Toyota Valuation: Is the World’s Largest Carmaker Undervalued?

What Is Toyota Worth? A DCF Valuation Case Study

Toyota Motor Corporation (TYO: 7203 / NYSE: TM) is the world’s largest automaker by volume, producing over 10 million vehicles annually across a diversified powertrain portfolio that includes internal combustion engines (ICE), hybrids, hydrogen fuel cells, and battery electric vehicles (BEV). This company valuation case study uses a discounted cash flow (DCF) model to estimate Toyota’s intrinsic value, finding approximately 40% upside relative to its market price at the time of analysis.

| Metric | Value |

|---|---|

| Ticker | TYO: 7203 / NYSE: TM |

| Market Cap (2026) | ~$318 billion USD |

| Revenue (TTM) | ~$322 billion USD |

| Trailing P/E | ~13.5x |

| Forward P/E | ~12.5x |

| EV/EBITDA | ~12.2x |

| Price-to-Book | ~1.0x at time of analysis |

| WACC (case study) | 6.4% |

| DCF Intrinsic Value (base case) | JPY 2,509 / share |

| Upside at Analysis | ~40% |

The key question: Can Toyota’s multi-pathway strategy, combining hybrids, hydrogen, and a cautious approach to battery EVs, create more shareholder value than the “EV-only” approach pursued by competitors like Tesla and BYD? Here is how we valued Toyota using a DCF framework, and what the analysis reveals about valuing cyclical companies in a transitioning industry.

Starting your finance career?

Our Starter Program gives you the foundational skills to land your first analyst role — DCF valuation, financial modeling, and interview prep included.

ICE Vehicles Are Not Going Away, Providing Ongoing Revenue Support

- Toyota is the world’s largest car manufacturer, ranked by a composite of market cap, revenue, and employees.

- The company has been a leader in alternative energy solutions such as hybrids and hydrogen-powered vehicles. The prior president has said that the company will “not simply repeat the approach of other companies” when it comes to electric vehicles (EV).

- Toyota points out the limited battery range, scarcity of lithium resources, lack of a charging network, and consumer preferences towards internal combustion engines (ICE).

- And developing markets in South America, Asia, and Africa could be decades away from having the infrastructure to implement a massive EV rollout; Toyota is well-positioned to grow with these markets.

- Over the next five years, we expect Toyota to return to its pre-pandemic average growth level and achieve a CAGR of 6.9%.

Why Does Toyota’s EV Strategy Matter for Valuation?

Toyota’s approach to the EV transition is not just a strategic question; it is a valuation question. The market has punished Toyota’s stock price precisely because investors question whether its multi-pathway approach can compete against pure-EV players. Understanding which valuation method to use and how to model strategic uncertainty is essential for any analyst covering the automotive sector.

The debate breaks down into three valuation-relevant pillars:

1. ICE Vehicles Are Not Going Away (Revenue Protection)

- Developing markets in South America, Asia, and Africa are decades from full EV infrastructure

- ICE and hybrid vehicles will generate reliable cash flows through 2030 and beyond

- Toyota’s manufacturing scale in ICE gives it cost advantages that pure-EV startups cannot match

2. Hybrid and Hydrogen Leadership (Optionality Value)

- Toyota pioneered mass-market hybrids with the Prius (1997), selling 5+ million units

- Hybrids currently account for ~27% of Toyota’s total vehicle sales

- Hydrogen fuel cell technology (Mirai model) provides additional optionality

- These technologies serve as a bridge that competitors like Tesla do not have

3. EV Investment Is Coming (Growth Upside)

- Toyota announced plans to invest US$70 billion in electrifying part of its fleet by 2030

- The company is not ignoring EVs; it is sequencing the transition differently

- Recent solid-state battery breakthroughs could leapfrog current lithium-ion technology

For investors, the question is not “Will Toyota make EVs?”, it is “Does the market correctly price Toyota’s strategic optionality?”

Hybrid and Hydrogen Leadership, and More EVs Coming, Could Prove Critics Wrong

- Toyota is a pioneer in the mass production of hybrid technology, having rolled out its hybrid “Prius” model in 1997, since selling more than 5m. Currently, hybrids account for about 27% of total vehicle sales.

- Toyota is pushing ahead with hydrogen-powered cars, currently selling its “Mirai” model. The beaten-down share price is some evidence that observers expect the company’s hydrogen offerings will eventually fail.

- But there is promise to the technology, and an investor could consider Toyota’s hydrogen to have an option value. Of course, Toyota has not turned its back on EVs; recently, announcing plans to invest US$70bn in electrifying part of its fleet by 2030.

- We appreciate Toyota’s diversified approach to transition to more carbon-neutral cars and expect total CAPEX spending of about JPY12trn over the next few years.

How Was Toyota Valued? DCF Methodology Explained

The DCF valuation of Toyota uses the Free Cash Flow to the Firm (FCFF) approach. Here are the key assumptions and inputs:

DCF Model Inputs

| Input | Value | Rationale |

|---|---|---|

| Risk-Free Rate | 1% | Japanese government bond yield |

| Market Equity Risk Premium | 10% | Japanese market premium |

| Beta | 1.0x | Market-average risk |

| Debt-to-Total Capital | 44.6% | Toyota’s capital structure |

| WACC / Discount Rate | 6.4% | Blended cost of capital |

| Terminal Growth Rate | 1% | Conservative long-term GDP growth |

| Projection Period | Through 2027E | 5-year forecast horizon |

Valuation Scenarios

| Scenario | Gross Margin Assumption | FCFF Value per Share | Upside vs. Market Price |

|---|---|---|---|

| Base Case | 18.2% p.a. through 2027E | JPY 2,509 | ~40% |

| Optimistic Case | 20.2% p.a. through 2027E | JPY 2,802 | ~57% |

The 5-year revenue projection assumes Toyota returns to its pre-pandemic average growth level, achieving a CAGR of approximately 6.9%.

Why FCFF Instead of FCFE?

The FCFF approach was chosen because:

- Toyota carries significant debt (44.6% debt-to-capital), making the capital structure an important factor

- FCFF captures the value of the entire firm before debt payments, then adjusts for debt

- This is the standard approach for capital-intensive manufacturing companies

For more on this methodology, see our complete DCF valuation guide.

Ready to advance?

The Advancer Program helps mid-career professionals sharpen their valuation and equity research skills and stand out for promotions or lateral moves into investment roles.

How Does Toyota Compare to Automotive Peers?

Valuation does not happen in a vacuum. To understand whether Toyota is cheap or expensive, analysts compare its multiples to those of its peers. Here is how Toyota stacks up against key competitors:

| Company | P/E (TTM) | EV/EBITDA | P/B | Revenue ($B) | EV Strategy |

|---|---|---|---|---|---|

| Toyota | ~13.5x | ~12.2x | ~1.0x | ~$322B | Multi-pathway (hybrid + hydrogen + BEV) |

| Tesla | ~65x+ | ~45x+ | ~12x+ | ~$97B | Pure BEV |

| BYD | ~20x | ~15x | ~4x | ~$95B | BEV + plug-in hybrid |

| Volkswagen | ~4x | ~3x | ~0.3x | ~$300B | BEV transition |

| Hyundai | ~5x | ~5x | ~0.5x | ~$120B | Multi-pathway |

Key observations:

- Toyota trades at a significant discount to Tesla but at a premium to European and Korean OEMs

- The P/B ratio of ~1.0x at the time of analysis suggested the market was pricing Toyota at roughly its book value, implying zero growth premium

- Hyundai’s parallel strategy offers the closest strategic comparison, and it trades at an even deeper discount

- Mercedes-Benz and other legacy automakers face similar valuation challenges during the EV transition

The gap between Tesla’s ~65x P/E and Toyota’s ~13.5x P/E illustrates the market’s willingness to pay for perceived EV leadership even when Toyota generates far more revenue and profit.

Negative Sentiment Pressuring Price, But at 1x PB, It Might Be the Time to Buy

- The sector is unfavorable given recession fears, as well as investors’ doubts about Toyota’s unconventional EV policies and its ability to defend its position as the world’s largest carmaker.

- The company’s price-to-book ratio (PB) dropped below 1x, which is 1x std dev below its long-term average.

- With an average net margin of 7.8% over the past 5 years, Toyota is among the most profitable automobile companies in the world.

- We believe negative sentiment has been too punishing, and the stock deserves a re-rating.

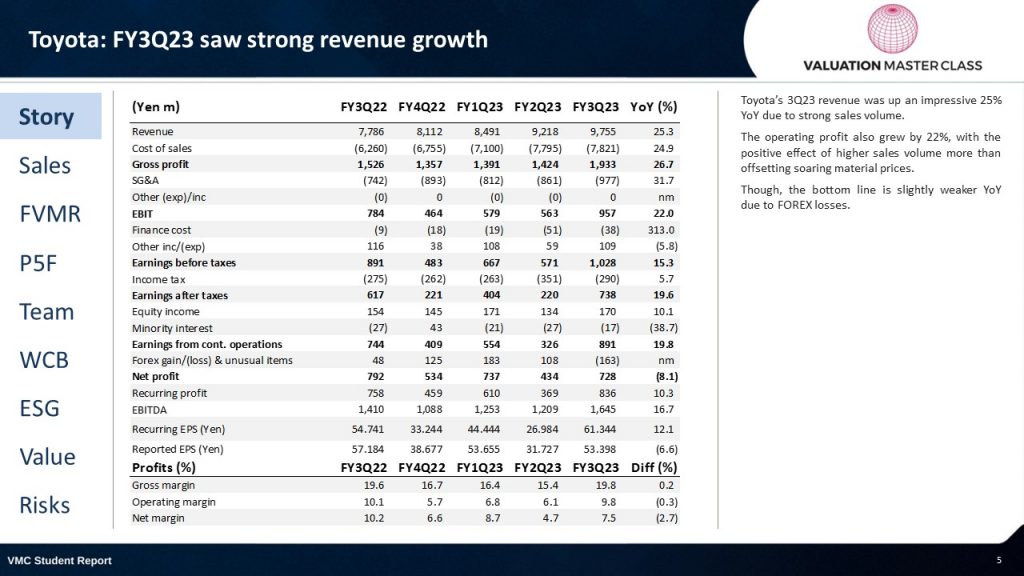

FY3Q23 Saw Strong Revenue Growth

- Toyota’s 3Q23 revenue was up an impressive 25% YoY due to strong sales volume.

- The operating profit also grew by 22%, with the positive effect of higher sales volume more than offsetting soaring material prices.

- Though the bottom line is slightly weaker YoY due to FOREX losses.

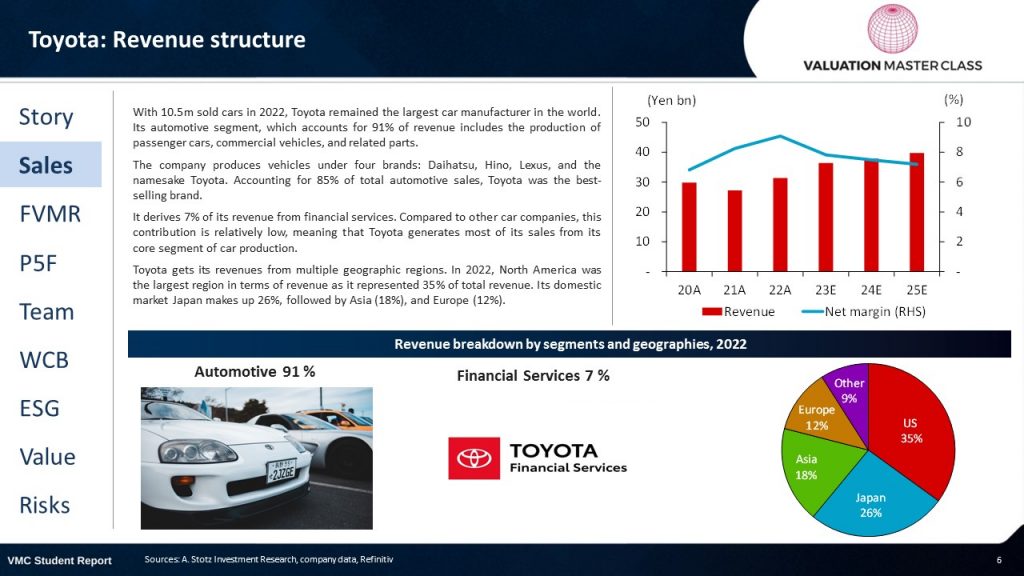

Revenue Structure

- With 10.5m sold cars in 2022, Toyota remained the largest car manufacturer in the world. Its automotive segment, which accounts for 91% of revenue, includes the production of passenger cars, commercial vehicles, and related parts.

- The company produces vehicles under four brands: Daihatsu, Hino, Lexus, and the namesake Toyota. Accounting for 85% of total automotive sales, Toyota was the best-selling brand.

- It derives 7% of its revenue from financial services. Compared to other car companies, this contribution is relatively low, meaning that Toyota generates most of its sales from its core segment of car production.

- Toyota gets its revenues from multiple geographic regions. In 2022, North America was the largest region in terms of revenue as it represented 35% of total revenue. Its domestic market Japan, makes up 26%, followed by Asia (18%), and Europe (12%).

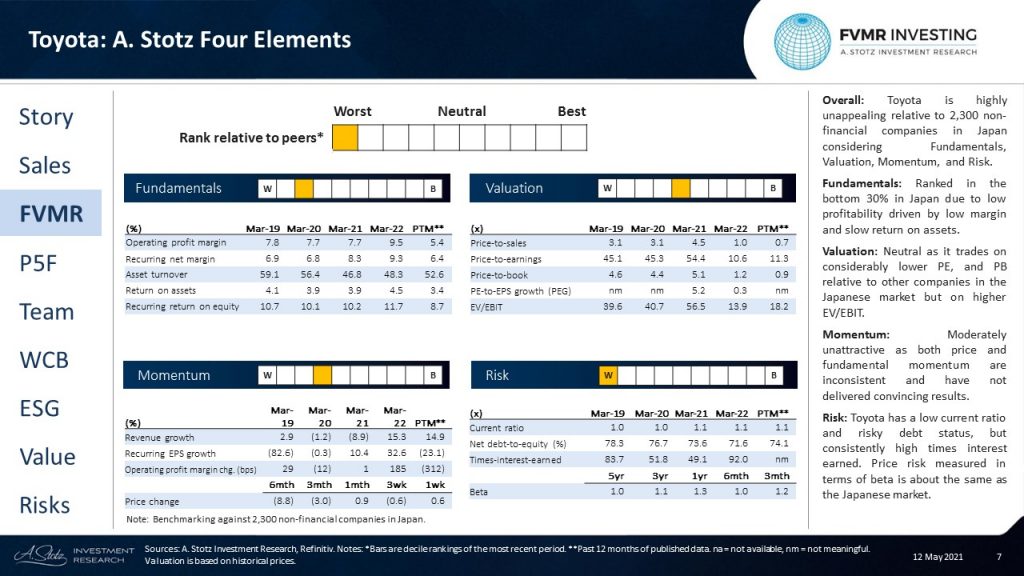

A. Stotz Four Elements

- Overall: Toyota is highly unappealing relative to 2,300 non-financial companies in Japan, considering Fundamentals, Valuation, Momentum, and Risk.

- Fundamentals: Ranked in the bottom 30% in Japan due to low profitability driven by low margins and slow return on assets.

- Valuation: Neutral as it trades on considerably lower PE and PB relative to other companies in the Japanese market, but on higher EV/EBIT.

- Momentum: Moderately unattractive as both price and fundamental momentum are inconsistent and have not delivered convincing results.

- Risk: Toyota has a low current ratio and risky debt status, but consistently high times interest earned. Price risk, measured in terms of beta, is about the same as the Japanese market.

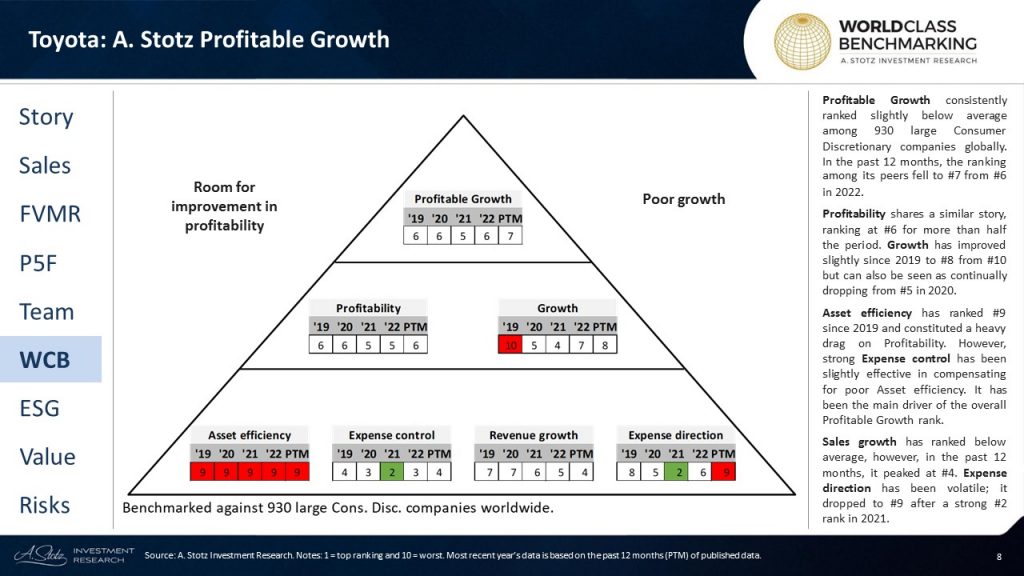

A. Stotz Profitable Growth

- Profitable Growth consistently ranked slightly below average among 930 large Consumer Discretionary companies globally. In the past 12 months, the ranking among its peers fell to #7 from #6 in 2022.

- Profitability shares a similar story, ranking at #6 for more than half the period. Growth has improved slightly since 2019 to #8 from #10 but can also be seen as continually dropping from #5 in 2020.

- Asset efficiency has ranked #9 since 2019 and constituted a heavy drag on Profitability. However, strong Expense control has been slightly effective in compensating for poor Asset efficiency. It has been the main driver of the overall Profitable Growth rank.

- Sales growth has ranked below average; however, in the past 12 months, it peaked at #4. Expense direction has been volatile; it dropped to #9 after a strong #2 rank in 2021.

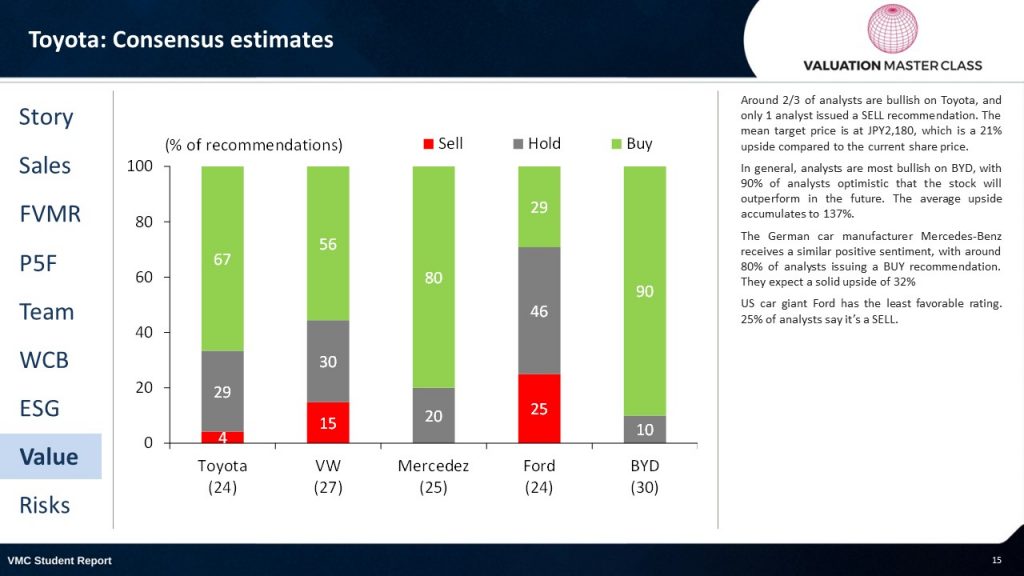

Consensus Estimates

- Around 2/3 of analysts are bullish on Toyota, and only 1 analyst issued a SELL recommendation.

- The mean target price shows about a 21% upside.

- In general, analysts are most bullish on BYD, with 90% of analysts optimistic that the stock will outperform in the future. The average upside is 137%.

- The German car manufacturer Mercedes-Benz receives a similar positive sentiment, with around 80% of analysts issuing a BUY recommendation. They expect a solid upside of 32%

- US car giant Ford has the least favorable rating. 25% of analysts say it’s a SELL.

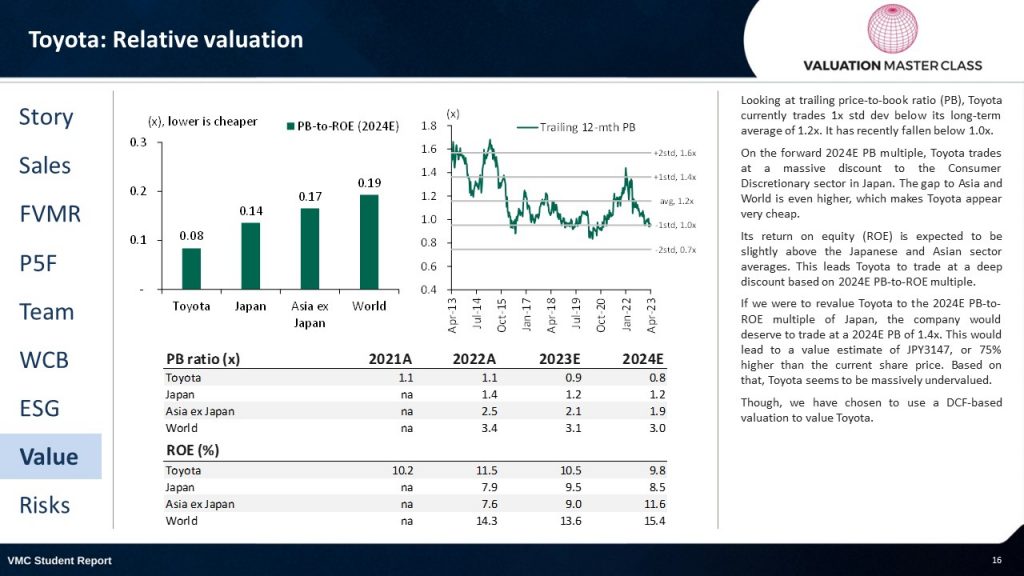

Relative Valuation

- The trailing price-to-book ratio (PB) shows that Toyota is trading 1x std dev below its long-term average of 1.2x. And it has recently fallen below 1.0x.

- On the forward 2024E PB multiple, Toyota trades at a massive discount to the Consumer Discretionary sector in Japan. The gap between Asia and the world is even higher, making Toyota appear cheap.

- I expect its return on equity (ROE) of 10% to be slightly above Japanese and Asian sector averages, which leads Toyota to trade at a deep discount based on the 2024E PB-to-ROE multiple.

- If we were to revalue Toyota to the 2024E PB-to-ROE multiple of Japan, the company would deserve to trade at a 2024E PB of 1.4x. This would lead to a value estimate of JPY3147, or 75% higher than the current share price. Based on that, Toyota seems to be massively undervalued.

- Though we have chosen to use a DCF-based valuation to value Toyota.

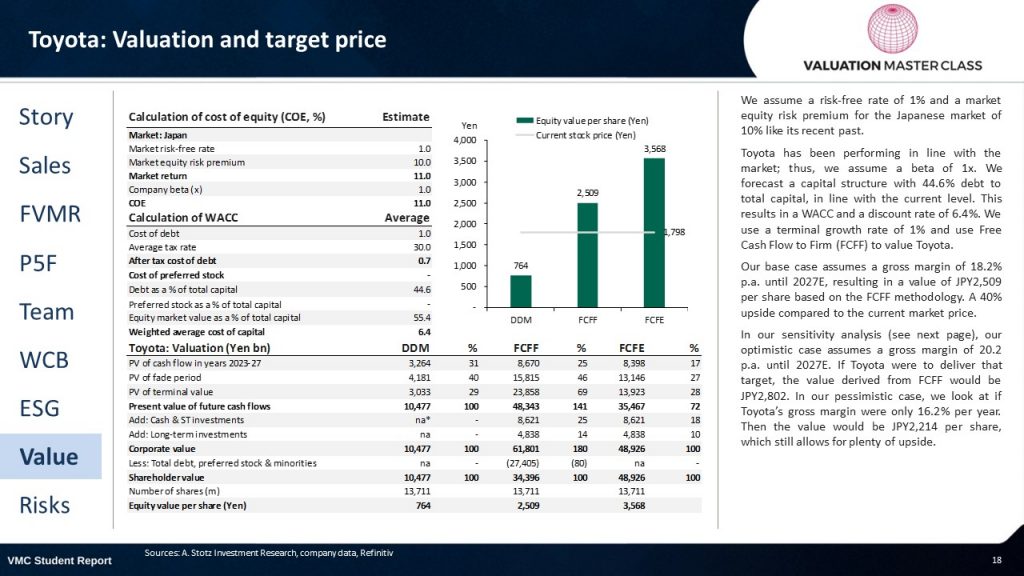

Valuation and Target Price

- We assume a risk-free rate of 1% and a market equity risk premium for the Japanese market of 10%, like its recent past.

- Toyota has been performing in line with the market; thus, we assume a beta of 1x. We forecast a capital structure with 44.6% debt to total capital, in line with the current level. This results in a WACC and a discount rate of 6.4%. We use a terminal growth rate of 1% and use Free Cash Flow to Firm (FCFF) to value Toyota.

- Our base case assumes a gross margin of 18.2% p.a. until 2027E, resulting in a value of JPY2,509 per share based on the FCFF methodology. A 40% upside compared to the current market price.

- In our sensitivity analysis (see next page), our optimistic case assumes a gross margin of 20.2 p.a. until 2027E. If Toyota were to deliver that target, the value derived from FCFF would be JPY2,802. In our pessimistic case, we look at if Toyota’s gross margin was only 16.2% per year. Then the value would be JPY2,214 per share, which still allows for plenty of upside.

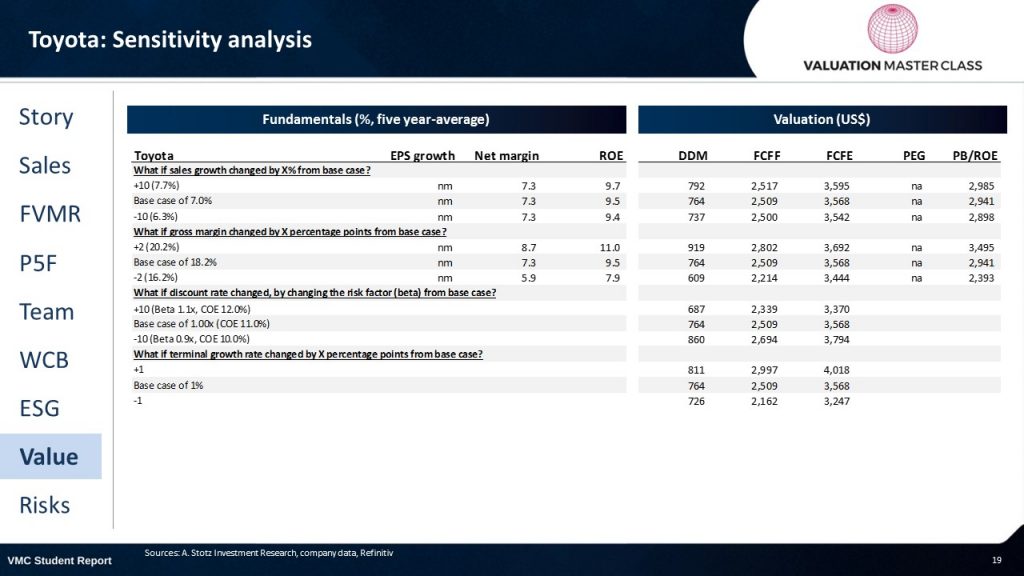

Sensitivity Analysis

The Main Risk Is the Failure to Adapt to the Industry Trends

Failure to Adapt to the Industry Trends

- We built our forecast around the fact that Toyota’s decision to delay the full shift to EVs is a wise decision, and also around the fact that it would be successful in its endeavors toward hybrids, electric, and hydrogen fuel cars.

- Any sudden change in consumer preferences would hurt the company’s short-term results.

- Also, any failure in the production of its new hybrid, electric, or hydrogen fuel cars would hurt the automaker’s long-term results.

- Toyota recently offered to buy back its new electric SUV (BZ4X) from its owners because of a severe problem: the wheels could fall off while driving, even after just a short time on the road! Anything like that would drag down our target price and affect the company’s position in the market.

Soaring Raw Material Prices

- Prices of raw materials such as cobalt, lithium, and nickel have surged. In May 2022, lithium prices were over seven times higher than at the start of 2021.

- Unprecedented battery demand and a lack of structural investment in new supply capacity are key factors. Russia’s invasion of Ukraine has created further pressure since Russia supplies 20% of global high-purity nickel.

- Also, China produces three-quarters of all lithium-ion batteries and is home to 70% of the production capacity for cathodes and 85% of the production capacity for anodes (both are key components of batteries), so if geopolitical tensions lasted long, it would cause huge drops in the company’s margins and disruptions in its supply chain.

Concentration of Suppliers

- Automakers must rely on suppliers of cheaper raw materials to succeed in the automotive industry.

- But, Toyota depends on a limited number of suppliers, whose replacement with others may be difficult, exposing the company to a wide range of risks.

- Any loss of an important supplier or inability to obtain materials in a timely and cost-effective manner could lead to increased costs or delays in Toyota’s production and deliveries, which would hurt the company’s revenues and margins.

- Nonetheless, Toyota has managed to build great relationships with its suppliers, which reduces the risk of losing them.

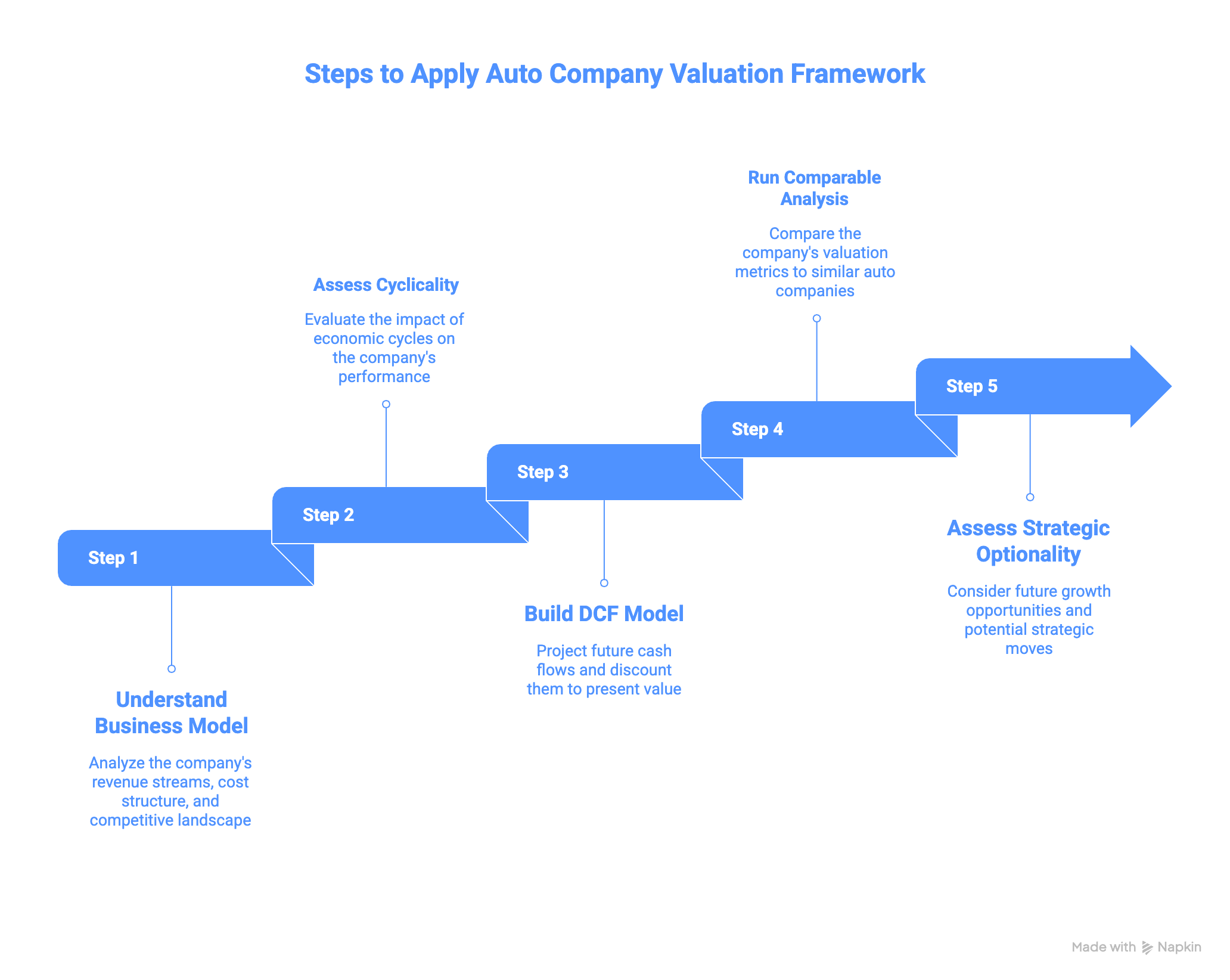

How to Apply This Valuation Framework to Other Auto Companies

The methodology used to value Toyota can be applied to any automotive company. Here is a step-by-step framework:

Step 1: Understand the Business Model

Identify which powertrains (ICE, hybrid, BEV, hydrogen) drive revenue. Map revenue by geography. Determine whether the company is a volume manufacturer (Toyota, Volkswagen) or a premium/niche player (Ferrari, Volvo).

Step 2: Assess Cyclicality

Automotive companies are cyclical businesses. Use normalized earnings or mid-cycle margins rather than peak-year figures. Toyota’s 18.2% gross margin assumption reflects a mid-cycle estimate, not peak profitability.

Step 3: Build the DCF Model

- Calculate WACC using local market inputs (risk-free rate, equity risk premium, beta)

- Project revenue growth using industry growth rates and company-specific factors

- Model gross margins conservatively with sensitivity analysis

- Apply a terminal growth rate that reflects long-term GDP growth

- Use FCFF for companies with significant debt (like most automakers)

Step 4: Run Comparable Analysis

Compare P/E, EV/EBITDA, and P/B ratios against peers. Adjust for differences in growth rates, EV exposure, and geographic mix. The peer comparison table above is a template for this analysis.

Step 5: Assess Strategic Optionality

For companies in transitioning industries, traditional DCF may undervalue strategic options. Toyota’s hydrogen and solid-state battery programs have an option value that a base-case DCF does not fully capture. Consider scenario analysis (base, optimistic, pessimistic) to bound the valuation range.

For a deeper dive into choosing the right approach, see which valuation method is most suitable for different types of companies.

Switching into finance from another field?

Our Switcher Program is designed for career changers who need to build credibility fast — no finance background required.

Common Mistakes When Valuing Automotive Companies

Analysts frequently make these errors when valuing automakers like Toyota:

1. Using Peak-Year Margins in DCF Projections

Auto companies are cyclical. Using a single year’s high margins in your DCF will overstate intrinsic value. Always normalize margins across the cycle. The Toyota case study uses an 18.2% gross margin, not the highest recent year, but a sustainable mid-cycle estimate.

2. Ignoring Capital Intensity

Automakers require enormous capital expenditures for new platforms, factories, and technology. Failing to model capex correctly will inflate free cash flow projections. Toyota’s $70 billion EV investment commitment must be reflected in the model.

3. Treating All EV Exposure as Positive

The market assigns premium multiples to “EV companies,” but the transition is expensive. Tesla’s valuation reflects this premium, while legacy automakers’ spending billions on EV transitions often sees their margins compress. Not all EV exposure creates value.

4. Applying a Single Valuation Multiple

Toyota operates across multiple geographies, powertrains, and segments. A single P/E or EV/EBITDA multiple cannot capture this complexity. Use sum-of-the-parts valuation or, at a minimum, run DCF scenario analysis.

5. Ignoring the Japanese Market Context

Toyota’s WACC reflects Japanese market conditions: a 1% risk-free rate and 10% equity risk premium. Applying US-centric discount rates to a Japanese company will produce incorrect valuations. Always use local market inputs for cost of capital calculations.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.

Frequently Asked Questions

What is Toyota’s intrinsic value based on DCF analysis?

Using a Free Cash Flow to the Firm (FCFF) approach with a WACC of 6.4% and a terminal growth rate of 1%, the base-case DCF valuation yields JPY 2,509 per share. This assumed an 18.2% gross margin through 2027E. An optimistic scenario using 20.2% gross margins produces a value of JPY 2,802 per share. Both scenarios suggested approximately 40-57% upside relative to Toyota’s market price at the time of analysis, though the stock has since appreciated significantly.

Why does Toyota trade at a lower P/E than Tesla?

Toyota trades at roughly 13.5x trailing earnings compared to Tesla’s 65x+ because the market prices growth expectations, not current profitability. Tesla is perceived as a pure-play EV growth company, while Toyota is seen as a mature, cyclical automaker. However, Toyota generates more than 3x Tesla’s revenue and significantly higher absolute profits. The valuation gap reflects differing market narratives about the future of the auto industry, not current financial performance.

Is Toyota’s hybrid strategy better than going all-in on EVs?

Toyota’s multi-pathway approach, combining hybrids, hydrogen fuel cells, and battery EVs, may create more shareholder value than an EV-only strategy. Hybrids generate immediate cash flow and serve markets without EV infrastructure. Hydrogen provides long-range, heavy-vehicle optionality. Battery EVs address regulatory and consumer demand in developed markets. By not committing exclusively to one technology, Toyota preserves strategic flexibility, though it risks falling behind in BEV scale if the market shifts faster than expected.

How do you value a cyclical company like Toyota?

Valuing cyclical companies requires normalizing earnings across the business cycle rather than using peak or trough figures. For Toyota, this means using a mid-cycle gross margin estimate (18.2%) rather than the best or worst recent year. Apply a DCF model with a projection period long enough to capture a full cycle (5-7 years), use conservative terminal growth rates, and run sensitivity analysis on key margin assumptions. See our detailed guide on how to value cyclical companies.

What WACC should you use for a Japanese company like Toyota?

Toyota’s WACC of 6.4% reflects Japanese market conditions: a 1% risk-free rate (Japanese government bonds), a 10% market equity risk premium for Japan, a beta of 1.0x, and a capital structure with 44.6% debt-to-total capital. When valuing Japanese companies, always use local inputs rather than US Treasury rates or US equity risk premiums. The lower risk-free rate in Japan typically produces a lower WACC than equivalent US companies, which increases the present value of future cash flows.

What is the best way to learn company valuation online?

The most effective way to learn company valuation is through case-study-based programs that apply real methods to real companies, exactly like this Toyota analysis. Valuation Master Class offers a hands-on business valuation course designed by Dr. Andrew Stotz, a former #1-ranked equity analyst. The program covers DCF valuation, comparable analysis, and financial modeling using real company data, so you build practical skills you can apply immediately in your career.

Ready to Take the Next Step?

Join 5,000+ finance professionals who’ve leveled up with Valuation Master Class.