Would You Buy Tesla on 19x 2025 Earnings?

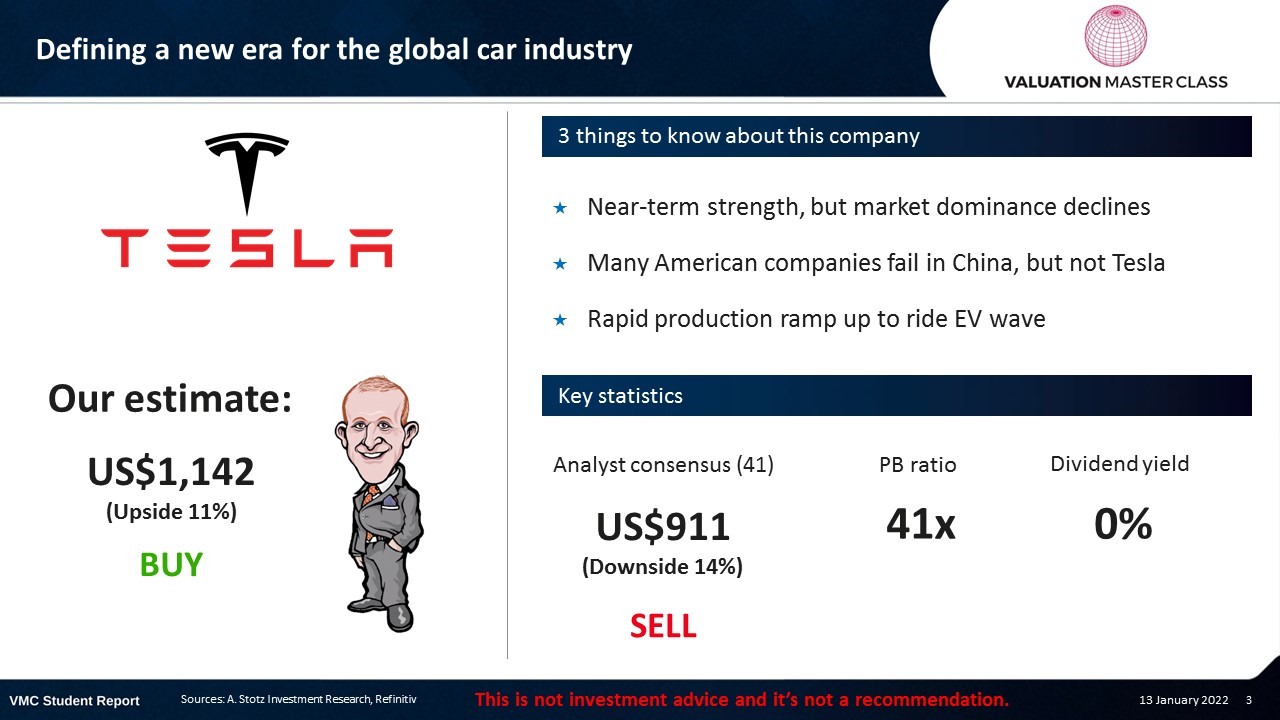

Defining a new era for the global car industry

Highlights:

- Near-term strength, but market dominance declines

- Many American companies fail in China, but not Tesla

- Rapid production ramp up to ride EV wave

Download the full report as a PDF

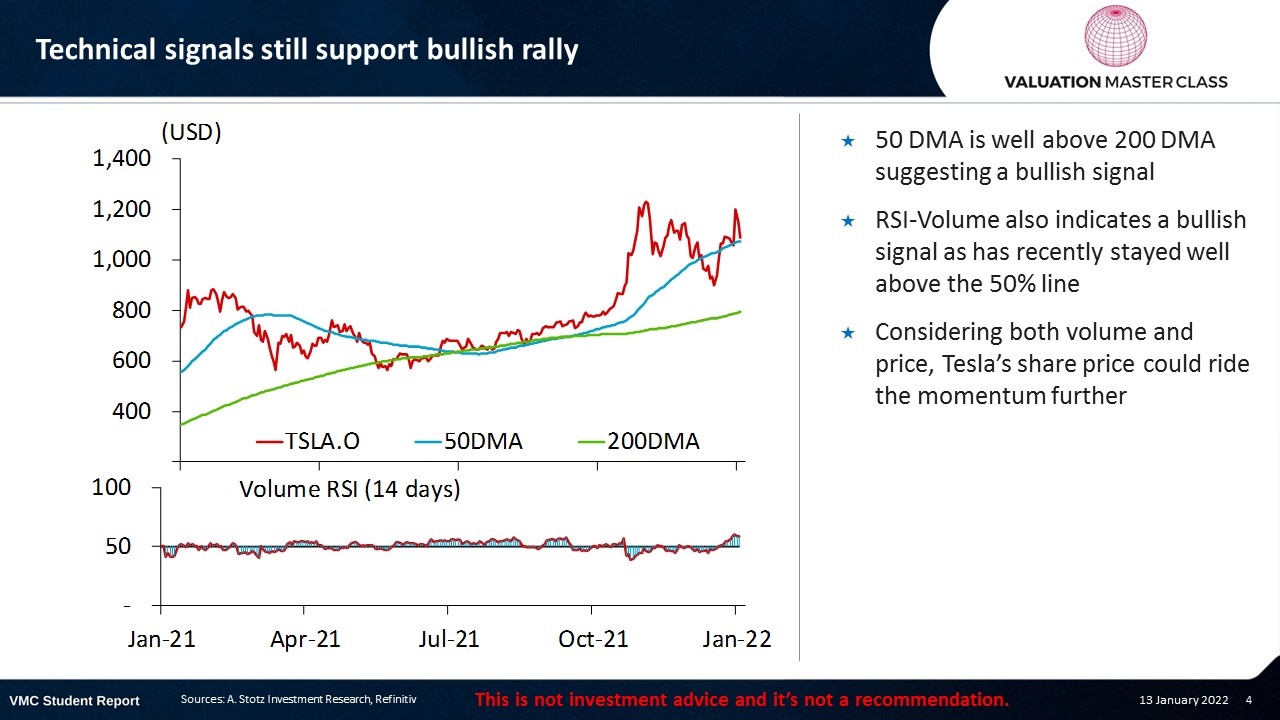

Technical signals still support bullish rally

- 50 DMA is well above 200 DMA suggesting a bullish signal

- RSI-Volume also indicates a bullish signal as has recently stayed well above the 50% line

- Considering both volume and price, Tesla’s share price could ride the momentum further

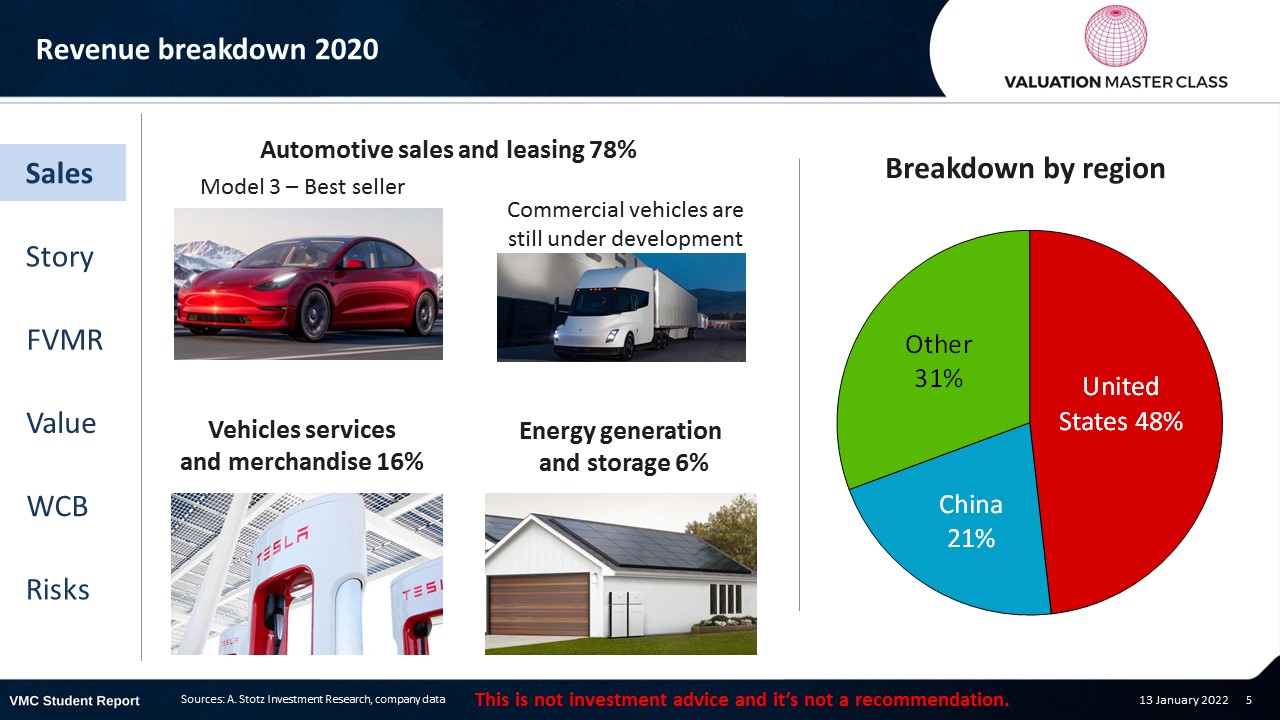

Tesla’s revenue breakdown 2020

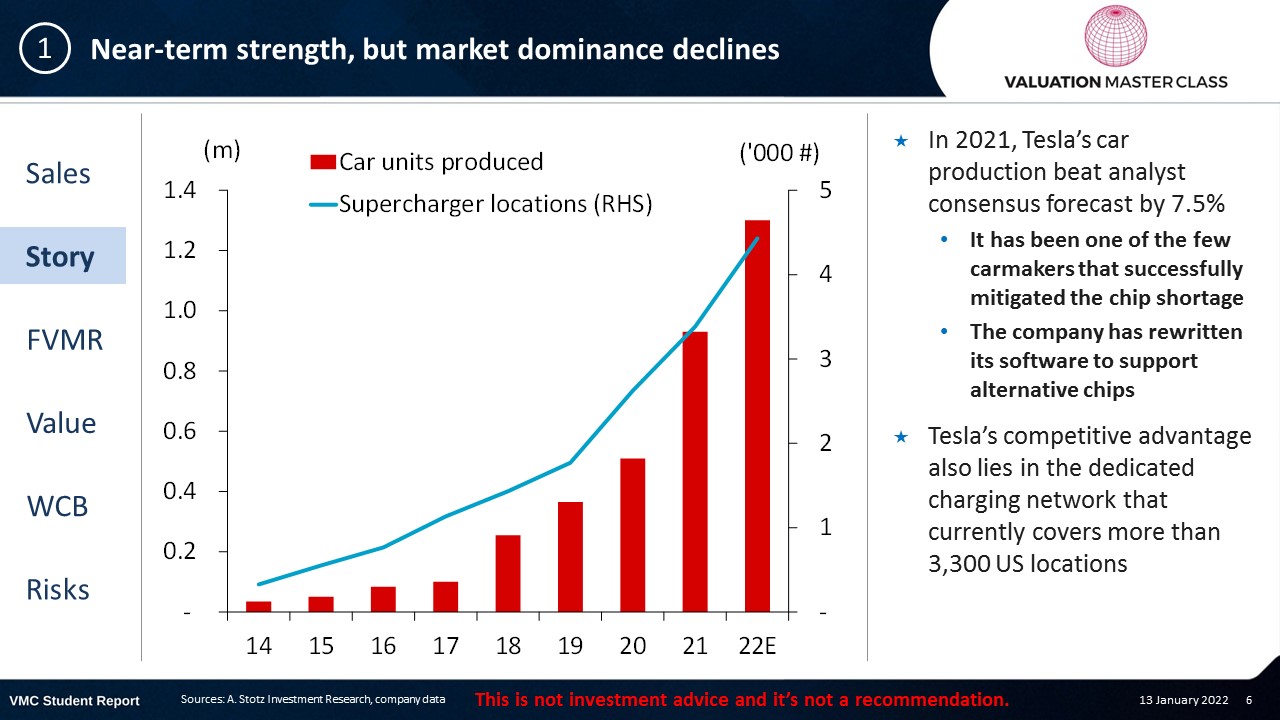

Near-term strength, but market dominance declines

- In 2021, Tesla’s car production beat analyst consensus forecast by 7.5%

- It has been one of the few carmakers that successfully mitigated the chip shortage

- The company has rewritten its software to support alternative chips

- Tesla’s competitive advantage also lies in the dedicated charging network that currently covers more than 3,300 US locations

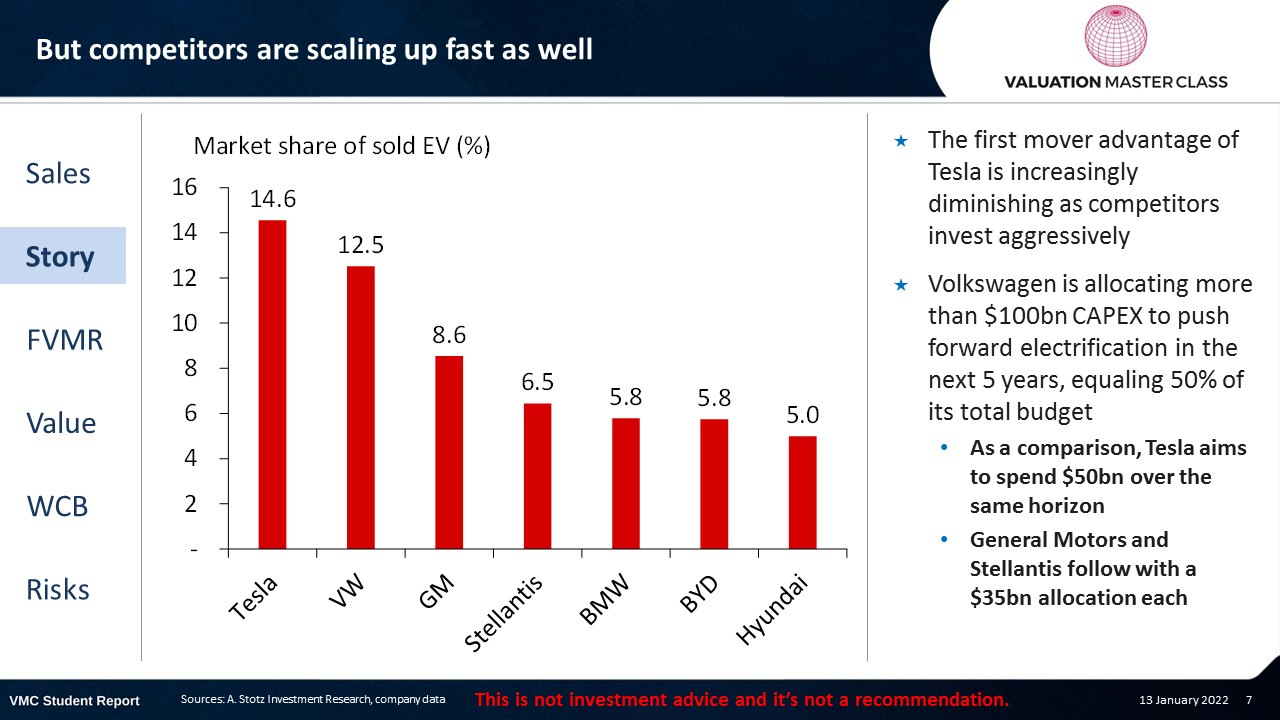

But competitors are scaling up fast as well

- The first mover advantage of Tesla is increasingly diminishing as competitors invest aggressively

- Volkswagen is allocating more than $100bn CAPEX to push forward electrification in the next 5 years, equaling 50% of its total budget

- As a comparison, Tesla aims to spend $50bn over the same horizon

- General Motors and Stellantis follow with a $35bn allocation each

Many American companies fail in China, but not Tesla

- China is the dominant market for EV and battery development

- In 2021, Chinese EV sales was 3.3m vehicles, 8x the US

- Tesla recognized early the potential and expanded its Chinese factory to an annual production volume of 600,000

- China already makes up 29% of Tesla’s sales in 2021 and that contribution could go up much further

Why do most big US companies fail in China?

- Some reason why they failed

- Lack of localization strategy

- Government and regulatory hurdles

- Underestimating domestic competitors

- Rapidly changing market

- Lack of understanding cultural sensitivity

Tesla needs China and China needs Tesla

- Despite the US-China trade war, China has supported Tesla in building its Giga Factory

- It granted Tesla cheap access to land, tax incentives, and low interest rate loans

- In return, Tesla is supposed to advance the Chinese EV industry and stimulate competition for technological progress

- This is also called the “catfish effect”

- The interdependency allows Tesla to succeed in China while other US companies fail

Rapid production ramp up to ride EV wave

- Tesla’s builds its factories at an enormous speed through ready-made construction elements

- Chinese factory took just 168 days to build

- Two further factories in Berlin and Austin are on the edge of opening, adding more than 1m cars additional capacity by 2022

- We expect the company to reach an annual production of 2m cars by 2023

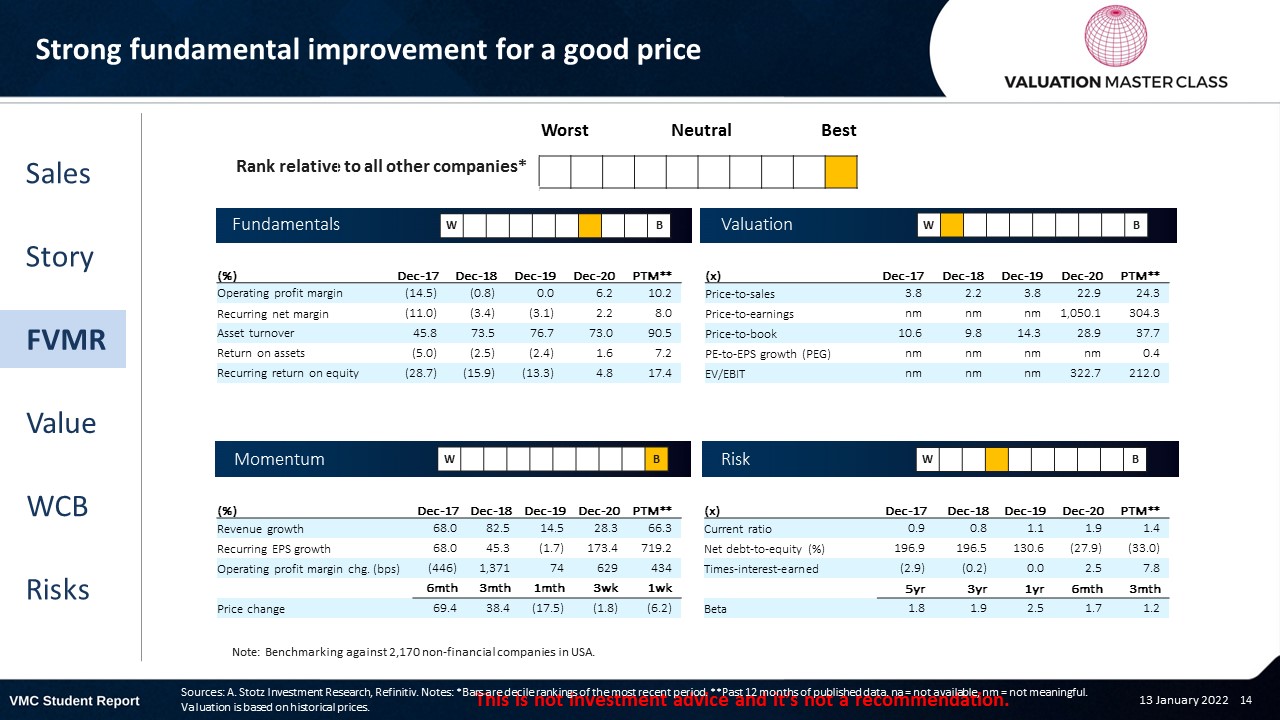

FVMR Scorecard – Tesla

- A stock’s attractiveness relative to stocks in that country or region

- Attractiveness is based on four elements

- Fundamentals, Valuation, Momentum, and Risk (FVMR)

- Scale from 1 (Best) to 10 (Worst)

Consensus remains optimistic regarding profitability turnaround

- Analysts are mixed about Tesla’s outlook

- High dispersion among analysts is usually really rare

- There are 10 sell or strong sell recommendations

- Consensus expects revenue to continue growing at a very fast pace

Get financial statements and assumptions in the full report

P&L – Tesla

- We expect the company to fulfill its massive growth expectations reflected in high double-digit revenue growth

- Tesla started to write black ink on its bottom-line in 2020

- With the production ramp up, it generates growing profits from 2021E onward

Balance sheet – Tesla

- The company has a massive cash position, holding around 37% of its assets in cash as of 2020

- Heavy fixed assets investments necessary to maintain leading role in climate neutral car development

- Tesla has moderately low leverage

- Liabilities-to-assets ratio stood at 56% in 2020

- Retained earnings should turn positive in 2022E

- Higher jumps in retained earnings would come from increased profitability

Cash flow statement – Tesla

- Operating cash flow could turn massively positive in 2022

- Heavy CAPEX in 2021E due to the development of two further Giga factories

- We expect Tesla to continue massive spending on its technology e.g., batteries

Ratios – Tesla

- Tesla laid the foundation for high growth by expanding its production capacity fast

- As Tesla moves closer to full capacity of its existing plans, we expect a higher efficiency

- Tesla has the ability to achieve an above-industry margin

- Tesla became a net cash company in 2020

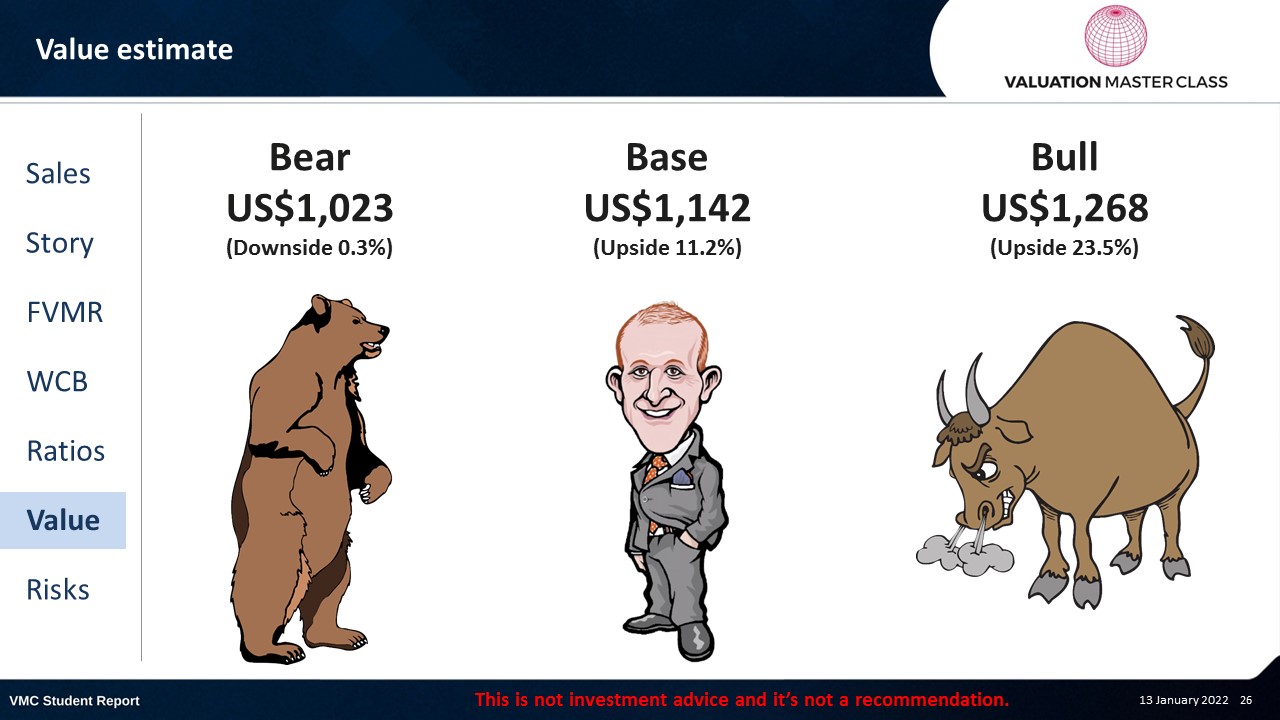

Value estimate – Tesla

- While Tesla trades on a massive PE-multiple, we should not neglect its vast growth potential

- Looking at the 2022E PEG multiple, Tesla trades slightly below the average US Consumer Discretionary company

- In this valuation let’s say that Tesla re-rates to its industry average

TSLA: Possibilities – Buying on 19x 2025 PE

- If volume goes from 1m units in 2021 to 6m in 2025

- And the price of cars rises by about 10% per year

- This would mean revenue grows from US$51bn in 2021 to US$446bn in 2025

- Assume that net profit margin rises from 2021’s 9% to 12% by 2025

- Then Tesla would produce profit in 2025 of US$54bn

- The company currently trades on 213x 2021 PE

- But that would fall to 90x 2022, 37x 2023, 25x 2024, and 19x 2025

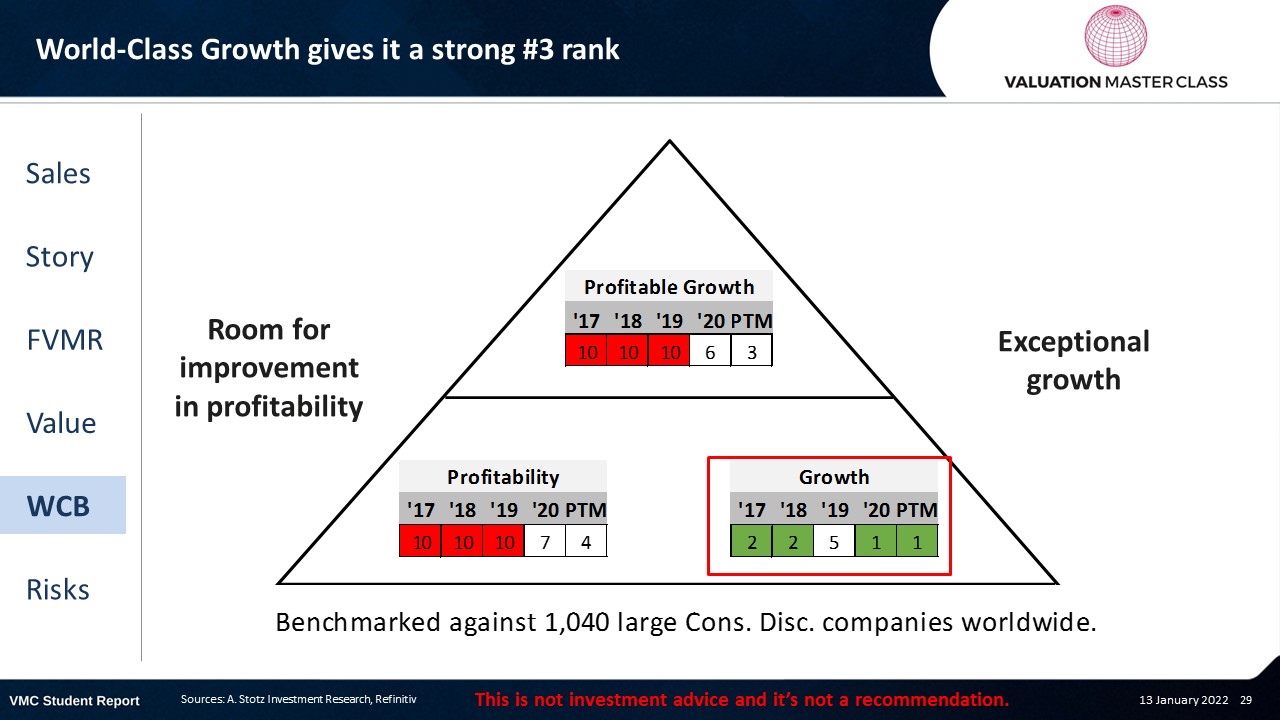

World Class Benchmarking Scorecard – Tesla

- Identifies a company’s competitive position relative to global peers

- Combined, composite rank of profitability and growth, called “Profitable Growth”

- Scale from 1 (Best) to 10 (Worst)

The key risks for Tesla

- Competitors could close the tech gap faster than expected as they invest heavily

- Adverse regulatory changes in China could hamper the business

- Sentiment can lead to volatile stock price movement

Conclusions

- Tesla’s success lies in the EV-dominant country China

- Delivering high profitability could convince skeptics

- Tesla’s high PE sounds more reasonable when relating it to its massive growth prospects

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.