Mistake #8: Choosing an Unreasonable Cost of Equity

I’ve narrowed down all the mistakes I’ve seen in my career over the last 25 years as an analyst, as a head of research, and in the Valuation Master Class, into these top nine. Check out the previous posts in the series here.

- Overly optimistic revenue forecasts

- Underestimating expenses causing unrealistic profit forecasts

- Growing fixed assets slower than revenue

- Confusing growth with maintenance Capex

- Forecasting drastic changes in the cash conversion cycle

- Underestimating working capital investment

- Valuing a stock using the calculated Beta

- Choosing an unreasonable cost of equity

- Not properly fading the return on invested capital

A very common error that I’ve seen made by analysts is discounting the future cash flows of a business at an unreasonable cost of equity (COE)—which is why it’s valuation mistake #8. Analysts are notorious for trying to manipulate their COE to get the outcome in valuation that they want. As head of research, my focus was always to prevent them from making these types of errors by giving them some framework to consider.

Why Is This Important?

The discount rate can massively impact the final valuation; and even if forecasts are perfect, it can cause a wrong estimation of value. A firm’s COE represents the compensation that the market demands in exchange for bearing the risk of owning that stock. Remember, it’s the market that is setting the COE ─ not you.

Now, of course, as an analyst or as a stock picker, we think we know the right COE. Therefore, we’re going to set it ourselves based on what we think; and, theoretically, we’re going to think that the market is wrong. It’s important to have a good structure and framework if you’re going to hedge that bias.

If your assumption of the COE is too high, you’ll underestimate the value of the company. And if it’s too low, then, your estimation of the value of the company will be just too high.

Analysts can often get lost in determining the various components of COE and miss the big picture. There’s the risk-free rate; market return; market premium; and beta, to mention a few. There are so many ways of slicing a pie, but that doesn’t change the size of the pie.

What Cost of Equity Do You Use?

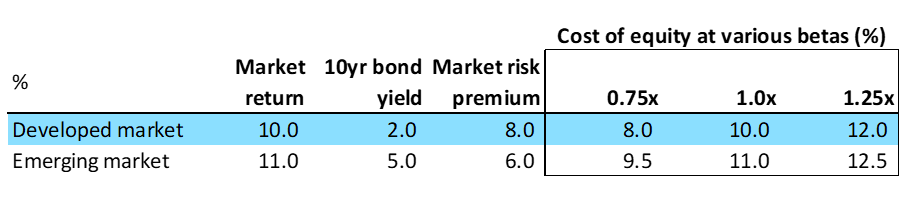

I’ve included the results below here of a simple study I recently undertook; where I wanted to help determine a reasonable COE in both emerging and developed markets. I studied the risk-free rate, the beta, and the market risk premium of these markets over the recent years to come up with a range of COE. The risk-free rate was based on the 10-year government bond yield in each country, while the market risk premium was calculated based on the Gordon growth model using the implied equity risk premium.

Here’s the end data:

[Fig. 8.1 Cost of Equity at Various Betas]

I’ve grouped developed markets and emerging markets. And you can see that based on the findings, a reasonable range of COE is about 8% to 13%. (Check out mistake #7 in this series for more on why I choose a beta of 0.75, 1.0, and 1.5.) The results show that emerging markets’ COE was slightly higher than developed markets due to the higher risk that investors are bearing.

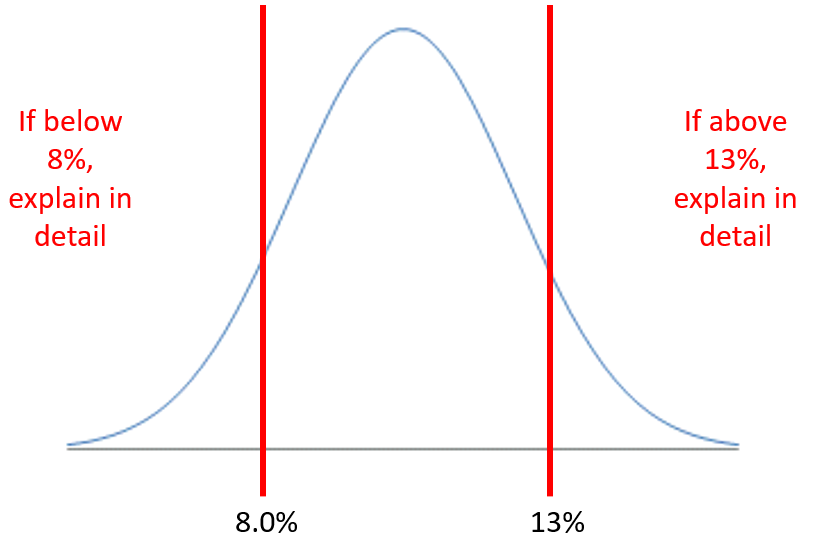

To keep it simple, it’s worth knowing that the majority of the outcomes are going to be in the range of 8.0% and 13.0%. This gives us a nice bell curve graph of data to demonstrate danger areas:

[Fig 8.2 Range of COE]

How to Avoid This Mistake

If your COE arrives outside of that range, you’re going to need a decent explanation as to why. If you want to go outside of the beta or the COE range, do it; just know that you need to explain in more detail why you are choosing that very high or very low COE.

And if you’ve done that, then you’ve really done your job as a stock picker or the valuation expert. You are showing your significant point of difference, and that’s skill.

Most of the time I’ve seen situations where this happened though, where analysts can never explain why COE is too high or too low, leads me to believe it’s just a common mistake.

Chapter 8 Conclusion

- Don’t get lost in the components of the COE

- Instead, focus on the end results

- Too high or too low COE can significantly change your estimation of a firm’s fair value

- Based on our study, we consider a COE ranging from 8% to 13% to be a good rule of thumb

Don’t forget to watch the video that accompanies this chapter:

The final installment in this series covers not properly fading return on invested capital.

The Valuation Master Class is an on-demand online course that trains attendees to become company valuation experts. Graduates can confidently value any company and possess the in-demand industry skills needed to succeed as investment bankers, asset managers, equity analysts, or value investors.

Click here to learn more about Valuation Master Class Foundation.

The Valuation Master Class Boot Camp presents the Valuation Master Class Foundation material in a 6-week guided online course format. Daily live sessions, teamwork, progress tracking, and the intensive nature help guide attendees to completion. The final company valuation project and presentation is tangible evidence of the attendee’s practical valuation experience and dedication to building a career in finance.