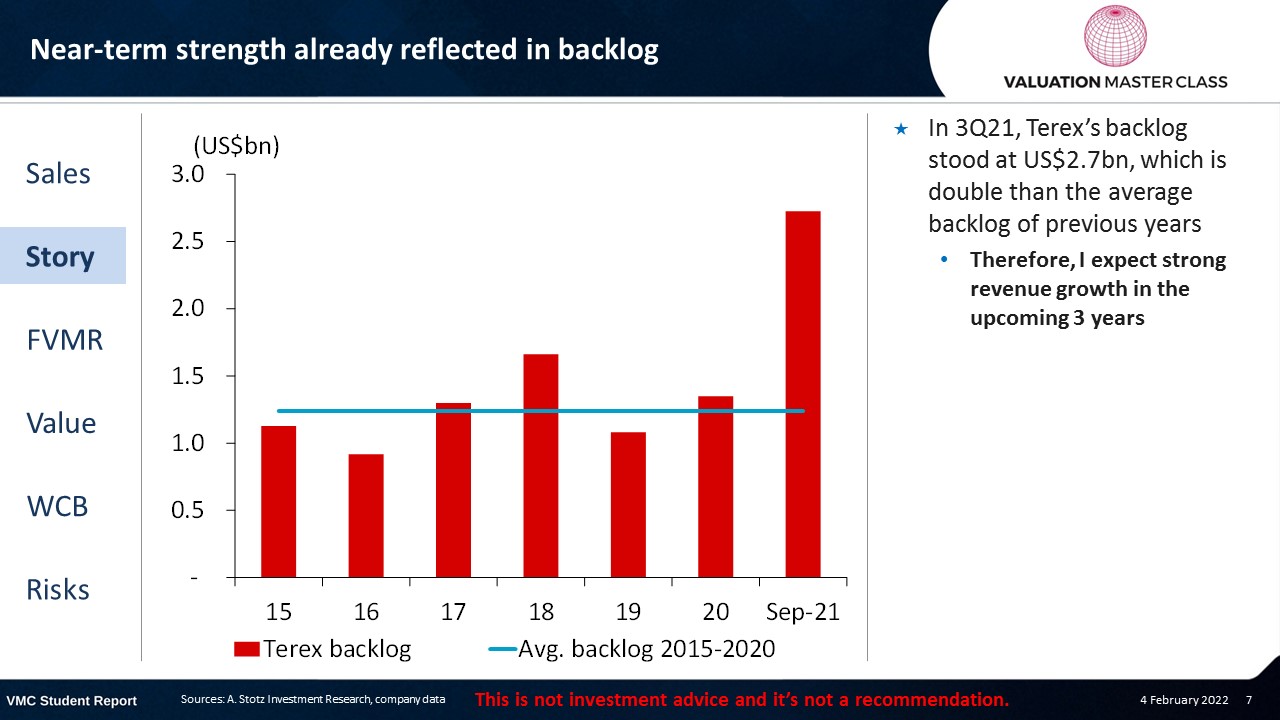

Near-term strength already reflected in backlog

- In 3Q21, Terex’s backlog stood at US$2.7bn, which is double than the average backlog of previous years

- Therefore, I expect strong revenue growth in the upcoming 3 years

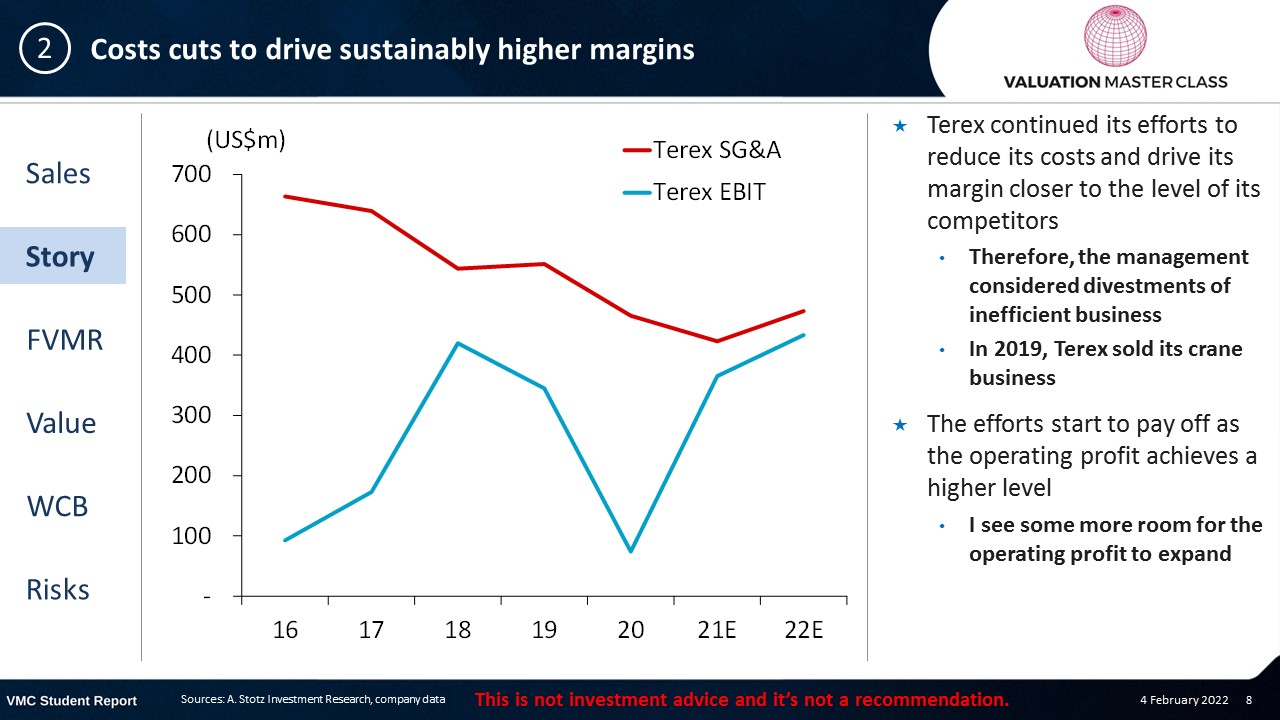

Costs cuts to drive sustainably higher margins

- Terex continued its efforts to reduce its costs and drive its margin closer to the level of its competitors

- Therefore, the management considered divestments of inefficient business

- In 2019, Terex sold its crane business

- The efforts start to pay off as the operating profit achieves a higher level

- I see some more room for the operating profit to expand

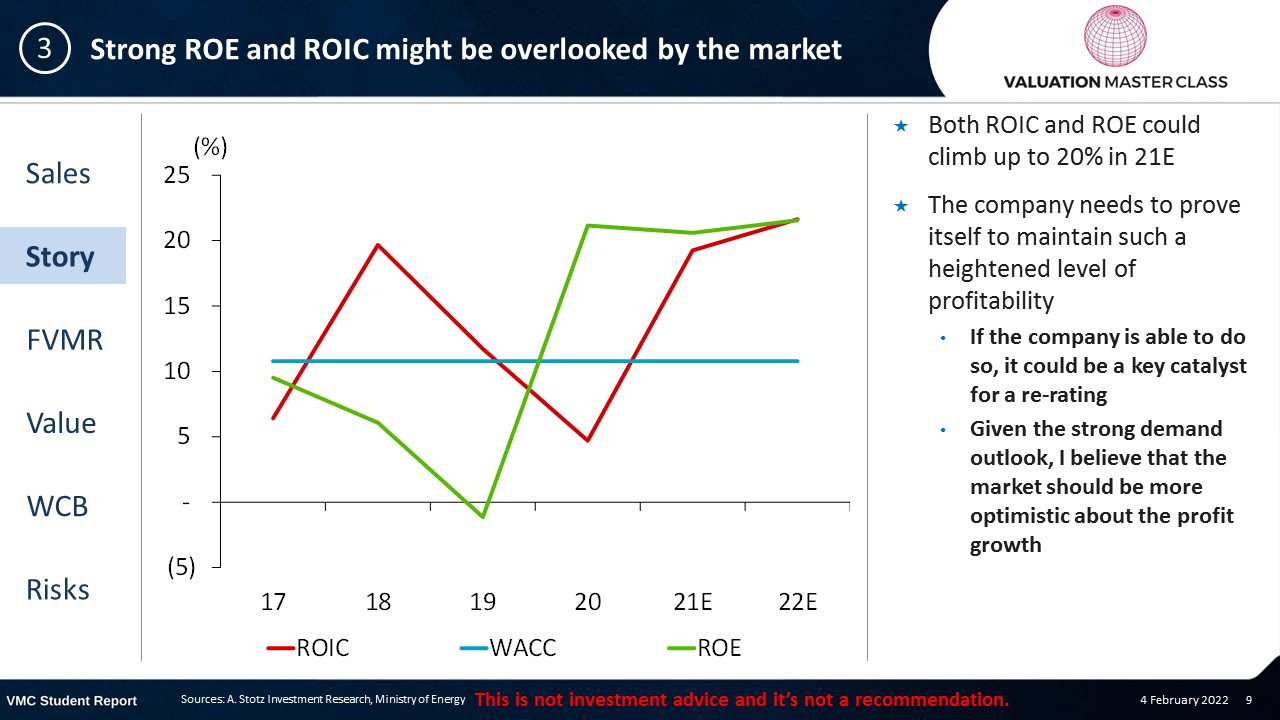

Strong ROE and ROIC might be overlooked by the market

- Both ROIC and ROE could climb up to 20% in 21E

- The company needs to prove itself to maintain such a heightened level of profitability

- If the company is able to do so, it could be a key catalyst for a re-rating

- Given the strong demand outlook, I believe that the market should be more optimistic about the profit growth

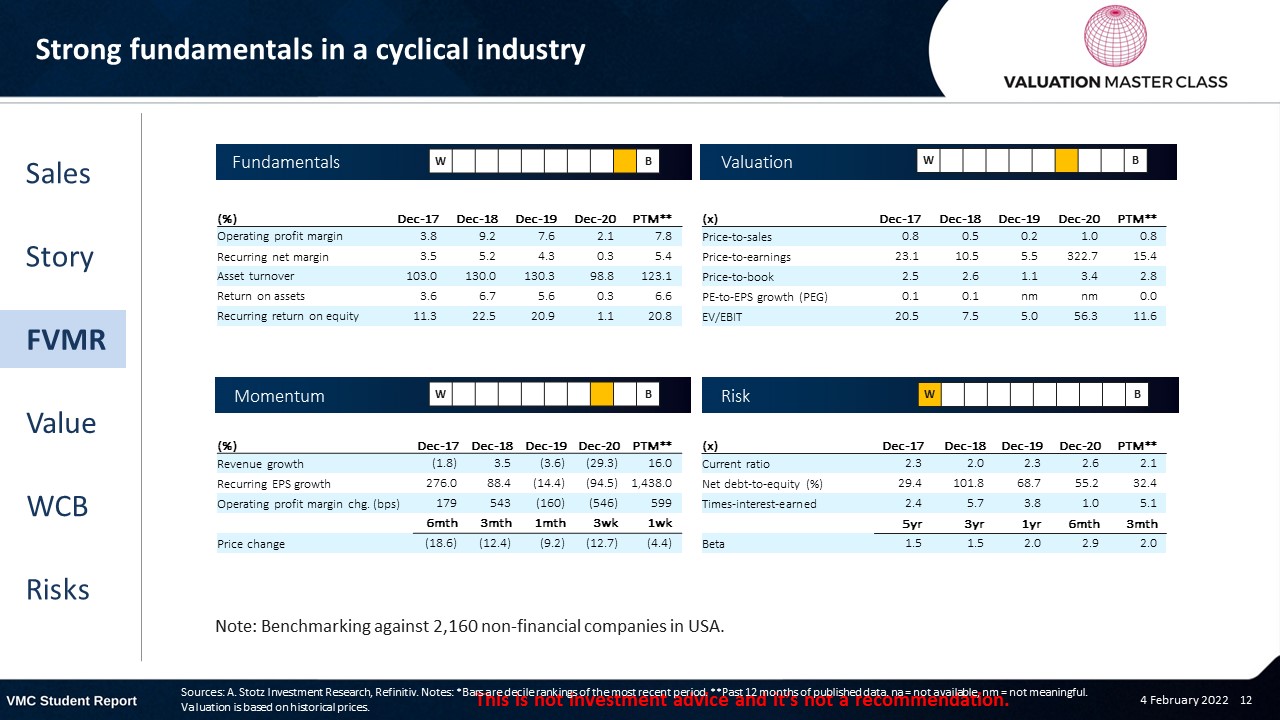

FVMR Scorecard – Terex Corporation

- A stock’s attractiveness relative to stocks in that country or region

- Attractiveness is based on four elements

- Fundamentals, Valuation, Momentum, and Risk (FVMR)

- Scale from 1 (Best) to 10 (Worst)

Consensus sees strong upside

- The majority of analysts issued a BUY recommendation, while 6 analysts recommend a HOLD

- Consensus expects strong revenue prospects, and a rising margin

- Considering growing infrastructure spending, the company could realize the targets

Get financial statements and assumptions in the full report

P&L – Terex Corporation

- The company is likely to turnaround its loss in 2020 and recognize strong profits in 21E and 22E

Balance sheet – Terex Corporation

- Significant increases in inventories and receivables as sales volume likely to ramp up as shown by the strong backlog

- The company started to reduce its long-term debt

- In 3Q21, its net debt-to-equity ratio stood at 0.3x, compared to 0.6x in 2020

Ratios – Terex Corporation

- The company is characterized by a strong efficiency, which also boosts future return on equity

- With the increased focus on its most profitable products, Terex could return to a gross margin above 20%, with further room to improve over time

Long-term share price performance potential

Free cash flow – Terex Corporation

- FCFF has been consistently positive, and there is no reason to assume differently in the future

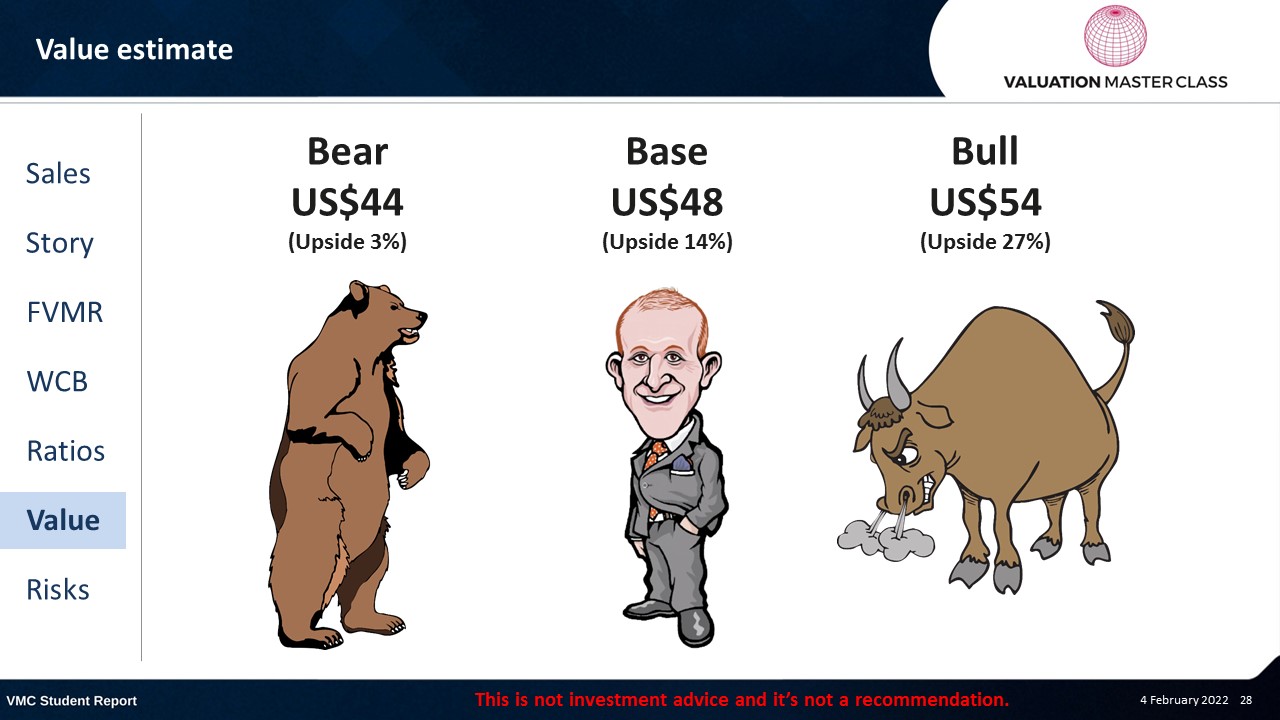

Value estimate – Terex Corporation

- Similar to consensus, I expect strong revenue and a margin improvement

- Terex is likely to ride the demand wave induced by gov’t infrastructure support

- The company is highly cyclical reflected in the above-average beta of 1.25x

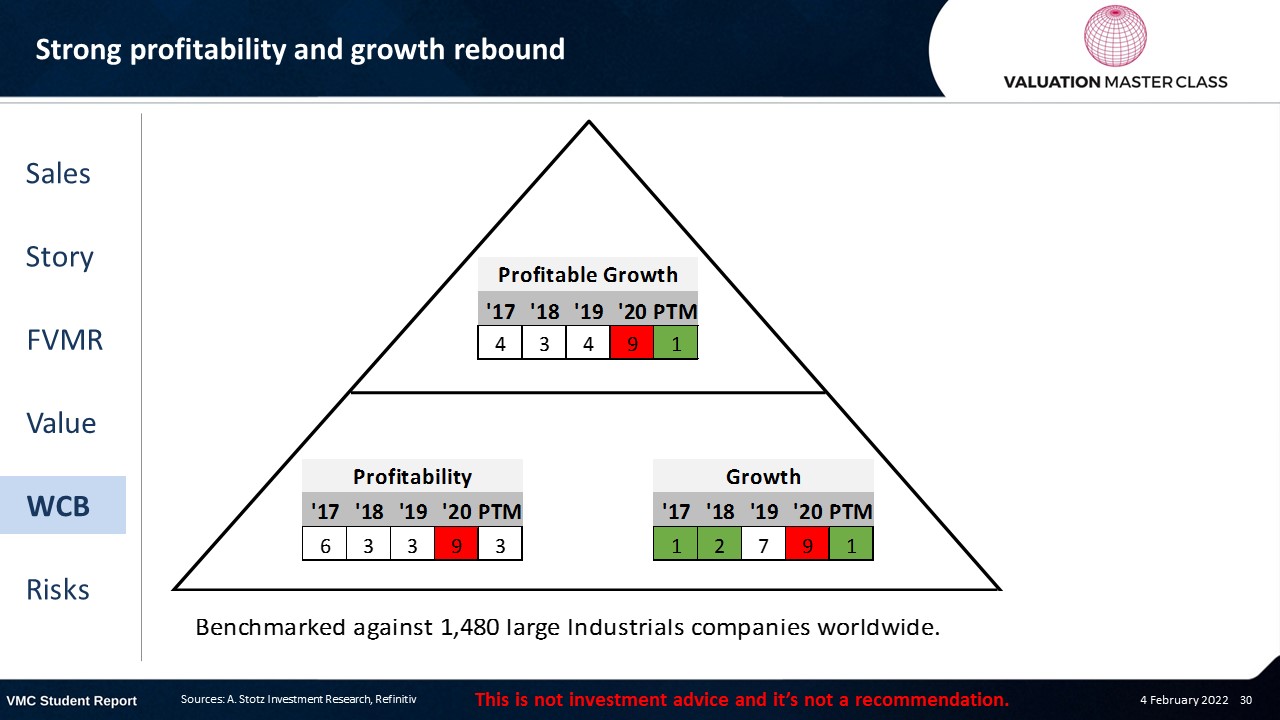

World Class Benchmarking Scorecard – Terex Corporation

- Identifies a company’s competitive position relative to global peers

- Combined, composite rank of profitability and growth, called “Profitable Growth”

- Scale from 1 (Best) to 10 (Worst)

Key risk is intensified price competition

- Low-cost competitors from China could result in loss of customers

- Its customers are dependent on gov’t spending

- Dependency on suppliers can lead to volatile margin

Conclusions

- Ramp up of gov’t infrastructure spending makes it worth to look at industrial companies

- Terex has room to expand its margin, making it a profitable growth play

- Valuation is relatively cheap, trading at a 50% discount

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.